Local vs National VA Lender in San Antonio (2026): Which One Actually Gets a Military Buyer to Closing?

LAST UPDATED: JULY 6, 2026 | BY CHRISTOPHER BEAL, U.S. ARMY VETERAN & REALTOR

Local vs National VA Lender in San Antonio (2026): Which One Actually Gets a Military Buyer to Closing?

Key Takeaways

- Both local San Antonio lenders and national VA lenders can close a VA loan - the real differences are appraisal speed, communication during underwriting, and how a listing agent perceives your offer.

- San Antonio homes averaged about 75 days on market in spring and early summer 2026 (SABOR MLS), so a lender who slips your closing by two weeks can cost you a rate lock, temporary housing money, or the house itself.

- Local lenders tend to win on VA appraiser familiarity, Tidewater response speed, and agent relationships; national VA lenders tend to win on advertised rates, technology, and 24/7 processing scale.

- The VA funding fee (2.15% for most first-use buyers) and the 4% cap on seller concessions are identical everywhere - so compare lenders on rate, lender fees, and execution, never on VA rules they all share.

- The 10-minute vetting checklist below works on any lender: VA volume, in-house underwriting, appraisal turn time in Bexar County, rate-lock terms, and a Loan Estimate in writing.

In This Guide

- Why does your VA lender choice matter more than the rate quote?

- What counts as a local VA lender in San Antonio?

- What do national VA lenders do well?

- How do local and national VA lenders compare head-to-head?

- Who closes faster in San Antonio, and why does the VA appraisal decide it?

- Which actually costs less: local or national?

- How do you vet any VA lender in 10 minutes?

- Which should you choose for your JBSA timeline?

Why Does Your VA Lender Choice Matter More Than the Rate Quote?

Every VA lender in America is delivering the same government-backed product. The entitlement rules, the appraisal requirements, the 4% cap on seller concessions, and the funding fee schedule come from the Department of Veterans Affairs, not from the bank. What varies - enormously - is how fast and how cleanly each company moves your file from contract to closing table.

That execution gap matters more in San Antonio than in most markets. Roughly one in five Bexar County purchase loans is VA-financed, the highest share of any major metro, because Joint Base San Antonio pushes tens of thousands of PCS moves through Lackland, Randolph, and Fort Sam Houston every year. Listing agents here have seen VA deals die from slow appraisals and missed conditions, and many of them quietly rank offers by which lender is attached.

I have closed more than 306 homes in and around San Antonio, the large majority with VA financing, and I have watched the same pattern for years: the buyer who chose a lender for a 0.125% advertised rate edge sometimes loses that edge - and more - in extended locks, repair renegotiations, and temporary housing when the closing slips past their report date.

What Counts as a Local VA Lender in San Antonio?

Local does not mean small, and it does not mean a better rate by default. It means the person structuring your loan knows which appraisers cover Converse versus Boerne, how Alamo Ranch new-builds handle VA MPR items, and which title companies in Stone Oak can close in a week when a PCS date moves. That pattern recognition is the product you are buying.

A strong local VA loan officer typically offers three things a call center cannot. First, direct cell-phone access on evenings and weekends - which matters when you are writing an offer on a Sunday from Germany at 9 p.m. Texas time. Second, personal relationships with San Antonio listing agents, who will call your lender to verify your file before accepting your offer over a competing one. Third, market-specific appraisal knowledge, including when and how to respond to a Tidewater notice with local comparable sales.

The trade-off is capacity and, sometimes, price. A two-person local team juggling forty files in a peak PCS month can bottleneck, and some local banks price VA loans slightly above the most aggressive national advertisers. Planning a PCS to JBSA? Christopher Beal specializes in military relocation - learn more here.

What Do National VA Lenders Do Well?

The best national VA lenders are genuinely good at VA loans - this is not a hit piece. Veterans United closed more VA purchase loans than any other lender in recent years, and USAA and Navy Federal have served military families for generations. Their underwriters see VA edge cases daily: entitlement restoration after a short sale, disability income grossing, COE corrections for Guard and Reserve time.

Their structural advantages are real. A 24/7 processing floor means your file does not stall because one loan officer took leave. Their app uploads beat email for OCONUS buyers signing documents from Ramstein or Okinawa. And their advertised rates are often the sharpest in the market, because volume lets them price thin.

The weaknesses are the mirror image of the strengths. You will rarely speak to the same person twice during underwriting. The appraisal is ordered through the VA portal either way, but a national processor who has never heard of Grey Forest cannot coach an appraiser conversation the way a local one can. And some San Antonio listing agents - fairly or not - discount offers backed by out-of-state call centers because they have watched those closings run long. Explore VA loan options here or request a free home evaluation if you also have a home to sell.

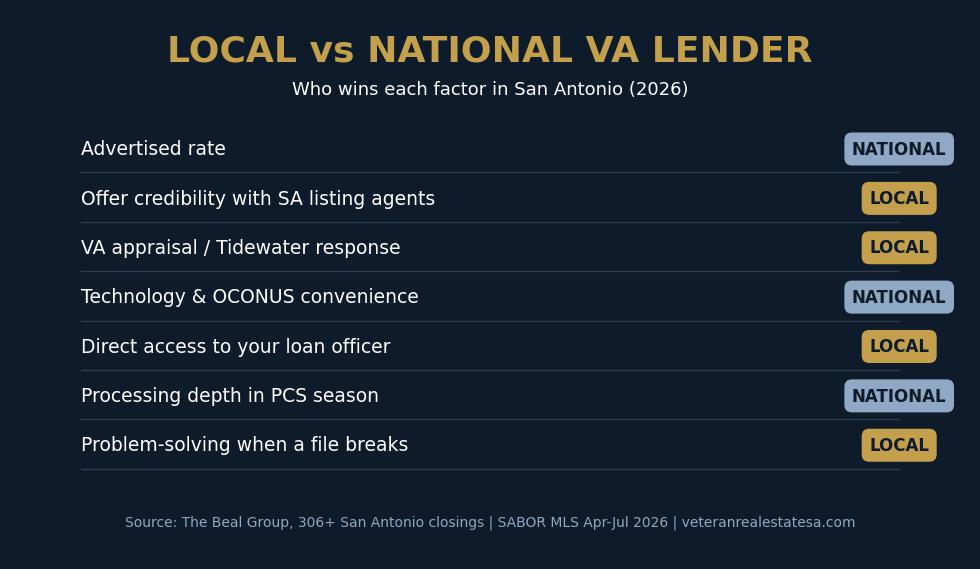

How Do Local and National VA Lenders Compare Head-to-Head?

Here is the comparison I walk military buyers through at the first consult. Score each row for your situation - a buyer purchasing sight-unseen from overseas weighs the technology row differently than a retiree buying in Schertz with time to spare.

| Factor | Local San Antonio VA Lender | National VA Lender |

|---|---|---|

| Advertised rate | Competitive, occasionally 0.125-0.25% above the sharpest ads | Often the lowest headline rates in the market |

| Offer credibility with SA listing agents | High - agents recognize the loan officer by name | Mixed - depends on the brand's local track record |

| VA appraisal / Tidewater handling | Strong - knows Bexar County appraiser pool, responds with local comps fast | Standardized - portal-driven, slower comp response |

| Communication | One loan officer, direct cell, weekends | Team model, portal messages, business hours |

| Technology / OCONUS convenience | Varies by shop | Excellent - app-based uploads and e-sign from any time zone |

| Processing depth in peak PCS season | Can bottleneck in June-August | Deep bench, files keep moving |

| Problem-solving when a file breaks | Loan officer walks it to the underwriter | Escalation queue, ticket-based |

Source: The Beal Group closing experience across 306+ San Antonio transactions, 2015-2026; SABOR MLS market data, April-July 2026. Individual lenders vary - vet the person, not just the brand.

Who Closes Faster in San Antonio, and Why Does the VA Appraisal Decide It?

A typical San Antonio VA purchase closes in 25 to 35 days when the file is managed well. The credit and income underwriting is rarely the delay; the appraisal is. Bexar County VA appraisal turn times run roughly 7 to 12 business days in normal months and stretch during summer PCS season, when thousands of families hit Lackland, Randolph, and Fort Sam Houston orders at once.

When a VA appraiser believes the value may come in below contract price, they issue a Tidewater notice, giving the lender's point of contact 48 hours to submit supporting comparable sales. This is the moment lender choice becomes visible. A local loan officer calls me, we pull SABOR comps for the subdivision the same afternoon, and the appraiser has a data package within hours. A national processing queue may burn most of the 48-hour window just routing the notice to someone authorized to respond.

Appraisal outcomes are also about preparation before the contract. An experienced military realtor prices the offer with VA appraisal behavior in mind, documents upgrades for the appraiser, and structures repair requests around VA Minimum Property Requirements instead of fighting them after the fact. That is agent work, not lender work - which is why the team you assemble matters as much as either piece alone.

Which Actually Costs Less: Local or National?

Three numbers are identical no matter which lender you pick, so refuse to let anyone sell you on them. The VA funding fee - 2.15% of the loan amount for most first-use buyers, and reduced or waived entirely for veterans with service-connected disability ratings - is set by the VA. The seller concession cap of 4% is set by the VA. And the rule that VA loans require no down payment at all is the same at every shop in America.

What actually moves your cost: the note rate, discount points, origination and underwriting fees, the rate-lock length (a 45-day lock costs more than a 30-day lock - and a lender who needs 45 days is telling you something), and lender credits. Get a written Loan Estimate from each finalist within the same 24-hour window, because rates move daily, and line up page 2 fee by fee. The Consumer Financial Protection Bureau's Loan Estimate explainer shows exactly where to look.

Also remember that lender cost is only one side of the ledger. Through our Serve & Save program, my team credits military and veteran clients 1% of the purchase price per year of service, up to 6%, which reduces closing costs directly - and that credit stacks with any lender you choose. See how Serve & Save works here.

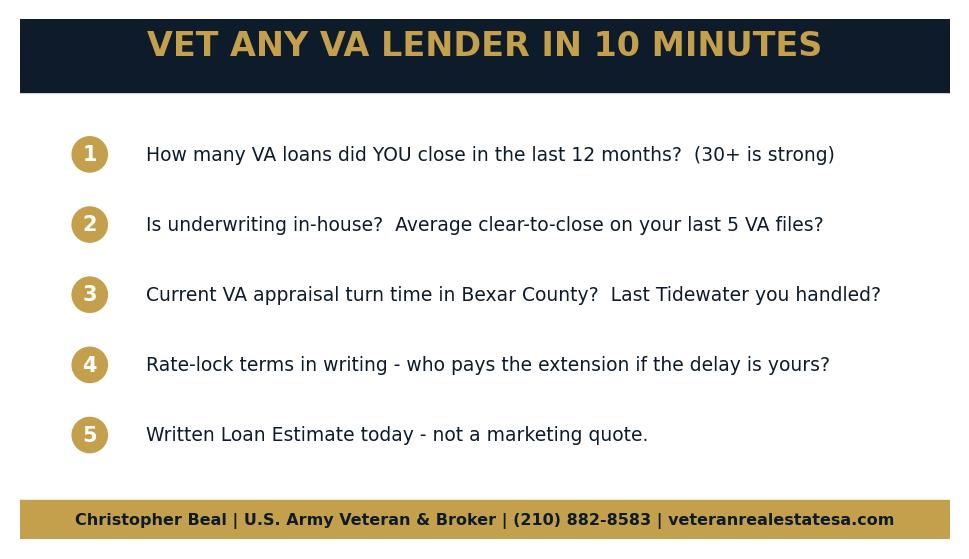

How Do You Vet Any VA Lender in 10 Minutes?

Run this checklist on every finalist, local or national, before you commit:

- Personal VA volume. "How many VA purchase loans did you personally close in the last 12 months?" You want a loan officer who lives in VA files - 30+ is a strong answer in this market. A great national LO beats a weak local one every time.

- In-house underwriting. Brokered-out underwriting adds days and removes control. Ask where the underwriter sits and the average clear-to-close time on the last five VA files.

- Bexar County appraisal turn time. If they cannot quote a current number for San Antonio, they are not closing enough loans here to know. Follow up: "Walk me through the last Tidewater you handled."

- Rate-lock protection. What does the lock cost, how long is it, and who pays the extension if the delay is on their side? Get it in writing.

- Same-day Loan Estimate. A lender who hesitates to put numbers on the official form is quoting you a marketing rate, not your rate. The VA's own home loan program pages and Military OneSource both recommend comparing multiple written offers.

Which Should You Choose for Your JBSA Timeline?

Different military buyers genuinely have different right answers. Here is the matchup table I use in consults:

| Your Situation | Best Pick | Runner-Up | Why |

|---|---|---|---|

| PCS with a report date under 60 days | Local VA lender | High-volume national with strong SA record | Appraisal management and agent credibility compress the timeline |

| Buying sight-unseen from OCONUS | National VA specialist | Local lender with strong e-close stack | App-based document flow and time-zone coverage matter most |

| Competing offers in Stone Oak, Alamo Ranch, or Schertz | Local VA lender | Whichever lender your agent can vouch for | Listing agents weigh the lender when offers are close |

| Complex file: entitlement restoration, Guard/Reserve COE, disability income | The strongest VA specialist available | - | Expertise beats geography on hard files |

| Rate-shopping a refinance, no deadline | National advertiser | Local credit union (RBFCU, Security Service) | With no execution risk, price wins |

Source: The Beal Group military buyer consults, 2024-2026.

The honest bottom line: I close on time with both kinds of lenders, and the variable that predicts a smooth closing is the individual loan officer's VA fluency, not the logo. Interview two or three, run the checklist, and let the written Loan Estimates - not the ads - make the call. Start with a bulletproof VA pre-approval here, and if a seller-funded rate buydown is on the table, know that VA seller concessions rules let sellers pay up to 4% toward your costs. Buyers with zero savings should read the VA down payment guide, and rate-sensitive buyers should also screen for assumable VA loans.

About the Author: Christopher Beal

Christopher Beal is a U.S. Army veteran, broker-owner of Veteran Real Estate San Antonio: The Beal Group at eXp Realty, and a Military Relocation Professional (MRP) with the National Association of REALTORS. Since 2015 he has closed more than 306 homes and over $117 million in volume across Bexar, Comal, Kendall, Medina, and Bandera counties, most of them for military and veteran families using VA financing. He is a three-time San Antonio Business Journal Top 25 agent, six-time eXp ICON award winner, 2026 RateMyAgent Agent of the Year for San Antonio, and holds a 5.0 rating across 60 Google reviews. Chris built the Serve & Save program, which reduces closing costs for military clients by 1% of the purchase price per year of service, up to 6%. He works PCS timelines for JBSA families year-round - from Lackland trainee moves to Randolph instructor tours - and he answers his own phone: (210) 882-8583. TREC #723559.

Explore More Resources

- VA Home Loans in San Antonio

- Military Relocation and PCS Services

- Free Home Evaluation

- Serve & Save Program

- Client Reviews

- About Christopher Beal

Ready to build your VA lending short list?

Call or text Christopher Beal at (210) 882-8583 for lender introductions that match your timeline.

Email [email protected] with your report date and target neighborhoods for a same-week game plan.

Visit veteranrealestatesa.com to search VA-friendly listings across greater San Antonio.

FAQ: Choosing a VA Lender in San Antonio

Do local lenders offer better VA rates than national lenders?

Not automatically. National high-volume VA shops often advertise the sharpest headline rates, while local lenders are usually within 0.125-0.25% and sometimes beat them outright. The only fair comparison is written Loan Estimates from both, pulled within the same 24-hour window.

Can a listing agent reject my offer because of my lender?

They cannot reject you for using a VA loan in a discriminatory way, but sellers can and do weigh financing strength when comparing offers. A pre-approval from a lender with a strong San Antonio closing record genuinely improves how your offer is received in competitive neighborhoods.

How long does a VA loan take to close in San Antonio in 2026?

A well-managed VA purchase closes in 25 to 35 days. The VA appraisal is the usual pacing item, running about 7 to 12 business days in Bexar County and longer during peak summer PCS season.

What is the Tidewater process and why does it matter?

Tidewater is the VA's early-warning procedure when an appraiser expects value to come in below the contract price. The lender's point of contact gets 48 hours to submit supporting comparable sales. Lenders and agents who respond fast with strong local comps save deals that slower files lose.

Is the VA funding fee different at different lenders?

No. The funding fee is set by the VA - 2.15% for most first-use buyers - and it is identical at every lender. Veterans receiving service-connected disability compensation are typically exempt. Compare lenders on rate, points, and fees instead.

Do I need a down payment for a VA loan in San Antonio?

No. VA loans allow qualified buyers to finance 100% of the purchase price with no down payment and no monthly mortgage insurance. Many of my JBSA buyers close with little more than earnest money and inspection costs out of pocket, especially when seller concessions cover closing costs.

Can I use USAA or Navy Federal from overseas for a San Antonio home?

Yes, and their technology makes OCONUS document flow easy. If you are buying sight-unseen on a tight report date, pair that lender with a San Antonio agent who can manage the appraisal and inspection process on the ground for you.

Should I get pre-approved before or after choosing a realtor?

Do them in the same week. Your agent will know which lenders perform locally and can flag a weak pre-approval before it costs you a house. I introduce most clients to two or three lenders and let the written numbers compete.

What credit score do I need for a VA loan?

The VA sets no minimum score; lender overlays typically start around 580 to 620. If your score is borderline, a VA-fluent loan officer can often structure the file - residual income is the VA's real yardstick - where a generic lender just declines it.

Does the Serve & Save program work with any lender?

Yes. Serve & Save is a Beal Group program that reduces closing costs by crediting 1% of the purchase price per year of service, up to 6%, at closing. It stacks with any local or national VA lender you choose.

Categories

- All Blogs (307)

- Alamo Heights (4)

- awards (2)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (68)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (23)

- Market Trends (3)

- Market Update (13)

- Military Relocation (93)

- Military Retirement (3)

- Mortgage (12)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (15)

- PCS (25)

- Real Estate (31)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (4)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (63)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (21)

- VA Home Loans (20)

- VA Loans (32)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts