VA Loan and Divorce in San Antonio (2026): Removing a Co-Borrower, Entitlement Restoration, and Who Keeps the House

Last Updated: June 29, 2026 | By Christopher Beal, U.S. Army Veteran & Realtor

VA Loan and Divorce in San Antonio (2026): Removing a Co-Borrower, Entitlement Restoration, and Who Keeps the House

Key Takeaways

- A divorce decree does not remove anyone from a VA mortgage. Only a refinance, a sale, or a lender-approved release of liability takes a name off the loan.

- The veteran's VA entitlement stays tied up in the home until the loan is paid off or refinanced, even if a civilian ex-spouse keeps the house, which can block the veteran from buying again with a VA loan.

- A VA Interest Rate Reduction Refinance Loan (IRRRL) can remove a co-borrower only if the veteran stays on the loan; the civilian spouse keeping the house usually needs a conventional refinance instead.

- Texas is a community property state, so a home bought during the marriage is generally marital property regardless of whose name is on the loan, which makes the buyout math the real negotiation.

- Selling is often the cleanest path: it pays off the loan, fully restores the veteran's entitlement, and splits the equity, and the Serve & Save program reduces closing costs for the next move.

In This Guide

- What happens to a VA loan in a Texas divorce?

- Can you remove an ex-spouse from a VA loan?

- How does VA entitlement restoration work after divorce?

- Who keeps the house: refinance, sell, or buy out?

- Can a civilian ex-spouse keep the VA-financed home?

- What does it cost to refinance or sell during a divorce?

- How do you time a divorce home sale with the San Antonio market?

- Frequently asked questions

What Happens to a VA Loan in a Texas Divorce?

The single most common mistake I see at the kitchen table is assuming the judge can split the loan. A San Antonio divorce decree can order who gets the house and who pays the mortgage, but it has no power over the lender or the U.S. Department of Veterans Affairs. If both names are on the note, both people remain on the hook for the payment in the eyes of the bank, no matter what the decree says.

This matters more for a VA loan than almost any other mortgage, because a VA loan is built on the veteran's entitlement, which is a finite benefit guaranteed by the federal government. When a Joint Base San Antonio family bought their home in Converse, Schertz, or Cibolo using that entitlement, the benefit was pledged against the property. Until the loan is gone, that entitlement is not fully available for the veteran to buy the next home.

Texas adds its own wrinkle. As a community property state, Texas generally treats a home bought during the marriage as belonging to both spouses, even if only the servicemember signed the note and only the servicemember had VA eligibility. That means the equity is usually split, and the spouse who did not qualify for the VA loan can still have a community property claim on the house. Sorting the loan, the deed, and the entitlement into three separate buckets is the first real step.

For a deeper look at who can legally be attached to a VA loan in the first place, our guide to VA loan co-borrowers in Texas walks through the eligibility rules that a divorce later has to unwind.

Can You Remove an Ex-Spouse From a VA Loan?

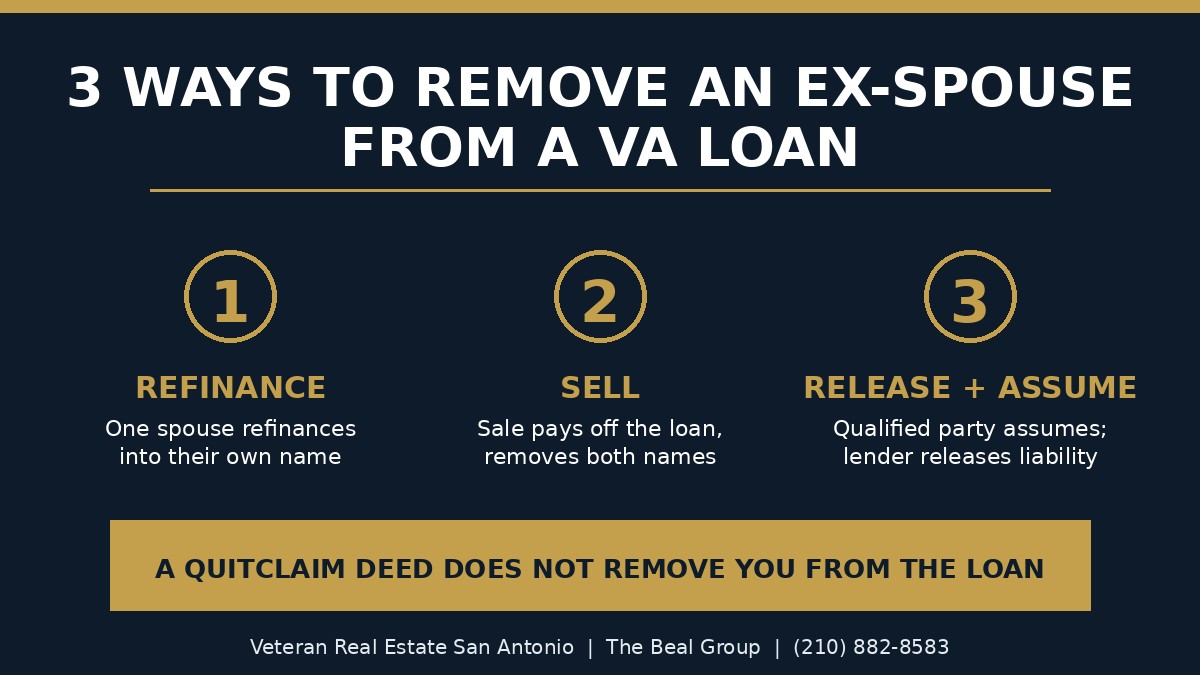

A quitclaim deed transfers ownership, not debt. Many San Antonio couples sign a quitclaim so the leaving spouse gives up the house, then assume the job is done. It is not. The person who quitclaimed away the property is often still a borrower on the mortgage, still liable for missed payments, and still has that debt on their credit report when they try to rent or buy. The deed and the loan are separate instruments.

There are three clean ways to actually take a name off a VA mortgage:

- Refinance into one spouse's name. If the veteran keeps the home, a VA Interest Rate Reduction Refinance Loan (IRRRL) or a VA cash-out refinance can remove the civilian spouse. If the civilian spouse keeps the home, they generally cannot use the VA program and refinance into a conventional loan instead.

- Sell the home. A sale pays off the entire loan at closing, removes both names at once, and frees the equity to divide. This is the most complete reset.

- Release of liability with loan assumption. The VA allows a qualified person to assume the loan and the VA may release the departing party from liability. The catch for the veteran is entitlement, covered in the next section.

Planning a move after the split? Christopher Beal specializes in military relocation across San Antonio and can map the sale-and-rebuy timeline against your PCS or report-date deadlines.

How Does VA Entitlement Restoration Work After Divorce?

This is the part that surprises the veteran most. You earned the VA home loan benefit through service, but it is not unlimited. Each VA loan uses a slice of your entitlement, and that slice stays committed to the property until the loan is satisfied. In a divorce, if the home and its VA loan land with your former spouse, your benefit can remain locked to a house you no longer own.

According to the U.S. Department of Veterans Affairs, entitlement is restored when the loan is paid in full and the property is no longer owned by the veteran, or in limited cases through a one-time restoration. Practically, that gives most divorcing San Antonio veterans two reliable paths to get their full benefit back:

- Sell the home. The loan is paid at closing, the property leaves the veteran's name, and full entitlement is restored, ready for the next VA purchase near JBSA Lackland, Randolph, or Fort Sam Houston.

- Refinance out of the VA loan. If the ex-spouse keeps the home and refinances into a conventional loan, that pays off the VA loan and restores the veteran's entitlement.

If you are weighing whether keeping the home is even worth it, our guide on assumable VA loans in San Antonio explains how assumptions and entitlement substitution actually work, and a surviving spouse facing a related question can start with VA loan surviving spouse benefits.

Who Keeps the House: Refinance, Sell, or Buy Out?

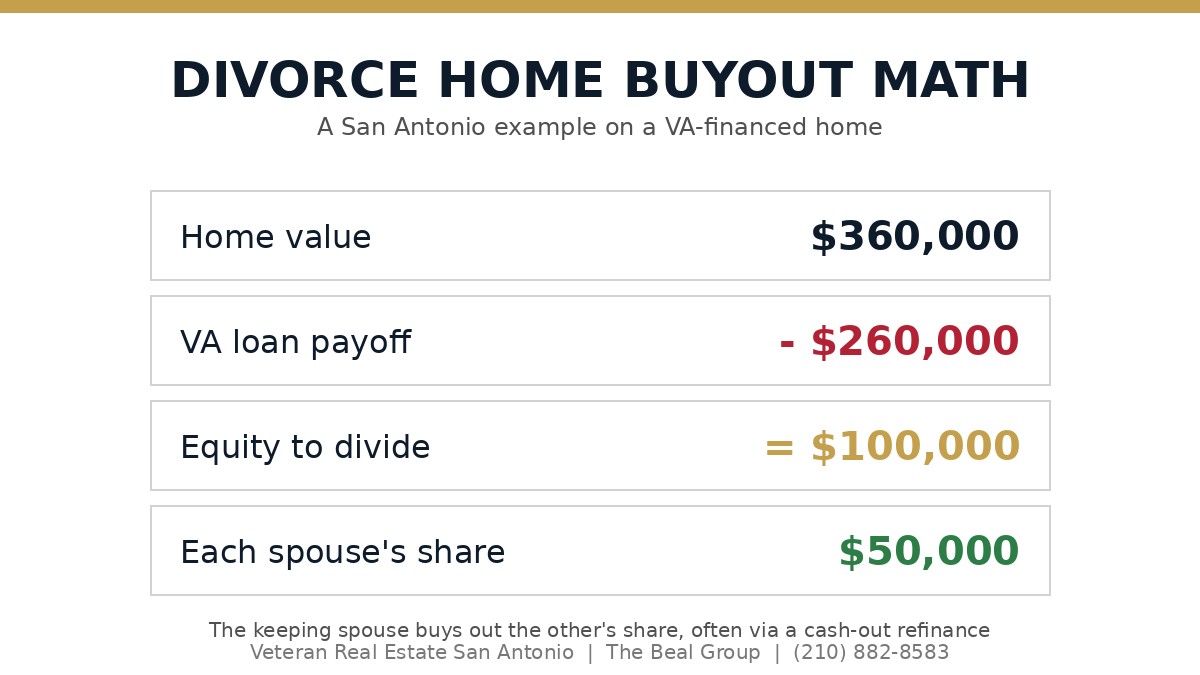

Start with the buyout math, because that is what the negotiation really turns on. In a Texas community property divorce, the spouse keeping the house typically buys out the other's share of the equity. If the home is worth $360,000 and the payoff is $260,000, the $100,000 of equity is generally split, so the keeping spouse owes the leaving spouse roughly $50,000, often funded by a cash-out refinance or other marital assets.

Three honest questions decide the path:

- Can one person qualify alone? A single income has to cover the new payment, taxes, and insurance. Many San Antonio homes that were comfortable on two incomes are not on one.

- Does the veteran want to buy again soon? If yes, keeping a VA loan on the old house may block the next purchase, which tilts toward selling.

- Is there enough equity to make a buyout fair? Thin equity plus refinance costs sometimes means selling nets both people more.

Can a Civilian Ex-Spouse Keep the VA-Financed Home?

The civilian spouse keeping the home is the scenario that most needs a plan. A non-veteran cannot get a brand-new VA loan in their own name. So if the civilian spouse wants the house, the realistic options are a conventional refinance into their name, or a VA loan assumption where they take over the existing VA loan with the lender's and the VA's approval.

An assumption can be attractive when the existing VA rate is far below today's market, but it has two requirements that trip families up. First, the assuming party must qualify with the servicer. Second, the veteran's entitlement question must be resolved: ideally another eligible veteran substitutes their entitlement, or the veteran accepts that their benefit stays tied to the home. The Military OneSource financial counseling line is a free resource for service members working through these tradeoffs, and Texas-specific procedural help is available through TexasLawHelp.org.

What Does It Cost to Refinance or Sell During a San Antonio Divorce?

The numbers below are typical San Antonio ranges for 2026, not a quote. Your lender's Loan Estimate and a Realtor's net sheet give the real figures.

| Factor | Refinance buyout (keep home) | Sell the home |

|---|---|---|

| Up-front cost | 2 to 5 percent of loan in closing costs, plus cash for the equity buyout | Agent commissions and seller closing costs, paid from sale proceeds |

| VA funding fee | IRRRL fee is 0.5 percent; a VA cash-out is 2.15 percent (first use, with under 5 percent down). Exempt for veterans with a service-connected disability rating. | None on the sale; applies only to the next VA purchase |

| Veteran entitlement | Stays tied to the home unless the veteran is the one refinancing out | Fully restored at closing |

| Qualifying | One person must qualify on one income | No new qualifying required to sell |

| Best when | Strong single income, low existing rate, one party deeply wants the home | Thin equity, neither party qualifies alone, or the veteran wants to buy again |

Source: VA funding fee schedule, va.gov, 2026; typical San Antonio closing cost ranges. Figures are illustrative and not a loan offer.

Comparing a refinance against a fresh VA purchase later? The VA funding fee explained guide breaks down first-use versus subsequent-use fees, and the Serve & Save program page shows the closing-cost credit in detail.

How Do You Time a Divorce Home Sale With the San Antonio Market?

Divorce sales fail on timing more than on price. When two people need the proceeds split by a court date, or when the veteran has a PCS clock running, the schedule drives everything. A listing-agent net sheet and a realistic days-on-market estimate let the attorneys write a decree that the calendar can actually meet.

If the home appraises below the agreed value during a buyer's financing, the deal can stall, which is why understanding what happens if your San Antonio home appraises low matters in a divorce sale as much as a normal one. And if the veteran is keeping the house as a rental rather than selling, the VA loan occupancy rules decide whether that is even allowed.

When you are ready, you can call Christopher Beal at (210) 882-8583 for a confidential, no-pressure walk-through of your options.

About the Author: Christopher Beal

Christopher Beal is the Owner of Veteran Real Estate San Antonio: The Beal Group at eXp Realty and a U.S. Army veteran who has guided more than 306 families to closing across over $117 million in San Antonio real estate. He holds TREC License #723559 and the Military Relocation Professional (MRP) certification, is a member of the Veterans Association of Real Estate Professionals (VAREP), and has been recognized as a San Antonio Business Journal Top 25 producer and a six-time eXp ICON agent. He works specifically with military and veteran buyers and sellers across Bexar, Comal, Kendall, Medina, and Bandera counties, including families navigating PCS moves, VA loans, and the hard transitions that come with a divorce. His Serve & Save program reduces closing costs for those who served. This article is general information for San Antonio veterans and is not legal or financial advice.

Explore More Resources

Frequently Asked Questions

Does a Texas divorce decree remove my name from the VA loan?

No. A decree can order who is responsible for the mortgage, but the lender and the VA are not bound by it. Your name comes off the loan only through a refinance, a sale, or a lender-approved release of liability with an assumption.

Can my ex-spouse keep our San Antonio home if it has a VA loan?

Yes, but a civilian cannot originate a new VA loan, so they usually refinance into a conventional loan or formally assume the existing VA loan with lender and VA approval. Living in the home is not the same as being responsible for the loan.

Will I get my VA entitlement back after the divorce?

Your entitlement is restored when the VA loan is paid off, typically by selling the home or by the home being refinanced out of the VA program. If a civilian ex-spouse keeps the house with the VA loan attached, your entitlement can stay tied up.

Can I use a VA IRRRL to remove my spouse from the loan?

An IRRRL can remove a co-borrower only if the veteran remains on the loan. If the civilian spouse is the one keeping the home, an IRRRL is generally not available to them and a conventional refinance is the path.

Is the house community property if only I had VA eligibility?

In Texas, a home bought during the marriage is generally community property regardless of whose name was on the loan or who had VA eligibility, so the equity is usually divided. Confirm specifics with your Texas family law attorney.

Should I sell or refinance during the divorce?

Selling restores your entitlement, splits equity cleanly, and avoids one-income qualifying, which is often best when equity is thin or you plan to buy again. A refinance buyout makes sense when one person strongly wants the home, can qualify alone, and the existing rate is low.

How long does it take to sell a San Antonio home in a divorce?

A well-prepared Bexar County home in the 2026 market typically takes about 45 to 70 days from list to close. Build that runway into the decree timeline, especially if a PCS or report date is in play.

Does the VA funding fee apply when I refinance after divorce?

Yes. A VA IRRRL carries a 0.5 percent funding fee and a VA cash-out refinance is 2.15 percent for first use with under 5 percent down. Veterans with a service-connected disability rating are exempt.

Going through a separation and need a clear, confidential plan for the house? I help San Antonio military and veteran families decide whether to sell, refinance, or buy out, and I protect your VA entitlement in the process.

Call or text Christopher Beal at (210) 882-8583.

Email [email protected].

Visit veteranrealestatesa.com to start with a free, no-pressure home

Categories

- All Blogs (299)

- Alamo Heights (3)

- awards (2)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (66)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (5)

- Luxury (25)

- Luxury Real Estate (22)

- Market Trends (2)

- Market Update (12)

- Military Relocation (92)

- Military Retirement (3)

- Mortgage (11)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (15)

- PCS (25)

- Real Estate (30)

- reviews (1)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (1)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (61)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (19)

- VA Home Loans (20)

- VA Loans (31)

- Va Loans & Financing (26)

- Veterans (5)

- Veterans Resources (38)

Recent Posts