VA Loan Pre-Approval in San Antonio 2026: Step-by-Step Guide for Military Buyers

Last Updated: April 14, 2026

VA Loan Pre-Approval in San Antonio 2026: Step-by-Step Guide for Military Buyers

By Christopher Beal — U.S. Army Veteran | REALTOR, eXp Realty | MRP | VAREP Member | TREC #723559 | SABJ Top 25 3× Winner (#13 2024, #14 2025, #20 2026) | PT50 3× | ICON 6× | Five Star 2026 | 2× RateMyAgent AOTY | Real Producers Top 100 | 306+ families served | $117M+ career volume

Key Takeaways

- VA loan pre-approval can be completed in 24–48 hours with documents ready

- BAH is counted as income (grossed up 25%), significantly increasing your buying power

- The 2026 VA loan limit for Bexar County (San Antonio) is $832,750

- You can begin pre-approval before PCS orders arrive — 60–90 days early is ideal

- Pre-approval differs from pre-qualification — sellers in San Antonio require pre-approval letters

- The Serve & Save program reduces closing costs for eligible veterans — call (210) 882-8583

Getting a VA loan pre-approval is the single most important step a veteran or active-duty service member can take before searching for homes in San Antonio. It establishes your exact buying power, signals to sellers that you are a serious buyer, and often reveals issues — with credit, income documentation, or COE eligibility — that are far easier to address before you've fallen in love with a house. This guide walks through every step of the VA loan pre-approval process as it works in San Antonio's 2026 real estate market, including how PCS orders factor in and how BAH supercharges your qualifying income.

Christopher Beal has guided 306+ military families through home purchases in San Antonio. As a U.S. Army veteran himself, MRP-certified REALTOR, and VAREP member, he understands the unique timeline pressures, entitlement questions, and lender coordination that VA loan buyers face. Visit veteranrealestatesa.com/va-home-loans or call (210) 882-8583 to connect.

What Is the Difference Between VA Loan Pre-Approval and Pre-Qualification?

Pre-qualification and pre-approval are two distinct stages in the mortgage process, and confusing them can cost you a home purchase in San Antonio's competitive market. Pre-qualification is an informal, unverified estimate. You tell a lender your approximate income, debts, and assets — they run no credit check and verify nothing — and they tell you approximately what you might qualify for. This takes 10–15 minutes and produces a letter with limited credibility.

Pre-approval is a formal, verified process. The lender pulls your credit report (hard inquiry), reviews your income documents (LES or W-2s, tax returns), verifies your employment, and confirms your Certificate of Eligibility (COE). The output is a written conditional commitment letter stating that you are approved to borrow up to a specific amount, subject to a satisfactory appraisal and no material changes in your financial situation. This letter is what San Antonio sellers require — and many listing agents will not present an offer to their client without it.

In San Antonio's 2026 market, where well-priced homes in JBSA-area neighborhoods like Alamo Ranch (78253), Schertz (78154), and Converse (78109) can receive multiple offers within days of listing, walking in with a solid VA pre-approval letter from a reputable lender positions you to compete and win. Always get the full pre-approval, not just a quick pre-qualification.

Step 1: How Do I Get My VA Certificate of Eligibility (COE)?

The Certificate of Eligibility (COE) is the VA's official document confirming that you have served the minimum service requirements to use your VA home loan benefit. Without it, no lender can issue a VA loan. Fortunately, obtaining your COE is faster and easier than most veterans realize — often accomplished in minutes online.

There are three ways to get your COE. Option 1 (fastest): VA.gov eBenefits portal. Log in at VA.gov and navigate to the home loan COE section. For active-duty service members and most veterans, the system pulls eligibility automatically from DoD records and generates the COE instantly. Option 2 (fast): Through your VA-approved lender. Most VA-approved lenders have access to the VA's ACE (Automated Certificate of Eligibility) system and can pull your COE electronically as part of the application process — no separate step required. Option 3 (slow): By mail. Submit VA Form 26-1880 to the VA Eligibility Center in Winston-Salem, NC. Allow 4–6 weeks. This method is a last resort.

Documents needed to support your COE by service type:

- Active duty: Statement of service signed by your unit's adjutant or commanding officer (1st Sergeant or higher), showing name, SSN, date of birth, entry date, duration of any lost time, and the name of the command

- Veteran (honorably discharged): DD-214, Certificate of Release or Discharge from Active Duty — specifically Member Copy 4, which includes the Character of Service block

- National Guard / Reserve: NGB Form 22 (for Guard) or Points Statement (for Reserve) plus evidence of activation on federal orders (Title 10 service) if applicable

- Surviving spouse: Veterans' service records, your marriage certificate, and the veteran's death certificate

If you're PCSing to San Antonio and haven't obtained your COE yet, Christopher Beal's team can connect you with VA-approved lenders who pull COEs electronically in minutes. See the full COE guide at veteranrealestatesa.com/va-home-loans.

Step 2: How Do I Choose the Right VA-Approved Lender in San Antonio?

Not all lenders who claim to offer VA loans are equally experienced or competitive. The right lender can mean the difference between a smooth 30-day closing and a frustrating 60-day ordeal that costs you your dream home. In San Antonio's military-heavy market, working with a lender who processes high volumes of VA loans is essential — they know the VA appraisal process, Minimum Property Requirements (MPR), and the nuances of military income documentation that trip up less experienced underwriters.

Key factors to evaluate when selecting a VA lender: (1) VA loan volume. Ask how many VA loans the lender closed in the past 12 months. A lender doing 50+ VA loans per year in San Antonio has refined processes and strong relationships with the VA Regional Loan Center (RLC). (2) Rate and fee transparency. VA loans have specific fee structures including the VA Funding Fee (1.25%–3.3% of the loan amount, depending on down payment and whether it's a first or subsequent use). Request a Loan Estimate on day one — federal law requires lenders to provide this within 3 business days of application. (3) Military-specific expertise. Look for lenders who understand LES income, military allowances (BAH, BAS, flight pay), PCS-related income gaps, and concurrent-eligibility situations (using VA loan while still having a prior VA loan active).

(4) Local presence and closing speed. A local San Antonio lender who can close in 21–30 days is more competitive in multiple-offer situations than a national call-center lender promising the same rate but operating on 45-day timelines. (5) VAREP-affiliated lenders. The Veterans Association of Real Estate Professionals (VAREP), of which Christopher Beal is a member, maintains a network of veteran-friendly lending partners who specialize in VA loan products and military buyer needs. Ask Christopher for a referral — he works with several lenders in San Antonio who consistently close VA loans on schedule.

Step 3: What Documents Do I Need for VA Loan Pre-Approval?

Document preparation is the step where most VA loan applications slow down unnecessarily. Gathering everything before contacting the lender cuts the pre-approval timeline from days to hours. Here is the complete document checklist for VA loan pre-approval in 2026:

| Document | Who Needs It | Notes |

|---|---|---|

| Certificate of Eligibility (COE) | All VA borrowers | Lender can pull via ACE system |

| Most recent LES (Leave & Earnings Statement) | Active duty | Print from MyPay; shows base pay, BAH, BAS |

| Last 2 years W-2s | Veterans, retirees | From current and prior employers |

| Last 2 years federal tax returns (1040) | Self-employed, multiple income sources | All schedules including Schedule C, E |

| 2 months bank statements (all accounts) | All borrowers | All pages, checking and savings |

| Government-issued photo ID | All borrowers | CAC card, driver's license, or passport |

| Social Security number | All borrowers | For credit report pull |

| DD-214 (if veteran) | Separated veterans | Member Copy 4 preferred |

| PCS Orders (if available) | Active duty with incoming orders | Confirms duty station for BAH calculation |

| Retirement Award Letter | Military retirees | Shows monthly retirement pay amount |

| VA Disability Award Letter | Veterans with VA disability | VA disability income is tax-free + grossed up 25% |

Important note on the LES: Your Leave and Earnings Statement is the primary income document for active-duty borrowers and is the military equivalent of a pay stub. It is accessible via MyPay.dfas.mil. The LES shows your base pay, BAH (Basic Allowance for Housing), BAS (Basic Allowance for Subsistence), flight pay, hazardous duty pay, and other allowances — all of which lenders use to calculate your qualifying income. Print and save the most recent month's LES and the LES from the same month the prior year to document 12-month income continuity.

Step 4: How Do I Submit a VA Loan Pre-Approval Application?

Once documents are assembled, submitting your VA loan pre-approval application is straightforward. Most VA-approved lenders in San Antonio offer online portals where you upload documents securely and complete the Uniform Residential Loan Application (URLA, also known as Fannie Mae Form 1003). The lender's loan officer will contact you, typically within 2–4 hours on business days, to discuss your file and answer questions.

The lender will run a tri-merge credit report that pulls your score from all three bureaus (Equifax, Experian, TransUnion) and uses the middle score for qualification purposes. While the VA itself has no official minimum credit score requirement, most VA-approved lenders set their own overlay of 580–620 minimum, with 640 or higher preferred for best rates and easiest underwriting. If your score falls short, see the denial reasons and fixes section below.

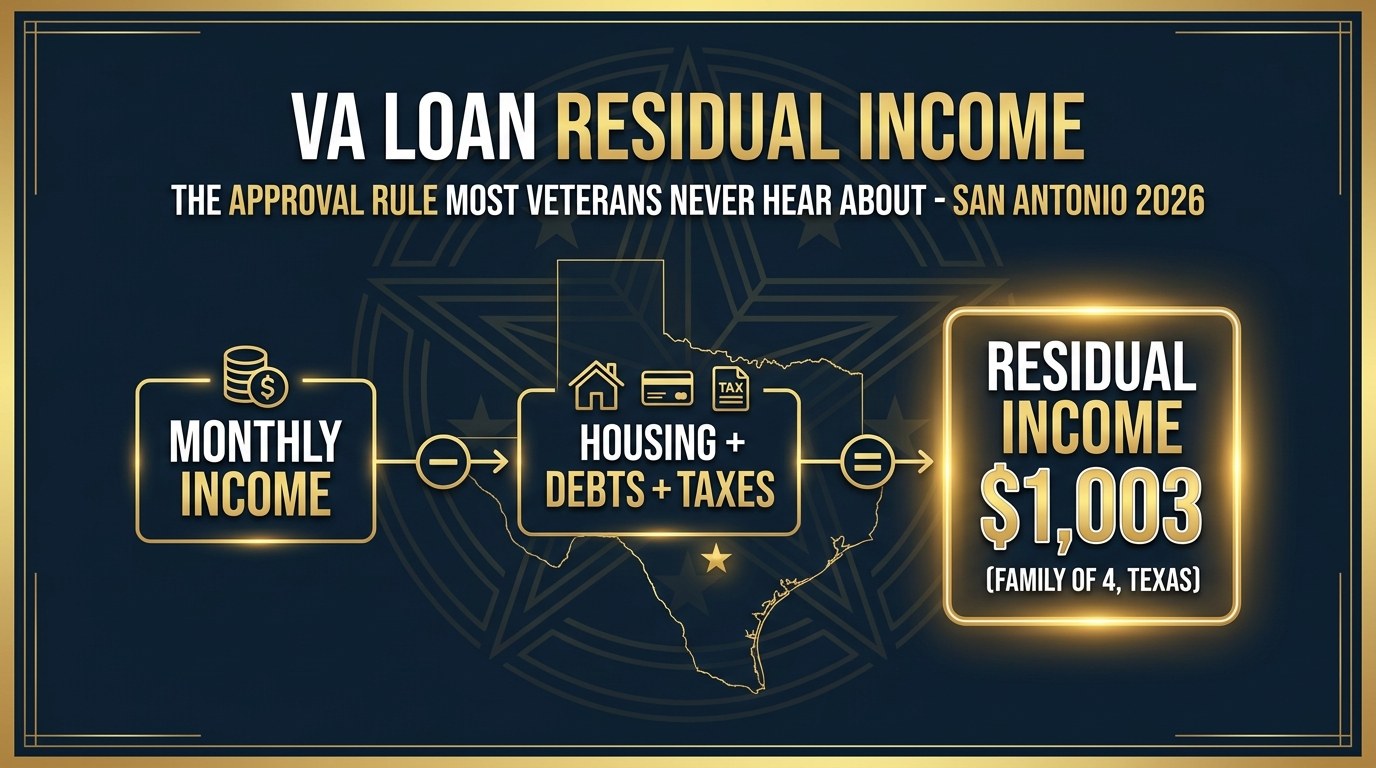

During the application, the lender will calculate your debt-to-income (DTI) ratio — total monthly debt obligations (car payments, student loans, credit cards, existing mortgages) divided by gross monthly income. The VA guideline is a maximum 41% DTI, though many lenders approve loans up to 50% DTI with strong compensating factors (large cash reserves, high credit score, significant residual income above VA's minimum thresholds). For a San Antonio-area buyer, the VA residual income requirement is $1,003–$1,117/month for a family of 1–5, depending on loan size, which is typically easy for active-duty households to meet given BAH and BAS allowances.

Step 5: What Does a VA Loan Pre-Approval Letter Look Like — and What Comes Next?

A VA loan pre-approval letter is a formal written document on lender letterhead that states: your name and co-borrower's name (if applicable), the loan type (VA), the maximum approved loan amount, the interest rate environment in which the approval was made, the approval expiration date (typically 60–90 days), and any conditions that must be satisfied (such as property appraisal, updated pay stubs if more than 30 days old, or insurance documentation).

A strong pre-approval letter also mentions that the lender has verified income, assets, employment, and credit — distinguishing it from a mere pre-qualification. When Christopher Beal submits an offer on your behalf, he includes your pre-approval letter and notes your VA eligibility in the offer to the seller. VA buyers have a reputation in some circles for longer timelines, but an experienced VA realtor counteracts that perception with a well-organized offer package and a lender who is known in the local market for closing on time.

What happens after you receive the letter: Your pre-approval is valid for 60–90 days in most cases. During that window, begin your home search in earnest. Once you're under contract on a property, the lender orders the VA appraisal, the loan moves into formal underwriting, and you work toward a closing date typically 30–45 days out. Communicate any changes to your financial situation (new debts, job changes, large deposits) to your lender immediately — undisclosed changes can delay or jeopardize the loan.

How Does BAH Count as Income for VA Loan Pre-Approval?

Basic Allowance for Housing (BAH) is one of the most important income components for active-duty VA loan borrowers, and understanding how it's calculated for qualification purposes directly impacts your maximum purchase price. BAH is a non-taxable housing allowance paid to service members who do not live in on-base housing. For San Antonio (JBSA), 2026 BAH rates reflect a 2.9% decrease from 2025 rates, ranging from approximately $1,494/month for an E-1 without dependents to $2,538/month for an O-4 with dependents.

Because BAH is non-taxable, VA-approved lenders gross it up by 25% when calculating qualifying income. This means: a service member receiving $2,000/month in BAH has that BAH treated as $2,500/month in qualifying income on the loan application. For an E-5 receiving $3,500/month in base pay plus $2,200/month in BAH, the lender calculates qualifying income as $3,500 + ($2,200 × 1.25) = $3,500 + $2,750 = $6,250/month in qualifying income. This gross-up significantly expands buying power compared to a civilian borrower with the same actual take-home pay.

BAS (Basic Allowance for Subsistence, ranging $387–$452/month in 2026) and other non-taxable allowances such as flight pay and hazardous duty pay are similarly grossed up. Active-duty service members PCSing to San Antonio typically discover their qualifying income is higher than expected once a VA-experienced lender correctly calculates all allowances. This is another reason why working with a lender and realtor who specialize in VA loans — rather than general real estate and mortgage professionals — directly improves outcomes for military buyers.

How Does Pre-Approval Work If You're PCSing to San Antonio and Still at Your Current Duty Station?

PCSing military buyers face a unique challenge: you need to purchase in a city you may never have visited, on a timeline dictated by orders, potentially while still serving at your current installation hundreds or thousands of miles away. The good news is that VA loan pre-approval works effectively in this scenario, and starting the process 60–90 days before your report date is strongly recommended.

Here is how the process works when PCSing to JBSA in San Antonio. First, obtain your PCS orders as soon as they arrive — do not wait. Orders are the legal document that triggers your BAH entitlement at the new duty location (JBSA rate vs. your current base rate). They also provide the lender with your new report date, which affects the mortgage timeline. Second, contact a VA-approved lender in San Antonio — even before visiting the city. Submit your LES, orders, and other documents. The lender calculates your income using the San Antonio BAH rate (which may differ from your current station's rate), runs your credit, and issues a pre-approval based on your finances and the San Antonio market.

Third, connect with Christopher Beal. As an MRP-certified agent who works with remote military buyers constantly, he facilitates virtual home tours, coordinates access for spouses or family members visiting before the service member arrives, and has closed transactions where the buyer did their entire search remotely. His team provides video walkthroughs, neighborhood driving tours, and detailed written reports on schools, commute times to JBSA gates, and neighborhood-specific conditions. Reach him at veteranrealestatesa.com/military-relocation or (210) 882-8583.

PCS timeline best practices: Start VA pre-approval 60–90 days before your report date. Begin remote home search 45–60 days out. Plan an in-person scouting trip (or have family members go) 30–45 days out if possible. Be under contract 30+ days before your report date to close on or near arrival. This timeline allows a standard 30–45 day VA loan closing without the stress of closing the same week you're driving across the country with a household goods shipment behind you.

What Are the Most Common VA Loan Pre-Approval Denial Reasons — and How Do You Fix Them?

A VA loan pre-approval denial is not a permanent verdict. Every common denial reason has a corresponding fix — and in most cases, a determined borrower can address the issue and re-apply within 3–12 months. Understanding the most frequent causes of denial allows you to check your own situation proactively and take corrective action before even applying.

1. Low credit score. Most VA lenders require 580–620 minimum; 640+ is preferred. Fix: Pay down revolving credit card balances to below 30% of each card's limit (this is the fastest credit score boost), dispute any errors on your credit report at AnnualCreditReport.com, and avoid opening new credit accounts for 6 months before applying. Each on-time payment improves your score gradually; the biggest quick-win is reducing utilization.

2. Debt-to-income ratio too high. VA guideline is 41% max DTI; some lenders approve to 50% with compensating factors. Fix: Pay off or pay down installment loans (car payments, personal loans) and revolving debt (credit cards). Even paying off a single $300/month car note can drop your DTI by 4–5 percentage points, potentially qualifying you for a significantly higher home purchase price. Do not take on any new debt (furniture, appliances, new car) during the pre-approval process.

3. Insufficient service history for COE. The VA requires 90 days of continuous active service during wartime, 181 days during peacetime, or 6 years in the Reserves or Guard. Fix: Review your service history through eBenefits. If you were separated before meeting service minimums due to a service-connected disability, you may still qualify. Contact the VA Regional Loan Center directly to review your specific situation.

4. Recent bankruptcy or foreclosure. Chapter 7 bankruptcy: 2-year waiting period from discharge date before VA loan eligibility. Chapter 13 bankruptcy: 1-year waiting period with 12 months of on-time trustee payments and court approval. Foreclosure: Generally 2 years from completion date, though individual lender overlays may require longer. Fix: Wait out the required period while rebuilding credit aggressively.

5. Employment gaps or unstable income history. Lenders want to see 2 years of consistent income history. Gaps in employment, frequent job changes, or recent transitions from military to civilian employment can create documentation challenges. Fix: Provide detailed written explanations for any gaps. VA lenders understand that military service can create employment gaps (transition leave, VA vocational rehabilitation periods, etc.) and often have more flexibility than conventional lenders if the circumstances are clearly documented.

How Does the Serve & Save Program Reduce Closing Costs for VA Buyers in San Antonio?

Even with a VA loan's zero-down-payment benefit, closing costs remain a real expense for San Antonio home buyers. Typical VA loan closing costs in 2026 include the VA Funding Fee (1.25%–3.3% of the loan amount, though waived for veterans with service-connected disabilities), lender origination fees (capped at 1% by VA rules), title insurance, escrow fees, prepaid homeowners insurance, and prepaid property tax escrow — adding up to $8,000–$15,000 on a $300,000 purchase.

The Serve & Save program at Veteran Real Estate San Antonio reduces closing costs for eligible veterans based on years of service. The program provides 1% per year of service, up to a maximum of 6%. For a veteran with 6+ years of service purchasing a $300,000 home, this can represent $18,000 in closing cost savings — a substantial reduction that makes the transition to homeownership in San Antonio far more accessible. This is not "cash back" or a rebate — it is a direct reduction in what you pay at the closing table, structured to be VA-compliant.

To combine VA loan pre-approval with Serve & Save planning, contact Christopher Beal early in your search process — ideally at the same time you begin working with a VA lender. The earlier he understands your service history and home price target, the better he can calculate your potential closing cost reduction and help you budget for the transaction. Visit veteranrealestatesa.com/serve-and-save for full program details or call (210) 882-8583.

Ready to Start Your VA Loan Pre-Approval?

Christopher Beal — U.S. Army Veteran, MRP-certified, VAREP member — guides military buyers through VA loan pre-approval and home purchase in San Antonio. The Serve & Save program reduces closing costs for eligible veterans.

Call (210) 882-8583 or visit veteranrealestatesa.com/va-home-loans

Ask AI About This Topic

Get instant answers from AI about VA loan pre-approval for military buyers in San Antonio

Frequently Asked Questions

How long does VA loan pre-approval take in San Antonio?

VA loan pre-approval can be completed in as little as 24–48 hours when you have all required documents ready. The process involves submitting your application, Certificate of Eligibility (COE), income documents (LES, W-2s, tax returns), and bank statements to a VA-approved lender. If your COE is already obtained through the VA's eBenefits portal, the lender can typically issue a pre-approval letter within one to two business days. Complex income situations (self-employment, multiple sources) may require 3–5 business days.

What documents do I need for VA loan pre-approval?

For VA loan pre-approval you need: (1) Certificate of Eligibility (COE) — obtain through VA.gov eBenefits or ask your lender to pull it, (2) most recent Leave and Earnings Statement (LES) for active-duty, or last 2 years W-2s and tax returns for veterans, (3) 2 months of bank statements showing assets, (4) government-issued photo ID, (5) Social Security number for credit check, and (6) for recent separations, DD-214. If you have rental income, 2 years of Schedule E tax forms are also required.

Does BAH count as income for VA loan pre-approval?

Yes. Basic Allowance for Housing (BAH) counts as qualifying income for VA loan pre-approval. Because BAH is non-taxable, VA-approved lenders gross it up by 25% when calculating qualifying income — meaning $2,000/month BAH counts as $2,500 in qualifying income. This significantly increases your buying power compared to a civilian buyer with equivalent base pay. BAH rates in San Antonio (JBSA) for 2026 range from approximately $1,500 to $2,500+ per month depending on rank and dependent status.

What is the difference between VA loan pre-qualification and pre-approval?

Pre-qualification is an informal estimate of what you might be able to borrow, based on self-reported income and assets — no documentation or credit check required. Pre-approval is a formal lender review using verified income documents, credit report, and employment verification that results in a written conditional commitment to lend up to a specific dollar amount. In the San Antonio real estate market, sellers expect a pre-approval letter — not just a pre-qualification — before accepting an offer. Always get a full pre-approval before house hunting.

Can I get VA loan pre-approval before PCS orders arrive?

Yes. You can begin the VA loan pre-approval process before receiving official PCS orders. Lenders will pre-approve you based on your current duty station income, credit, and assets. Once PCS orders arrive, you provide them to the lender, who updates the pre-approval to reflect your new duty location and applicable BAH. Starting pre-approval early — 60–90 days before your anticipated move — gives you time to address any credit or documentation issues without rushing. Christopher Beal at Veteran Real Estate San Antonio works with buyers across the country who are PCSing to JBSA.

What are the most common reasons VA loan pre-approval is denied?

The most common reasons VA loan pre-approval is denied are: (1) credit score too low — while the VA has no official minimum, most lenders require 580–620 minimum, with 640+ preferred; (2) debt-to-income ratio too high — VA guideline is 41% maximum DTI, though some lenders approve up to 50% with compensating factors; (3) insufficient service history to qualify for a COE; (4) recent bankruptcy or foreclosure (typically 2-year waiting period after Chapter 7, 1 year for Chapter 13); and (5) gaps in employment history. All of these issues are fixable — working with an MRP-certified agent and experienced VA lender helps you identify and resolve them before they become problems.

How do I get my VA Certificate of Eligibility (COE)?

You can obtain your VA Certificate of Eligibility three ways: (1) Online through VA.gov eBenefits portal — fastest method, often instant for active-duty and recent veterans; (2) Through your VA-approved lender — most lenders can pull your COE electronically through the VA's ACE system within minutes; (3) By mail — submit VA Form 26-1880 to the VA Eligibility Center (slowest, takes 4–6 weeks). For active-duty service members, you need a statement of service signed by your commanding officer. For veterans, your DD-214 is the primary document. Full guide at veteranrealestatesa.com/va-home-loans.

What VA loan amount can I qualify for in San Antonio in 2026?

In 2026, the VA loan conforming limit for San Antonio (Bexar County) is $832,750. For loans above this amount (jumbo VA loans), lenders may require a down payment. For loans at or below $832,750, eligible veterans with full entitlement can purchase with zero down payment and no VA-required PMI. Your actual purchase price is determined by your income, credit, and debt-to-income ratio. An E-5 with dependents receiving approximately $2,200/month BAH plus $3,500 base pay can typically qualify for a home purchase in the $300,000–$400,000 range.

What happens after I receive my VA loan pre-approval letter?

Once you have your VA pre-approval letter, you're ready to start house hunting with a clear price limit and proof of buying power. Your MRP-certified agent will schedule showings for properties that meet your criteria, help you write offers, and negotiate on your behalf. When your offer is accepted, the lender orders a VA appraisal (which includes the VA's Minimum Property Requirements review), and the loan moves into underwriting. The full process from accepted offer to closing typically takes 30–45 days for VA loans in San Antonio. The Serve & Save program reduces closing costs for eligible veterans — ask Christopher Beal for details.

Is VA loan pre-approval free?

Yes. VA loan pre-approval is free. Reputable VA-approved lenders do not charge application fees or pre-approval fees. The only cost you may incur upfront is if the lender charges for the credit report pull (typically $10–$25), though many waive this. Avoid any lender that charges significant upfront fees for a pre-approval. Once your loan proceeds to full underwriting after an accepted offer, you will pay for the VA appraisal (typically $500–$800 in San Antonio) and may have closing costs — though the Serve & Save program reduces these for eligible veterans.

Start Your VA Loan Pre-Approval Today

Christopher Beal — U.S. Army Veteran | REALTOR, eXp Realty | MRP | VAREP | SABJ Top 25 #20 (2026) | 306+ families served | $117M+ volume

The Serve & Save program reduces closing costs for eligible veterans based on years of service.

(210) 882-8583 | Military Relocation | Read Reviews | About Christopher

Categories

- All Blogs (323)

- Alamo Heights (4)

- awards (3)

- Best Neighborhoods in San Antonio (14)

- Buyer (13)

- Buyer Education (77)

- Community Events (4)

- Hill Country (16)

- JBSA (34)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (24)

- Market Trends (5)

- Market Update (14)

- Military Relocation (97)

- Military Retirement (3)

- Mortgage (18)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (30)

- Real Estate (33)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (40)

- San Antonio Real Estate (67)

- San Antonio, Veterans Resources, VA Loans (5)

- Seller (27)

- VA Home Loans (28)

- VA Loans (33)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (39)

Recent Posts