VA Energy Efficient Mortgage in San Antonio (2026): How Veterans Can Finance Home Upgrades

LAST UPDATED: JULY 10, 2026 | BY CHRISTOPHER BEAL, U.S. ARMY VETERAN & REALTOR

VA Energy Efficient Mortgage in San Antonio (2026): How Veterans Can Finance Home Upgrades

Key Takeaways

- A VA Energy Efficient Mortgage (EEM) is not a separate loan. It lets you add the cost of qualifying energy improvements on top of your VA purchase or refinance loan, with one closing and no down payment on the upgrade.

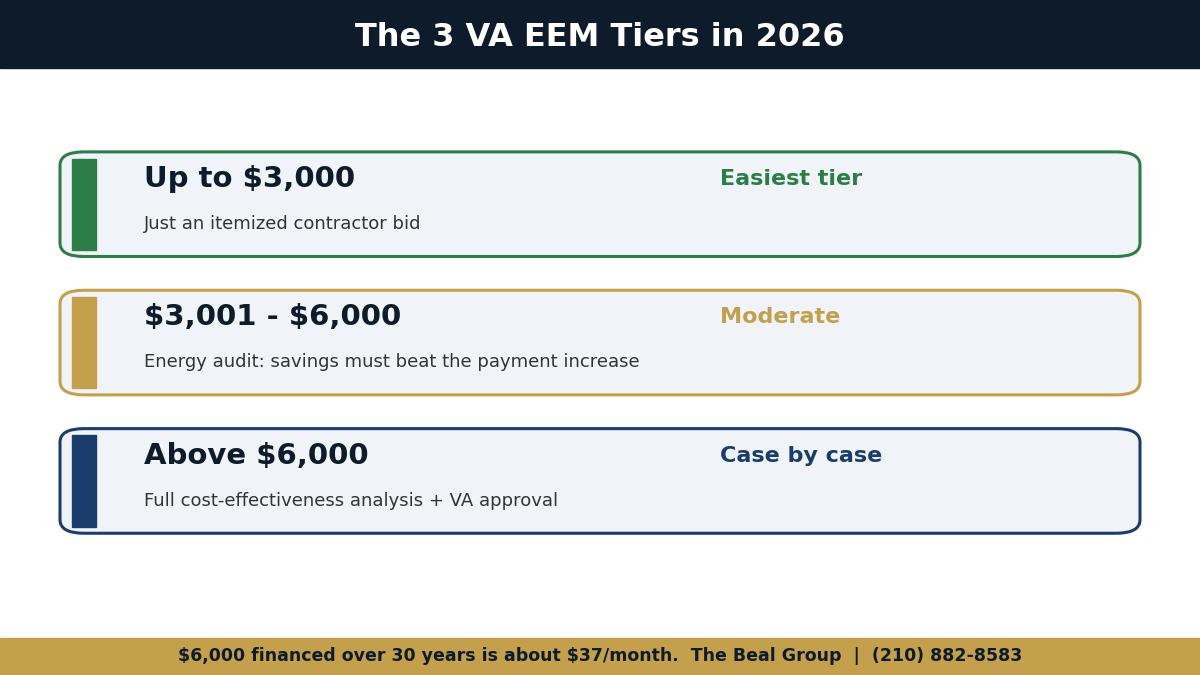

- In 2026 you can generally add up to 6,000 dollars for energy improvements. Up to 3,000 dollars is the easiest tier and usually needs only a contractor bid; 3,001 to 6,000 dollars requires proof that the energy savings exceed the payment increase.

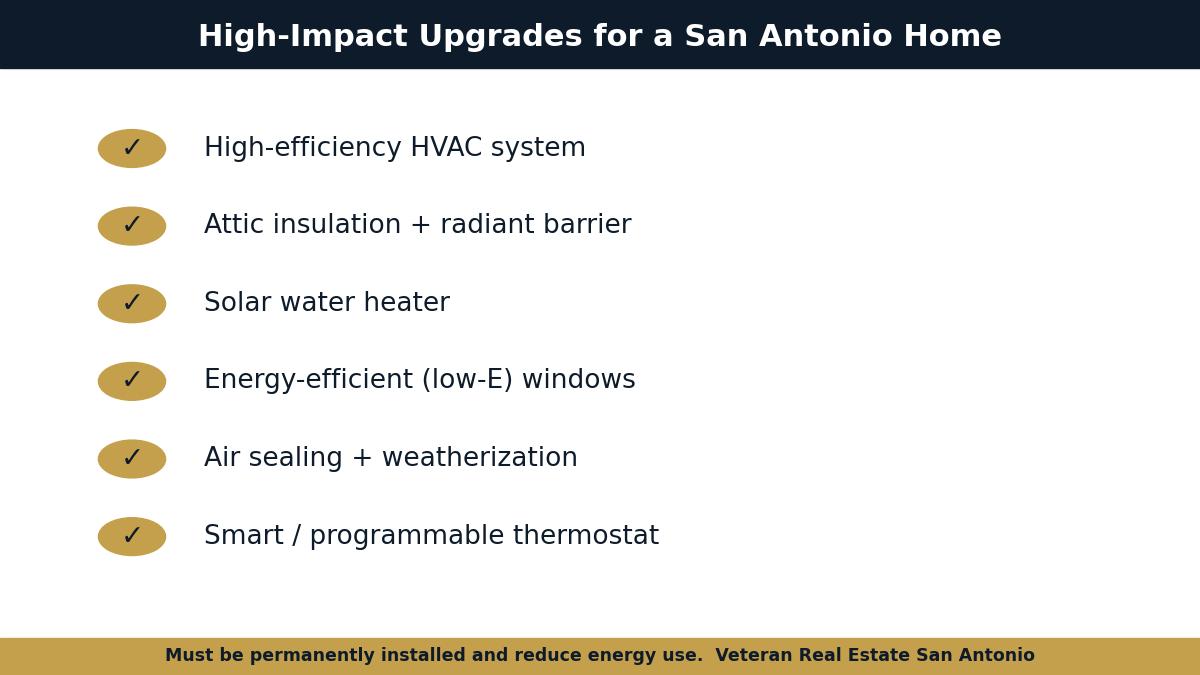

- Eligible upgrades include HVAC systems, attic insulation and radiant barrier, solar water heaters, energy-efficient windows, weatherization, and smart thermostats, all of which matter in San Antonio's long, hot summers.

- At 6,000 dollars financed over 30 years, the added payment is only about 37 dollars a month, and CPS Energy rebates can stack on top to lower your out-of-pocket cost further.

- The improvement funds are held in a VA escrow account and released to your contractor as the work is completed and verified, so plan the timeline with your lender and Realtor before closing.

In This Guide

A San Antonio summer will find every weak spot in your home's energy envelope. Triple-digit heat runs for weeks, air conditioners never stop, and CPS Energy bills climb right along with the thermometer. If you are buying a home with a VA loan, there is a benefit many veterans have never heard of that lets you fix those weak spots at closing, financed into the loan itself: the VA Energy Efficient Mortgage.

I am Christopher Beal, an Army veteran and the broker-owner of Veteran Real Estate San Antonio: The Beal Group. I have guided more than 306 families through San Antonio home purchases, and the EEM is one of the most underused tools in the VA loan playbook. This guide explains what it is, how much you can finance in 2026, which upgrades qualify in our climate, and exactly how to use it.

What Is a VA Energy Efficient Mortgage?

The EEM solves a real timing problem. Most buyers close on a home and only then discover the attic has almost no insulation or the 18-year-old air conditioner is on its last summer. Paying cash for those fixes right after a move is hard, and a separate home-improvement loan means new paperwork and another monthly bill. The EEM folds the cost into the mortgage you are already getting, so it closes when your loan closes.

Because the VA guarantees the loan, the program is designed to be low-friction. There is no additional down payment on the improvement amount, and for smaller projects there is not even an energy audit requirement. The upgrades must be permanently attached to the home and must reduce energy use in a measurable way.

How Much Can You Finance With a VA EEM in 2026?

The program is tiered by cost, and the tiers control how much documentation you need. Think of it as three doors, each opening a little wider but asking for a little more proof.

| Improvement Amount | What You Must Provide | Difficulty |

|---|---|---|

| Up to 3,000 dollars | Contractor bid itemizing costs and products | Easiest |

| 3,001 to 6,000 dollars | Energy audit showing savings exceed the payment increase | Moderate |

| Above 6,000 dollars | Full cost-effectiveness analysis, lender and VA approval | Case by case |

Source: U.S. Department of Veterans Affairs Energy Efficient Mortgage guidance; confirm current limits with your VA-approved lender.

Want to know whether a specific San Antonio home is a good EEM candidate before you write the offer? Request a free buyer consultation and I will help you and your lender scope it out.

What Energy Upgrades Qualify in San Antonio?

The VA keeps the eligible list broad, but our climate narrows what actually pays off. In San Antonio, cooling is the dominant load, so the improvements that move the needle most are the ones that keep heat out and help the air conditioner work less.

Common qualifying improvements include high-efficiency heating and cooling systems, added attic insulation and radiant barrier, solar water heaters, double-pane or low-E windows, air sealing and weatherization, and heat-pump water heaters. General remodeling, pools, and cosmetic work do not qualify; the upgrade has to save energy. If you are also buying new construction, my VA new-construction guide explains how builder homes and the EEM can fit together, and my guide to MUD and PID taxes covers another new-build cost to check.

Is a VA Energy Efficient Mortgage Worth It?

The math is usually favorable in our market for one reason: cooling costs are high. A worn-out 10 SEER air conditioner replaced with a modern high-efficiency unit can cut cooling energy use significantly during the five to six months a year San Antonio really runs the AC. When that saving beats a roughly 37-dollar monthly payment bump, you are ahead every month.

The EEM shines most for VA buyers who are tight on cash after a PCS move or a down-payment-free purchase. Instead of choosing between an emergency AC replacement and keeping your emergency fund, you finance the upgrade at your mortgage rate and keep your reserves. Learn more on my VA home loans page, and if you are relocating, the military relocation resources lay out the timeline.

How Do You Get a VA EEM Step by Step?

The single most important step is to raise the EEM before you are deep into underwriting. It is far easier to build the improvement into the loan up front than to add it late. Here is the sequence I walk buyers through:

- Flag it at pre-approval. Tell your VA-approved lender you want to use an Energy Efficient Mortgage so they structure the loan for it from the start.

- Get contractor bids. Have a licensed contractor itemize the upgrade and cost. For amounts over 3,000 dollars, arrange an energy audit that documents the projected savings.

- Add it to the loan. Your lender increases the loan amount by the approved improvement cost, confirming the savings-versus-payment test where required.

- Close, then complete the work. The improvement funds are held in a VA escrow account and released to the contractor once the work is finished and verified, typically within a set window after closing.

A Realtor who knows the program keeps this on track, coordinating the bid, the appraisal, and the escrow timeline so nothing stalls your closing. That coordination is exactly what I handle for the veteran buyers I represent through the Serve and Save program.

Can You Stack CPS Energy Rebates on Top of a VA EEM?

San Antonio buyers have a local advantage many other markets do not. CPS Energy runs efficiency rebate programs that can offset part of the cost of a new high-efficiency AC, added insulation, and similar upgrades. Because the EEM finances the work and the rebate reimburses part of the cost, the two can work together. Always confirm current rebate amounts and eligibility with CPS Energy and check federal options through ENERGY STAR, and verify EEM rules through the VA home loans program.

If you also want to lower your tax picture on the home you buy, my VA seller concessions guide and rural VA loan guide cover related ways to reduce your costs.

About the Author: Christopher Beal

Christopher Beal is a U.S. Army veteran and the broker-owner of Veteran Real Estate San Antonio: The Beal Group at eXp Realty. He holds TREC license #723559 and the Military Relocation Professional (MRP) certification, and he is a member of the Veterans Association of Real Estate Professionals (VAREP). Over his career he has closed more than 306 homes and over 117 million dollars in volume, earning recognition as a San Antonio Business Journal Top 25 Residential Real Estate Agent, a six-time eXp ICON agent, and a Five Star Professional. Christopher specializes in guiding military and veteran buyers and sellers through PCS moves, VA loans, and new-construction purchases across San Antonio and the surrounding counties of Bexar, Comal, Guadalupe, Kendall, Medina, and Bandera. Through his Serve and Save program, he reduces closing costs for the military families he represents.

Explore More Resources

Frequently Asked Questions About the VA Energy Efficient Mortgage

What is a VA Energy Efficient Mortgage?

It is an add-on to a VA purchase or refinance loan that finances the cost of energy-saving home improvements. It is not a separate loan or a second application; the approved improvement cost is added to your VA loan balance and closes when your loan closes.

How much can I finance with a VA EEM in 2026?

Generally up to 6,000 dollars. Up to 3,000 dollars usually needs only a contractor bid. From 3,001 to 6,000 dollars you must show that the projected energy savings exceed the increase in your monthly payment. Above 6,000 dollars requires a full cost-effectiveness analysis and lender and VA approval.

What improvements qualify for a VA EEM?

Permanently installed upgrades that reduce energy use, such as high-efficiency HVAC systems, attic insulation and radiant barrier, solar water heaters, energy-efficient windows, air sealing and weatherization, and heat-pump water heaters. Cosmetic remodeling and pools do not qualify.

How much will 6,000 dollars add to my monthly payment?

At 2026 rates over a 30-year term, roughly 37 dollars a month. If the energy the upgrade saves on your CPS Energy bill is more than that, you come out ahead each month, which is often the case in San Antonio's cooling-heavy climate.

Do I need an energy audit for a VA EEM?

Not for the smallest tier. Up to 3,000 dollars typically requires only an itemized contractor bid. Between 3,001 and 6,000 dollars you generally need an energy audit or documentation showing the savings exceed the payment increase. Your lender will tell you exactly what is required.

Can I use an EEM on a refinance, or only a purchase?

You can use it on a VA purchase loan or a VA refinance, including in many cases an Interest Rate Reduction Refinance Loan. Ask your VA-approved lender how the EEM applies to your specific transaction.

When does the improvement work get done?

Usually after closing. The improvement funds are held in a VA escrow account and released to your contractor once the work is completed and verified, typically within a set window. Your lender and Realtor should coordinate the timeline so it does not delay your closing.

Can I combine a VA EEM with CPS Energy rebates?

Often yes. CPS Energy rebates are separate from your mortgage, so financing an upgrade through an EEM generally does not disqualify you from a local rebate. Confirm current rebate amounts and eligibility directly with CPS Energy.

Does the EEM require a down payment on the improvement?

No. Like the base VA loan, the EEM does not require a down payment on the financed improvement amount. That is a major reason it works well for buyers who are cash-tight after a move.

Will the upgrades increase my home's appraised value?

They can, though the primary benefit is lower energy use and greater comfort. Energy-efficient features are increasingly valued by buyers, which can help at resale, but do not count on a dollar-for-dollar value bump; treat the savings as the main return.

Do not leave a valuable VA benefit on the table. If you are buying a San Antonio home that needs an AC, insulation, or windows, I will help you and your lender build the Energy Efficient Mortgage into the deal so you close comfortable and keep your cash.

Call Christopher Beal at (210) 882-8583, email [email protected], or visit veteranrealestatesa.com to get started.

Veteran Real Estate San Antonio: The Beal Group. Serving those who served, and saving them money at the closing table through the Serve and Save program.

Categories

- All Blogs (310)

- Alamo Heights (4)

- awards (2)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (71)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (23)

- Market Trends (3)

- Market Update (13)

- Military Relocation (93)

- Military Retirement (3)

- Mortgage (14)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (25)

- Real Estate (31)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (63)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (21)

- VA Home Loans (22)

- VA Loans (32)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts