VA Loan Residual Income and DTI Requirements in San Antonio (2026): The Approval Rule Most Veterans Have Never Heard Of

LAST UPDATED: JULY 17, 2026 | BY CHRISTOPHER BEAL, U.S. ARMY VETERAN & REALTOR

VA Loan Residual Income and DTI Requirements in San Antonio (2026): The Approval Rule Most Veterans Have Never Heard Of

Key Takeaways

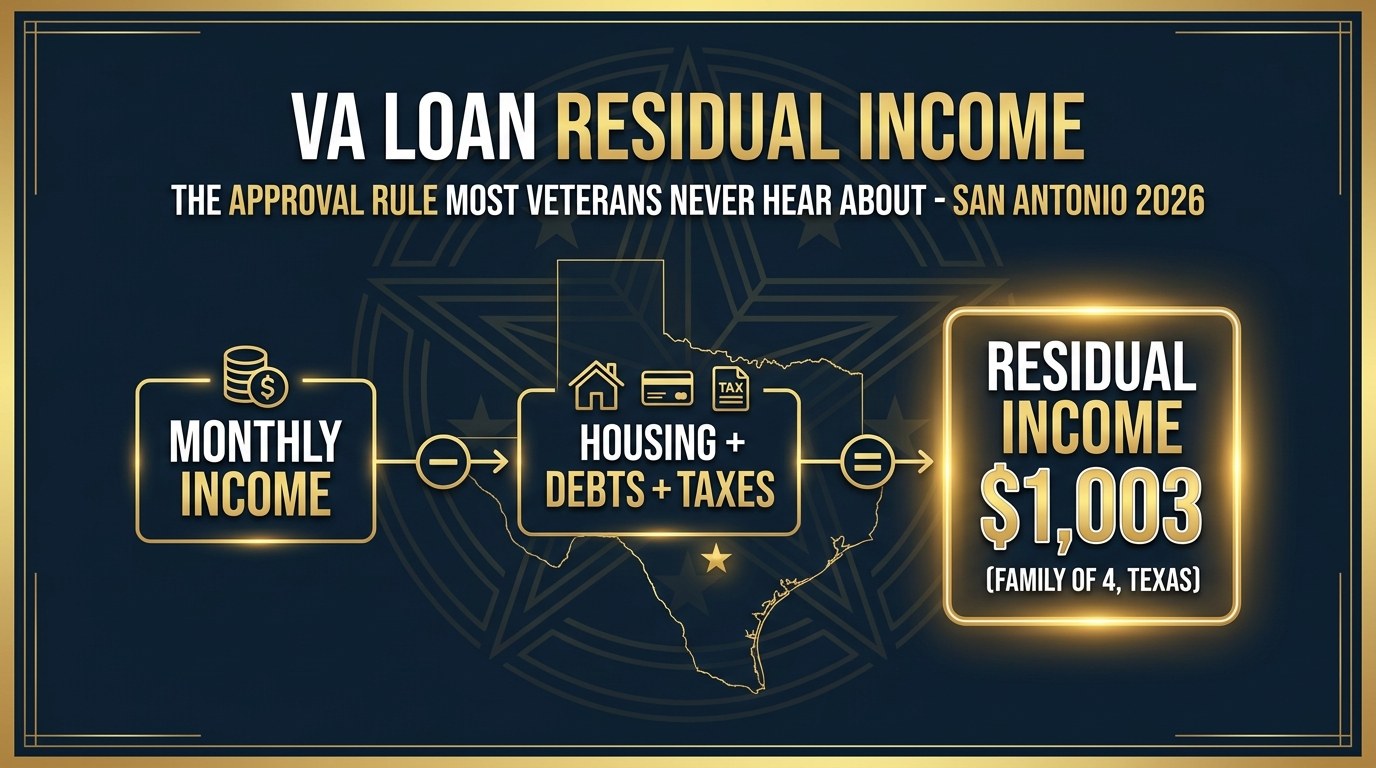

- Residual income is the cash left over each month after your new house payment, debts, taxes, and home maintenance estimate. In Texas (VA South region), a family of 4 needs $1,003 a month on loans of $80,000 or more.

- The VA's 41 percent debt-to-income figure is a benchmark, not a hard cap. Lenders approve VA loans above 41 percent DTI every week - but only when residual income is at least 120 percent of the guideline.

- BAH and disability compensation are non-taxable, so lenders gross them up. That is why military buyers in San Antonio often qualify for more than an online calculator suggests.

- Most surprise VA denials trace to residual income, not credit score. Childcare costs, car payments, and family size move the number more than veterans expect.

- San Antonio's median price near $311,025 (SABOR/LERA, July 2026) keeps residual income math friendlier here than almost any major Texas metro.

In This Guide

- What Is VA Residual Income?

- What Are the 2026 Residual Income Charts for Texas?

- How Do Lenders Calculate It?

- Is 41 Percent DTI a Hard Cap?

- How Do BAH and Non-Taxable Income Change the Math?

- Why Do VA Loans Get Denied on Residual Income?

- What Does San Antonio Pricing Mean for Your Numbers?

- How Can You Improve Residual Income Before Applying?

What Is VA Residual Income and Why Does It Decide Your Approval?

The VA underwrites family security, not just repayment odds. Conventional loans lean almost entirely on credit score and debt-to-income ratio. The VA adds a second test that no other major loan program uses: after every major obligation is paid, does this family still have enough cash to buy groceries, gas, uniforms, and school supplies? That cushion is residual income, and it is the reason VA loans carry some of the lowest foreclosure rates in the mortgage industry despite requiring zero down payment.

Most veterans I work with in San Antonio have never heard the term until a lender mentions it, usually at the worst possible moment - mid-application. Understanding it before you shop is a genuine advantage: it tells you your real price ceiling, it explains why two families with identical incomes qualify for different amounts, and it is the single best predictor of whether your file sails through underwriting at Lackland, Randolph, or Fort Sam Houston pay grades.

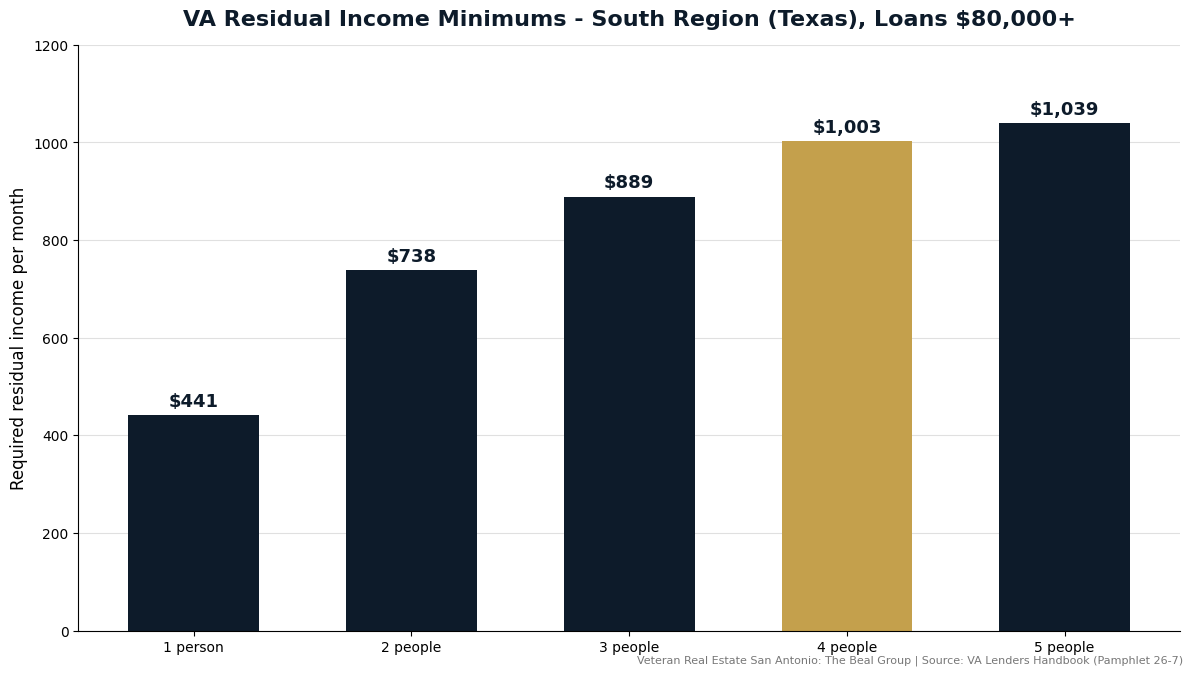

What Are the 2026 VA Residual Income Charts for Texas?

The chart is set by the VA Lenders Handbook and it is refreshingly simple. Find your family size, find your loan tier, and that is your required cushion. Every member of the household counts, including newborns, and an expecting family counts the baby. Active-duty borrowers get a small offset for on-base savings such as commissary and exchange privileges, which lenders may apply at $75 a month.

| Household Size | Loans Under $80,000 | Loans $80,000 and Above |

|---|---|---|

| 1 | $382 | $441 |

| 2 | $641 | $738 |

| 3 | $772 | $889 |

| 4 | $868 | $1,003 |

| 5 | $902 | $1,039 |

| 6-7 | Add ~$75-$80 per member | Add ~$80 per member |

Source: VA Lenders Handbook (Pamphlet 26-7), South region (includes Texas). Figures apply per month and are unchanged in the 2026 handbook tables.

How Do Lenders Actually Calculate Your Residual Income?

Walk through a real San Antonio example and the concept snaps into focus. Take an E-6 at Randolph with a spouse and two kids buying a $290,000 home in Schertz: roughly $4,400 base pay plus $2,094 BAH and $460 BAS. The lender subtracts estimated federal taxes on the taxable portion, the full new payment of about $2,510 including taxes and insurance, a $450 car payment, $180 in minimum card payments, $600 in childcare, and a utilities-and-maintenance estimate near $250 for an 1,800 square foot home.

Run the arithmetic and this family clears roughly $1,900 - comfortably above the $1,003 requirement for a family of four. That is a strong file even though the same numbers produce a DTI in the mid-40s, which would rattle a conventional underwriter. It is a perfect illustration of why VA buyers should never pre-judge their own file using conventional-loan rules of thumb, and why a real VA pre-approval beats every online calculator.

Is the VA Loan 41 Percent DTI Limit Actually a Hard Cap in 2026?

This is the most misunderstood number in VA lending. A conventional loan can die at its DTI cap no matter how strong the rest of the file looks. A VA file at 45 or even 50 percent DTI remains approvable when the residual cushion is fat: the working rule is 120 percent of the chart figure, so a Texas family of four above 41 percent DTI needs about $1,204 of residual income instead of $1,003. Lenders also weigh compensating factors like tax-free income, months of reserves, minimal payment shock, and a long service history.

| Test | Conventional Loan | VA Loan |

|---|---|---|

| Primary approval gate | Credit score + DTI cap | Residual income + overall file |

| DTI above 41-45% | Usually a denial or pricing hit | Approvable with 120% residual cushion |

| Non-taxable income (BAH, disability) | Counted at face value | Grossed up for qualifying |

| Family size | Ignored | Directly raises the required cushion |

| Down payment required | 3-20% | Zero |

Source: VA Lenders Handbook underwriting chapters and standard agency guidelines, July 2026. Individual lender overlays vary.

How Do BAH and Non-Taxable Income Change the Residual Income Math?

Military money is built differently, and the VA test rewards it. A civilian earning $7,000 gross loses a slice to federal taxes before the residual math starts. An E-7 whose $7,000 includes $2,112 of BAH and $460 of BAS only pays federal tax on the base-pay portion, so hundreds of extra dollars survive into the residual column. VA disability compensation works the same way for veteran buyers, and it also triggers a funding fee exemption that lowers the loan itself.

This is the quiet reason San Antonio military families punch above their weight as buyers. Check your exact allowance on my 2026 JBSA BAH rates guide, because grade and dependency status shift the figure - an E-6 with dependents draws $2,094 while an O-3 draws $2,127, and 2025 arrivals often carry grandfathered higher rates.

Why Do VA Loans Get Denied for Residual Income, and How Do You Fix It?

A residual income denial is almost never about income - it is about the subtraction column. The patterns I see repeatedly in San Antonio: a $750 truck payment that consumes the entire cushion, daycare for two kids at $1,400 a month that a pre-qual never asked about, a fifth household member arriving mid-process, or a jump from an 1,800 to a 3,200 square foot home that silently adds $200 of assumed maintenance. None of these show up in an online affordability widget.

The fixes are practical: pay the truck down or trade it, document a family member's childcare help in writing, choose the right square footage for your actual budget, or simply buy $25K below your maximum. A good agent structures the offer side too - seller-paid closing costs keep your reserves intact, and my Serve & Save program reduces closing costs with a credit of 1 percent per year of service, up to 6 percent. If credit depth is your limiting factor instead, start with my VA credit score guide.

What Does San Antonio Pricing Mean for Your Residual Income in 2026?

Geography is doing half the work for you here. The same E-6 income that struggles against the residual chart in Denver or San Diego clears it comfortably in Converse, Universal City, Schertz, or Alamo Ranch, because the payment on a median San Antonio home is hundreds of dollars lighter. Today's buyer's market compounds the advantage: sellers negotiating price, paying closing costs, and buying down rates all lower the PITI that gets subtracted in your residual calculation.

Price tiers matter, though. At $250K most dual-income families pass easily; at $350K a single-income family of five needs honest budgeting; at $450K and above the maintenance estimate and property taxes start to bite, which is exactly the analysis in my VA jumbo loan guide. Disabled veterans should also stack the Texas property tax exemption, which can cut the tax line in the calculation dramatically - to zero at a 100 percent rating.

How Can You Improve Your Residual Income Before You Apply?

Five moves cover almost every file I see. First, the vehicle: one $600 payment eliminated is $600 of instant residual income, worth more than a raise. Second, small debts: closing out a $40 minimum here and a $60 minimum there adds up faster than people expect. Third, documentation: make sure your lender captures BAH, BAS, disability compensation, and any spouse income correctly, because sloppy income math understates your cushion. Fourth, the house itself: square footage is a monthly cost in this test, so buy the home your budget wants, not the biggest one your DTI allows. Fifth, the contract: a well-negotiated San Antonio deal in 2026 should have the seller carrying ordinary closing costs.

Useful primary sources as you prepare: the VA's official home loan portal, the full VA Lenders Handbook (Pamphlet 26-7), and the CFPB's DTI explainer. Then get an actual pre-approval - it is free, it is fast, and it replaces guesswork with your real number.

About the Author: Christopher Beal

Christopher Beal is a U.S. Army veteran, the broker behind Veteran Real Estate San Antonio: The Beal Group at eXp Realty, and a Military Relocation Professional (MRP) and VAREP member. I have helped more than 300 families close over $120M in San Antonio real estate, earning recognition as a 3x San Antonio Business Journal Top 25 Individual Agent (#13 in 2024, #14 in 2025, #20 in 2026), a 7x eXp ICON Agent, and a 2x RateMyAgent Agent of the Year, with a 5.0 rating across 370+ verified client reviews. I hold TREC license #723559. VA loans are the core of my practice - from first pre-approval questions like residual income to jumbo files on Hill Country estates - and my Serve & Save program reduces closing costs by 1 percent per year of service, up to 6 percent. When you call, you get me, not a team handoff.

Explore More Resources

- VA Home Loans in San Antonio

- Military Relocation / PCS to JBSA

- Free Home Evaluation

- Serve & Save Program

- Client Reviews

- About Christopher Beal

Frequently Asked Questions: VA Residual Income and DTI

What is the VA residual income requirement in Texas for 2026?

Texas is in the VA's South region. For loans of $80,000 or more, the monthly minimums are $441 for one person, $738 for two, $889 for three, $1,003 for four, and $1,039 for five, adding roughly $80 per additional household member up to seven.

Is 41 percent DTI an automatic denial on a VA loan?

No. Above 41 percent, the VA asks lenders to justify the approval, most commonly with residual income at least 120 percent of the chart figure or other compensating factors. Files in the mid-40s are approved routinely when the cushion is strong.

What counts against my residual income?

The full new house payment including taxes and insurance, estimated federal income taxes, monthly debt payments, childcare and dependent care costs, alimony or child support, and a maintenance-and-utilities estimate of about 14 cents per square foot of the home.

Does BAH count as income for a VA loan?

Yes, fully. BAH and BAS are non-taxable, so they flow into residual income at face value, and lenders gross them up when computing your DTI. Active-duty buyers at JBSA should verify their exact 2026 rate because it varies by grade and dependency status.

Does family size really change how much house I can buy?

Yes. Each additional household member raises the required monthly cushion - a single E-5 needs $441 while an E-5 with a spouse and three kids needs $1,039. Same paycheck, different ceiling. Lenders count every dependent, including a baby on the way.

Why was my VA loan denied when my credit score was fine?

Residual income is the most common hidden reason. Large car payments, childcare costs, or an oversized home can push your leftover cash below the chart even with excellent credit. The fix is usually restructuring debt or adjusting price point, not waiting on your score.

Do I need reserves or savings to pass the residual income test?

Reserves are not part of the residual calculation itself, but they are a compensating factor that helps files above 41 percent DTI. Keeping your savings intact by negotiating seller-paid closing costs strengthens both sides of your file.

Does VA disability income help me qualify?

Yes, twice. Disability compensation is non-taxable income that boosts residual and gets grossed up for DTI, and veterans receiving it are exempt from the VA funding fee, which lowers the loan amount. Texas adds property tax exemptions on top.

Is the residual income rule different for a VA jumbo loan in San Antonio?

The chart tiers stop at $80,000 and above, so a jumbo file uses the same minimums - but bigger homes carry bigger tax, insurance, and maintenance numbers, so the subtraction column grows. Strong residual math matters even more at Hill Country price points.

How do I find out my actual residual income number?

A VA-fluent lender can calculate it in one conversation from your LES or pay stubs, debts, and family size. I connect San Antonio buyers with lenders who run this correctly up front, so the number never ambushes you mid-contract. Call or text (210) 882-8583.

Want your real number before you fall in love with a house? I will pair you with a VA-specialized lender and build your San Antonio search around a price point your residual income actually supports.

📲 Call or text: (210) 882-8583

📧 Email: [email protected]

🌐 Website: veteranrealestatesa.com

Categories

- All Blogs (314)

- Alamo Heights (4)

- awards (3)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (73)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (24)

- Market Trends (5)

- Market Update (13)

- Military Relocation (93)

- Military Retirement (3)

- Mortgage (16)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (25)

- Real Estate (31)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (64)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (23)

- VA Home Loans (24)

- VA Loans (32)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts