What Credit Score Do You Need for a VA Loan in San Antonio? (2026 Guide)

LAST UPDATED: MAY 29, 2026 | BY CHRISTOPHER BEAL, U.S. ARMY VETERAN & REALTOR

What Credit Score Do You Need for a VA Loan in San Antonio? (2026 Guide)

Key Takeaways

- The Department of Veterans Affairs sets no minimum credit score for a VA loan. Individual lenders set their own floors, called overlays.

- Most San Antonio VA lenders want a 620 middle score for their best pricing, many will approve at 580, and a smaller group works with scores in the 500s through manual underwriting.

- Your credit score mostly controls your interest rate, not whether you qualify. VA residual income and debt-to-income usually matter more for approval.

- A disabled-veteran funding fee waiver, BAH counted as income, and zero down payment make San Antonio one of the strongest VA markets in Texas even for mid-tier scores.

- Raising a score 20 to 40 points before you lock can save thousands over the life of a $350,000 loan, and there are fast, legitimate ways to do it.

In This Guide

- Does the VA require a minimum credit score?

- What credit score do San Antonio lenders actually want in 2026?

- How does your credit score change your VA loan rate?

- Why do residual income and DTI matter more than your score?

- Can you get a VA loan with a score under 620 in San Antonio?

- How can you raise your score before you buy near JBSA?

- Frequently asked questions

Does the VA Require a Minimum Credit Score?

This is the single biggest misconception I correct in San Antonio. Buyers walk into a consultation convinced that a 640 or 680 is a hard wall set by the government. It is not. The VA guarantees a portion of each loan, which protects the lender against loss, and that guarantee is why VA loans exist with no down payment and no monthly mortgage insurance. Because the VA absorbs that risk, it leaves the credit decision to the lender.

What that means in practice: two lenders can look at the exact same veteran with the exact same 590 score and reach opposite answers. One declines, the other approves. The VA never changed its rules between those two phone calls. The lenders simply have different risk appetites, and those internal rules are what the industry calls overlays.

The official VA guidance, published at va.gov, focuses on satisfactory credit history and the ability to repay rather than a single magic number. A clean recent payment history can carry more weight with an underwriter than a high score dragged down by one old medical collection.

What Credit Score Do San Antonio Lenders Actually Want in 2026?

Lenders pull all three bureaus and use your middle score. They order Equifax, Experian, and TransUnion, line up the three numbers, and use the middle one, not the average and not the highest. If you and a co-borrowing spouse apply together, the lender typically uses the lower of the two middle scores. Knowing this one rule keeps San Antonio couples from being surprised at the rate lock.

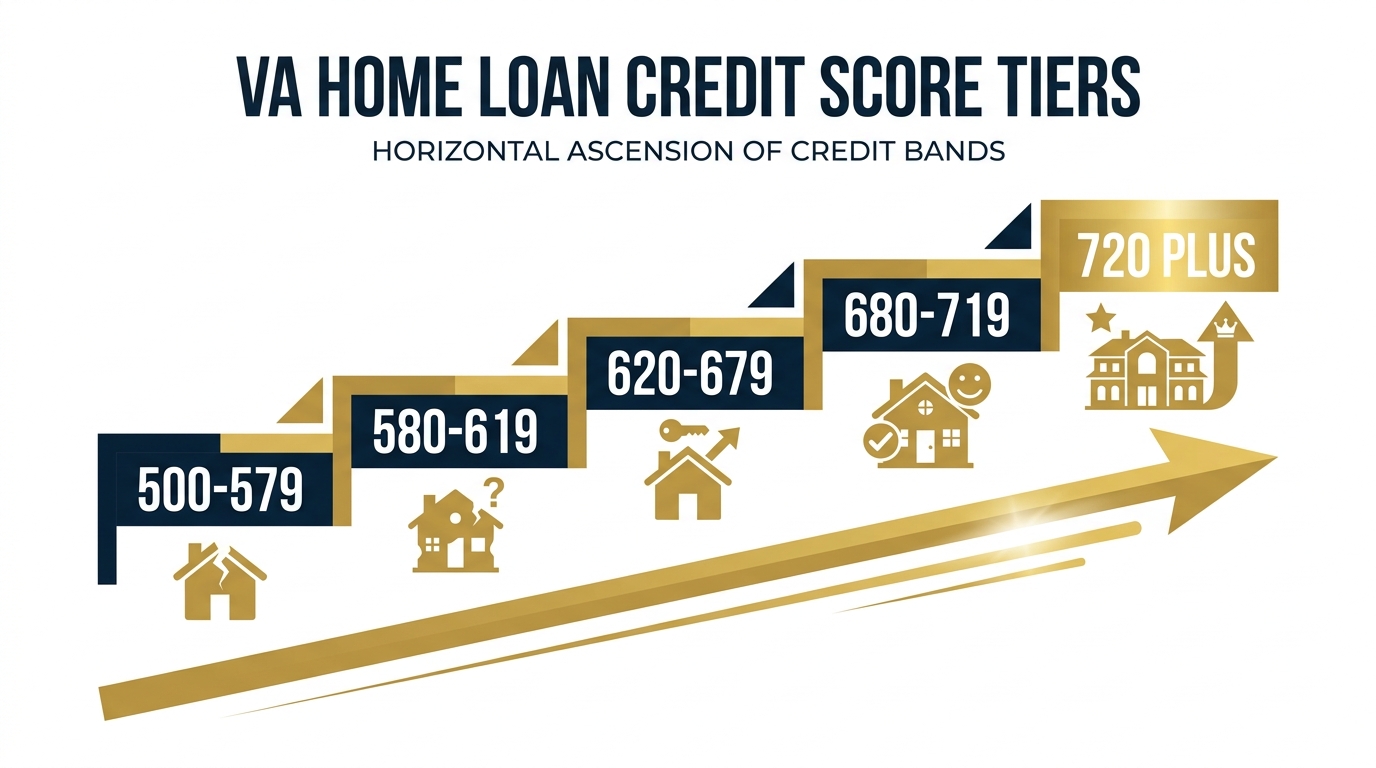

Here is how the common bands break down across the lenders my clients use most around JBSA-Lackland, JBSA-Randolph, and Fort Sam Houston:

| Middle Credit Score | Typical San Antonio Lender Treatment | What to Expect |

|---|---|---|

| 720 and up | Approved by virtually every VA lender | Best available rate, automated approval, smoothest file |

| 680 to 719 | Strong approval everywhere | Near-best pricing, minimal conditions |

| 620 to 679 | Most common lender floor for top pricing | Solid rate, fully automated underwriting in most cases |

| 580 to 619 | Many VA lenders approve, some add overlays | Slightly higher rate, may need a few compensating factors |

| 500 to 579 | VA specialists only, manual underwriting | Stronger residual income and reserves usually required |

Source: Composite of VA lender overlay guidelines used by San Antonio buyers, 2026. Individual lender thresholds change and should be confirmed in writing during pre-approval.

How Does Your Credit Score Change Your VA Loan Rate?

Credit score and rate are linked, but VA pricing is gentler than conventional. Conventional loans use loan-level price adjustments that punish lower scores hard. VA loans do not carry those same adjustments, so the penalty for a lower score is real but softer. Still, in a 2026 rate environment that has stayed elevated, every fraction of a point matters more than it did a few years ago.

Consider a $350,000 VA purchase, roughly the price of a well-kept four-bedroom in Cibolo, Converse, or the JBSA-Lackland northwest corridor. A rate that is half a point higher because of a 600 score instead of a 700 score adds well over a hundred dollars to the monthly payment and more than $40,000 in interest across 30 years. That is the cost of skipping a few months of credit cleanup.

You can track where market rates are sitting using the Freddie Mac Primary Mortgage Market Survey at freddiemac.com, but remember that the survey reflects conventional averages. Your VA quote depends on your score band, the lender, and whether you buy down points.

This is also why I always tell buyers weighing timing to read my buy now or wait decision framework for San Antonio before locking. The score-to-rate math is part of that larger decision.

Why Do Residual Income and DTI Matter More Than Your Score?

Residual income is the VA's secret weapon, and most buyers have never heard of it. Instead of looking only at ratios, the VA requires that a household have a minimum amount of discretionary cash left over each month based on family size and region. For the South region that covers Texas, a family of four typically needs several hundred dollars of residual income remaining after all obligations. A veteran with a 590 score who clears the residual test comfortably often looks safer to an underwriter than a 660 borrower stretched thin.

Debt-to-income, or DTI, is the second lever. VA loans are famous for tolerating higher DTI than conventional loans, sometimes well past 41 percent, precisely because the residual income test backstops it. In San Antonio, where BAH for JBSA service members counts as stable income, a lot of buyers qualify at numbers that would scare a conventional underwriter.

Compensating factors round out the picture. Cash reserves, a long stable job history, a conservative payment shock from your current rent, and a clean recent twelve months all help an underwriter say yes. If you are stacking a VA loan on top of an existing one, my guide to using your VA loan more than once in San Antonio walks through how entitlement and these factors interact.

Can You Get a VA Loan With a Score Under 620 in San Antonio?

Manual underwriting is the path for lower scores and thin credit files. When an automated system will not issue an approval, a human underwriter reviews the full file by hand. They look at your rent payment history, utility and phone records, residual income, reserves, and the story behind any derogatory marks. A single deployment-era late payment from 2021 reads very differently than a current pattern of missed bills.

The trade-off is documentation. Manual files ask for more, including a clean twelve-month housing payment history and often two months of mortgage payments in reserve. They take a little longer to clear. But they close, and I have walked first-time buyers near Randolph through exactly this process when their score sat at 585.

If your score is being held down by errors rather than real debt, dispute them first. The Consumer Financial Protection Bureau explains your dispute rights at consumerfinance.gov, and a single corrected reporting error can lift a middle score across the 620 line in a matter of weeks.

How Can You Raise Your Score Before You Buy Near JBSA?

Credit utilization is the fastest lever you control. The ratio of your card balances to your limits is a major scoring factor that updates monthly. Paying a $4,000 balance down to under $1,000 on a $5,000 limit card can move a score double digits in a single billing cycle. If you are 90 days from a PCS-timed purchase, this is where to start.

Next, pull your reports and hunt for errors. You are entitled to free reports, and mistakes are common, from accounts that are not yours to paid collections still showing a balance. Dispute them in writing and keep records.

Then protect what you have. Do not open a new car loan or store card in the months before you buy, and do not close old cards, because closing them shortens your credit history and shrinks your available credit. Both hurt. Keep older accounts open and lightly used.

Finally, talk to a lender early even if your score is not where you want it. A good loan officer runs a rapid rescore scenario and tells you the exact dollars-and-points payoff of getting from, say, 610 to 640. That number is usually motivating.

About the Author: Christopher Beal

Christopher Beal is a U.S. Army veteran and the Owner of Veteran Real Estate San Antonio, a Beal Group practice brokered by eXp Realty, TREC License #723559. He works exclusively with military and veteran buyers and sellers across Bexar, Comal, Kendall, Medina, and Bandera counties, with a focus on VA loans, PCS moves, and homebuying near JBSA-Lackland, JBSA-Randolph, and Fort Sam Houston. Having used his own VA benefit and navigated his own military moves, Christopher translates the parts of the VA loan process that confuse most first-time buyers, including the credit-score myths that scare people off before they ever start. He can be reached at (210) 882-8583.

Explore More Resources

Frequently Asked Questions

What is the lowest credit score that can get a VA loan in San Antonio?

There is no VA-set minimum, so the lowest score that works depends on the lender. Some San Antonio VA specialists approve scores in the low 500s through manual underwriting when residual income and reserves are strong. Most mainstream lenders set their floor at 580 or 620.

Does the VA have a minimum credit score requirement?

No. The Department of Veterans Affairs does not publish or enforce a minimum credit score. The number you encounter comes from the lender's internal overlay, not the VA program.

What credit score gets the best VA loan rate?

Generally a middle score of 720 or higher earns the best available pricing. The 680 to 719 band is close behind. Below 620, expect a slightly higher rate, though VA pricing penalizes lower scores less harshly than conventional loans do.

Which credit score do VA lenders use if I have three different ones?

Lenders pull all three bureaus and use the middle of the three scores, not the average or the highest. If you apply with a co-borrower, they typically use the lower of the two middle scores.

Can I use a VA loan with collections or a past bankruptcy?

Often yes. The VA looks at recent payment behavior and the reason behind derogatory marks. A bankruptcy that has been discharged for the required seasoning period, or old collections paired with a clean recent year, can still lead to approval, especially through manual underwriting.

How much can I raise my score before buying near JBSA?

Many buyers gain 20 to 40 points in 60 to 90 days by paying card balances below 30 percent of their limits, disputing errors, and keeping all payments current. That is often enough to move into a better rate band before locking.

Does my spouse's credit score affect our VA loan?

If your spouse is a co-borrower, yes. The lender uses the lower of the two middle scores, and your spouse's debts factor into the debt-to-income calculation. If your spouse is not on the loan, their score does not apply, though community-property rules in Texas can affect debts.

Will checking my own credit hurt my score before I buy?

No. Checking your own credit is a soft inquiry and does not affect your score. Only hard inquiries from new credit applications can ding it, which is why you should avoid opening new accounts in the months before you buy.

Does a higher credit score lower my VA funding fee?

No. The VA funding fee is based on your down payment and whether you have used your benefit before, not your credit score. Veterans with a service-connected disability rating are typically exempt from the funding fee entirely.

Thinking about a VA purchase in San Antonio? Whether your score is 760 or 580, the first move is the same: get a clear read on your numbers before you fall in love with a house. Call Christopher Beal at (210) 882-8583.

Ready when you are. Let us turn your VA benefit into a San Antonio home.

Serving those who served, from JBSA to the Hill Country.

Categories

- All Blogs (313)

- Alamo Heights (4)

- awards (3)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (71)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (24)

- Market Trends (5)

- Market Update (13)

- Military Relocation (93)

- Military Retirement (3)

- Mortgage (14)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (25)

- Real Estate (31)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (64)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (23)

- VA Home Loans (22)

- VA Loans (32)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts