Assumable VA Loans in San Antonio (2026): How to Find and Buy a Home With a Low-Rate Mortgage

LAST UPDATED: JUNE 22, 2026 | BY CHRISTOPHER BEAL, U.S. ARMY VETERAN & REALTOR

Assumable VA Loans in San Antonio (2026): How to Find and Buy a Home With a Low-Rate Mortgage

Key Takeaways

- An assumable VA loan lets a buyer take over a seller's existing mortgage at its original interest rate, which is powerful when that rate is 2.25% to 3.25% and new VA loans run near 6.9% in 2026.

- You do not have to be a veteran or active-duty to assume a VA loan, but you must qualify with the loan servicer and the loan must clear VA and servicer approval.

- The catch is the equity gap: you must pay or finance the difference between the low loan balance and the home's purchase price, often with cash or a second lien.

- A veteran buyer who substitutes their own entitlement protects the seller's VA benefit; a non-veteran buyer ties up the seller's entitlement until the loan is paid off.

- The assumption funding fee is 0.5% of the loan balance, far less than the 2.15% to 3.3% charged on a new VA purchase loan.

In This Guide

- What is an assumable VA loan, and why does it matter in 2026?

- How much can you save by assuming a VA loan in San Antonio?

- Who can assume a VA loan?

- How do you find assumable VA loan listings in San Antonio?

- What is the step-by-step assumption process?

- How do you cover the equity gap?

- What are the risks and catches to know?

- Assumption vs. a new VA loan: which is better right now?

What Is an Assumable VA Loan, and Why Does It Matter in 2026?

Every VA loan is assumable, and that single feature has become one of the most valuable buyer tools in the San Antonio market. When a seller financed their home in 2020 or 2021 at a 2.5% to 3.25% rate, that low rate is attached to the loan, not the person. A qualified buyer can step into it. With new 30-year VA loans hovering near 6.9% in June 2026, inheriting a sub-3% mortgage is the difference between a comfortable payment and a stretched one.

This is not a loophole. The U.S. Department of Veterans Affairs has always allowed VA loans to be assumed. Loans closed after March 1, 1988 simply require lender and VA approval first, which is a screening step, not a barrier. The reason almost no one talked about assumptions for a decade is that rates were low, so assuming a loan offered no advantage. The high-rate environment of 2025 and 2026 flipped that math entirely.

For San Antonio, a city where roughly one in three buyers has a military connection through Joint Base San Antonio, this matters more than almost anywhere in the country. A large share of local homes carry VA loans, which means a large share of listings carry assumable, low-rate mortgages waiting for the right buyer to claim them.

How Much Can You Save by Assuming a VA Loan in San Antonio?

The savings are not theoretical; they are arithmetic. A $400,000 balance at 2.75% over 30 years costs about $1,633 a month in principal and interest. The same balance financed fresh at 6.90% costs about $2,634. That is a $1,001 monthly gap before taxes and insurance.

That payment gap also expands your buying power. A buyer approved for a $2,600 monthly payment can afford a meaningfully more expensive home when the underlying rate is 2.75% rather than 6.9%. In neighborhoods like Stone Oak, Alamo Ranch, and Cibolo, where median prices sit well above the Bexar County median of $325,000, that leverage can move a family from a starter home into the school district they actually want.

Who Can Assume a VA Loan? (You Do Not Have to Be a Veteran)

This surprises most buyers: you do not need a Certificate of Eligibility or any military service to assume a VA loan. A schoolteacher, a nurse, or a small-business owner with no military background can take over a veteran's VA mortgage. The servicer evaluates the new borrower the same way a lender evaluates any applicant, looking at credit score, debt-to-income ratio, and stable income.

Where veteran status matters is entitlement. When a veteran buyer assumes the loan and substitutes their own VA entitlement, the seller's entitlement is fully restored, freeing the seller to use their VA benefit again on the next home. When a civilian assumes the loan, the seller's entitlement stays locked to that property until the loan is paid off or refinanced out of the VA program. We explain that trade-off in depth in our seller's playbook for assumable VA loans during a PCS, which is the companion piece to this buyer's guide.

How Do You Find Assumable VA Loan Listings in San Antonio?

There is no public filter for low-rate assumable loans, which is exactly why they stay hidden in plain sight. The San Antonio Board of Realtors MLS does not require sellers to advertise that their loan is assumable, and many sellers do not even realize they are sitting on a marketable asset. Finding these homes takes targeted work rather than a simple search.

The practical approach we use for buyers has three parts. First, we identify homes most likely to carry a VA loan, such as properties purchased between 2020 and 2022 near JBSA Lackland, Randolph, and Fort Sam Houston. Second, we contact listing agents directly to ask whether the seller's loan is assumable and what rate and balance it carries. Third, once a candidate is found, we verify everything in writing with the loan servicer before an offer is written. A buyer working alone almost never gets past the first step, because the information is not published anywhere.

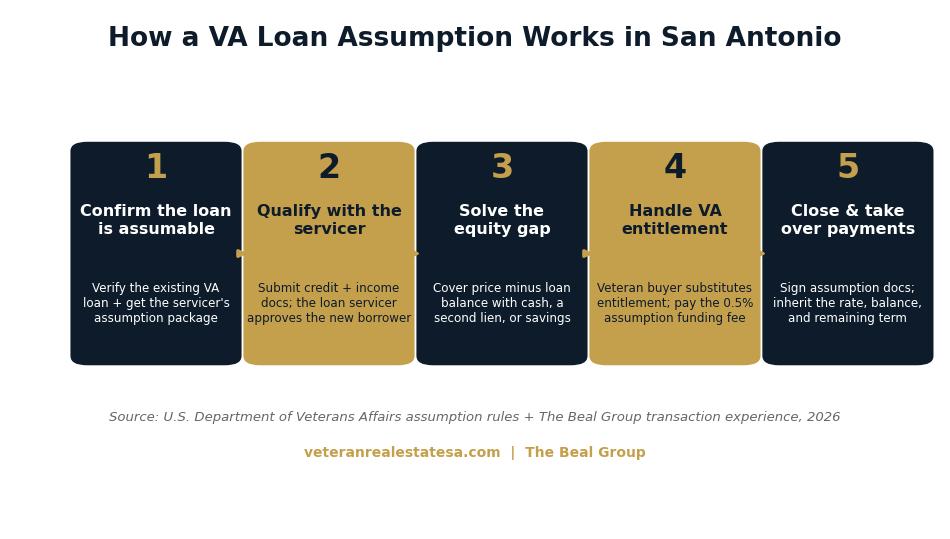

What Is the Step-by-Step Process to Assume a VA Loan?

An assumption is its own kind of transaction, and the loan servicer, not the buyer or seller, sets the pace. Here is the sequence:

- Confirm the loan is assumable. Get the seller's loan details and request the servicer's assumption package. Almost every VA loan qualifies, but the servicer must process it.

- Qualify with the servicer. Submit credit and income documentation. The servicer underwrites you as the new borrower and the VA reviews the file.

- Solve the equity gap. Plan how you will cover the difference between the purchase price and the lower loan balance (covered in detail below).

- Handle VA entitlement and the funding fee. A veteran buyer substitutes entitlement; everyone pays the 0.5% assumption funding fee unless exempt.

- Close and take over payments. Sign the assumption documents and inherit the original rate, balance, and remaining term.

The biggest difference from a normal purchase is timing. Servicer assumption departments can be slow, and a 45-to-90 day window is common. A San Antonio buyer should build that reality into their offer and their lease or temporary housing plan, which matters especially for families on PCS orders to JBSA working against a report date.

How Do You Cover the Equity Gap Between the Loan Balance and the Price?

This is where most assumptions succeed or fall apart. Suppose a Stone Oak home is priced at $537,000 and the seller's assumable VA loan balance is $360,000. The buyer must bring the $177,000 difference to the table, because assuming the loan does not reduce the price the seller is owed. The low rate applies only to the existing balance.

Buyers solve the gap in a few ways. Many use cash from savings or the sale of a previous home. Some use a second lien, where a separate lender finances the gap at today's rate while the large first loan keeps its low rate, blending to a payment still well below a single new mortgage. The blended approach can work beautifully, but it requires careful math, which is exactly the kind of analysis we run before you commit. Buyers should treat the equity-gap plan as the first thing to solve, not the last, because a home with a small loan balance and a high price may not pencil out no matter how attractive the rate looks.

What Are the Risks and Catches Veterans Should Know?

An assumption is a great tool, but it is not free of trade-offs. The entitlement issue is the one veterans miss most often. If you are a veteran selling to a civilian who assumes your loan, your entitlement remains attached to that property. You cannot get the full benefit back for your next purchase until the loan is paid off. That is a reason many veteran sellers prefer a veteran buyer who can substitute entitlement, and it is a point of leverage a buyer can use.

The other real risks are practical. The equity gap can be too large to finance comfortably. Servicer timelines can stretch and test a closing date. And the assumed loan keeps its original escrow and terms, so a buyer should review the existing taxes and insurance carefully. None of these are reasons to avoid assumptions; they are reasons to go in with a clear plan and a broker who has closed them. This article is general education, not legal, tax, or financial advice, and your situation should be reviewed with your lender and a tax professional before you act.

Assumption vs. a New VA Loan: Which Is Better Right Now?

| Factor | Assuming a VA Loan | New VA Loan (2026) |

|---|---|---|

| Interest rate | Seller's original rate (often 2.25% to 3.25%) | Current market, near 6.9% |

| Funding fee | 0.5% of loan balance | 2.15% to 3.3% (first vs. subsequent use) |

| Cash needed up front | High (must cover the equity gap) | Low (0% down available) |

| Who qualifies | Any creditworthy buyer, servicer approval | Veterans and eligible service members only |

| Typical timeline | 45 to 90 days (servicer driven) | 30 to 45 days |

| Best for | Cash-strong buyers chasing a low payment | Buyers needing maximum financing |

Source: U.S. Department of Veterans Affairs loan and funding fee guidance, 2026; market rates as of June 2026. Individual terms vary by lender and borrower.

About the Author: Christopher Beal

Christopher Beal is the owner and broker of Veteran Real Estate San Antonio: The Beal Group at eXp Realty, and a U.S. Army veteran. He holds the Military Relocation Professional (MRP) designation, is a member of the Veterans Association of Real Estate Professionals (VAREP), and has been recognized among the San Antonio Business Journal Top 25 and as a six-time ICON agent. Christopher and his team have closed more than 293 homes and over $112 million in volume, with a focus on military and veteran buyers and sellers, PCS moves, and VA loans across Bexar, Comal, Kendall, Medina, and Bandera counties. He works with buyers every week to evaluate whether assuming a low-rate VA loan is the right move, and his Serve and Save program reduces closing costs for the military families he serves.

Explore More Resources

- VA Home Loans in San Antonio

- Military Relocation and PCS Support

- Free Home Evaluation

- The Serve and Save Program

- VA Loan Pre-Approval: Step by Step

- About Christopher Beal

For the official rules behind VA loan assumptions, see the U.S. Department of Veterans Affairs home loan program and the Consumer Financial Protection Bureau, which both publish plain-language guidance on assuming a mortgage.

Frequently Asked Questions

Are all VA loans assumable?

Yes. Every VA loan is assumable. Loans closed after March 1, 1988 require lender and VA approval before the assumption can be completed, but the feature itself is built into every VA mortgage.

Do I have to be a veteran to assume a VA loan?

No. Any creditworthy buyer can assume a VA loan if the loan servicer approves their credit and income. Veteran status only matters for how VA entitlement is handled at closing.

What is the funding fee to assume a VA loan?

The VA assumption funding fee is 0.5% of the loan balance, which is much lower than the 2.15% to 3.3% charged on a new VA purchase loan. Some borrowers, such as veterans with a service-connected disability rating, are exempt.

How do I pay the difference between the loan balance and the price?

You cover the equity gap with cash, savings, gift funds, or a second mortgage layered on top of the assumed first loan. The low rate applies only to the existing balance, so the gap must be financed or paid separately.

How long does a VA loan assumption take in San Antonio?

Most assumptions take 45 to 90 days because the loan servicer controls the timeline. Build that window into your offer and any temporary housing or lease plans, especially on a PCS timeline.

Will assuming a loan hurt the veteran seller?

It can. If a non-veteran assumes the loan, the seller's VA entitlement stays tied to that property until the loan is paid off. A veteran buyer who substitutes their own entitlement restores the seller's benefit in full.

Is an assumed VA loan cheaper than a new VA loan in 2026?

On monthly cost and total interest, yes, when the assumed rate is far below the current market rate and you can cover the equity gap. A new VA loan is better when you need maximum financing with little cash up front.

Can I get an assumable VA loan listing through a regular MLS search?

Not reliably. Assumable status is rarely labeled in the MLS, so finding these homes takes targeted screening by an agent who then confirms the rate and balance with the listing agent and servicer.

Thinking about buying a home with an assumable VA loan in San Antonio? Let's find the hidden low-rate listings together.

Call or text Christopher Beal at (210) 882-8583.

Email [email protected].

Visit veteranrealestatesa.com.

Watch: How Assumable VA Loans Work in San Antonio

Here is a short video on how buying a home with an assumable VA loan can let you inherit the seller's low mortgage rate, and what it takes to qualify in San Antonio.

Categories

- All Blogs (297)

- Alamo Heights (3)

- awards (2)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (64)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (5)

- Luxury (25)

- Luxury Real Estate (22)

- Market Trends (2)

- Market Update (12)

- Military Relocation (92)

- Military Retirement (3)

- Mortgage (10)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (15)

- PCS (25)

- Real Estate (30)

- reviews (1)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (1)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (61)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (19)

- VA Home Loans (18)

- VA Loans (30)

- Va Loans & Financing (26)

- Veterans (5)

- Veterans Resources (38)

Recent Posts