Do You Need a Down Payment for a VA Loan in San Antonio? (2026 Guide)

Last Updated: June 16, 2026 | By Christopher Beal, U.S. Army Veteran & Realtor

Do You Need a Down Payment for a VA Loan in San Antonio? (2026 Guide)

Key Takeaways

- For the large majority of San Antonio veterans with full entitlement, a VA loan requires $0 down, with no private mortgage insurance, regardless of the purchase price within reason.

- A down payment is only required in specific cases: buying above your available entitlement, using reduced (second-tier) entitlement after a prior VA loan, or adding a co-borrower who is not VA-eligible.

- Down payment is not the same as cash to close. Even with $0 down, you will need earnest money, closing costs, and prepaids, though the VA funding fee can usually be financed into the loan.

- The VA funding fee is 2.15% of the loan for most first-use buyers; veterans with a service-connected disability rating are typically exempt entirely.

- In San Antonio's 2026 market, seller concessions of up to 4% on a VA loan can cover much of your closing costs, and the Serve & Save program reduces closing costs further for veteran clients.

In This Guide

- Does a VA loan really require zero down?

- When does a VA loan actually require a down payment?

- Down payment vs cash to close: what is the difference?

- What is the VA funding fee, and do you pay it up front?

- How can San Antonio veterans reduce cash to close?

- Should you ever put money down on a VA loan?

- About the Author

- Frequently Asked Questions

Does a VA Loan Really Require Zero Down?

The single biggest myth I hear from San Antonio buyers is that they need to save 20% before they can buy. For a veteran with full VA entitlement, that is simply not true. The VA home loan guaranty lets eligible service members, veterans, and surviving spouses finance 100% of the purchase price. You can confirm the basics straight from the U.S. Department of Veterans Affairs home loan program.

Just as important, VA loans carry no monthly private mortgage insurance (PMI). A conventional buyer putting less than 20% down pays PMI every month until they build equity; a VA buyer never does. That structural difference is why a VA loan often beats a low-down-payment conventional loan even when the rate looks similar. We break that comparison down in our VA loan vs conventional loan guide.

If you are still learning how the program works from the ground up, start with our explainer on how a VA loan works for first-time military buyers, then come back here for the down-payment specifics.

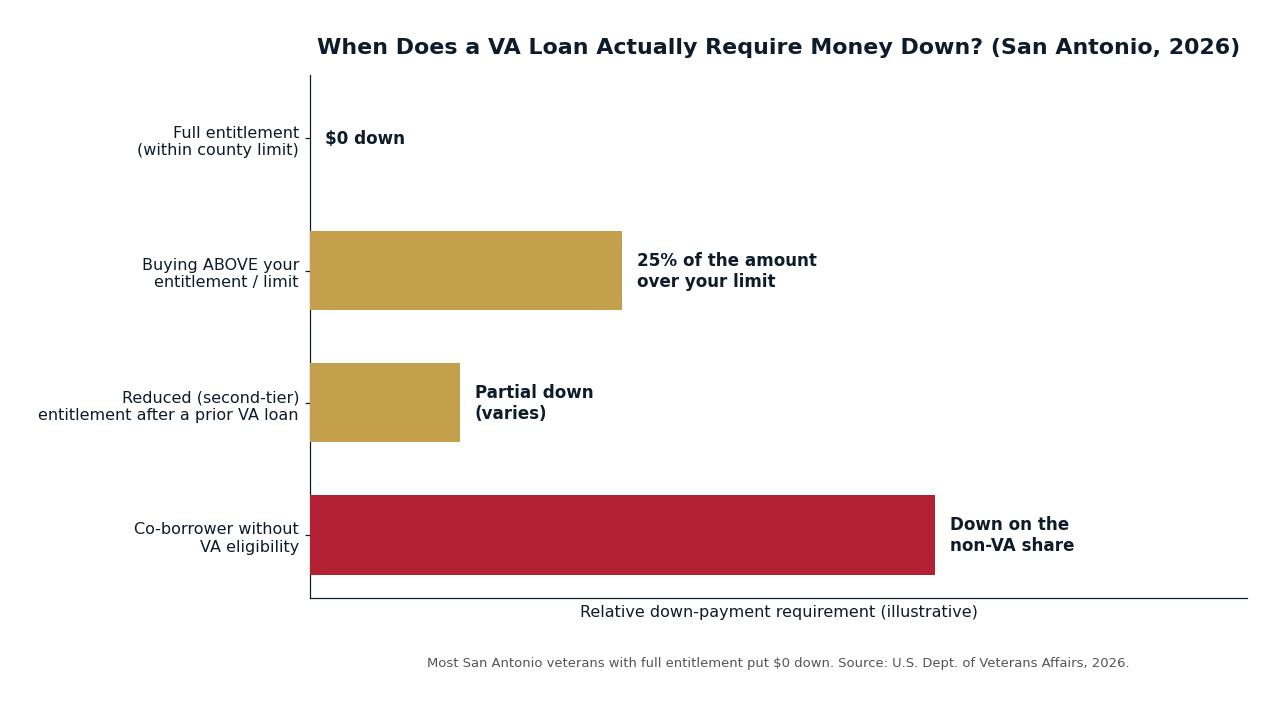

When Does a VA Loan Actually Require a Down Payment?

The exceptions are specific, predictable, and worth understanding before you shop. The chart below summarizes them, and each one comes up regularly with San Antonio buyers, especially those who have used their VA benefit before during an earlier assignment.

| Situation | Down Payment? | Why |

|---|---|---|

| Full entitlement, any reasonable price | $0 | No loan limit applies with full entitlement |

| Buying above your available entitlement | 25% of the amount over the limit | Lender wants 25% total coverage on the excess |

| Reduced (second-tier) entitlement after a prior VA loan | Often partial | Less entitlement remains to guaranty the new loan |

| Co-borrower who is not VA-eligible | Down on the non-VA share | VA guaranty covers only the veteran's portion |

Source: U.S. Department of Veterans Affairs entitlement and loan-limit rules, 2026. Figures are general; your lender calculates your exact requirement.

The case that surprises people most is the over-the-limit purchase. Veterans with full entitlement have no loan limit, but if you have used part of your entitlement on a home you still own elsewhere, your remaining entitlement is capped by the county loan limit. Buy above that, and you put down 25% of the amount over the limit. If you have used your benefit before, our guide on using a VA loan more than once and second-tier entitlement walks through the math.

For higher-priced San Antonio homes, even an over-the-limit VA loan can require far less down than a conventional jumbo. Our VA jumbo loan guide shows how veterans buy luxury homes with little to nothing down.

Down Payment vs Cash to Close: What Is the Difference?

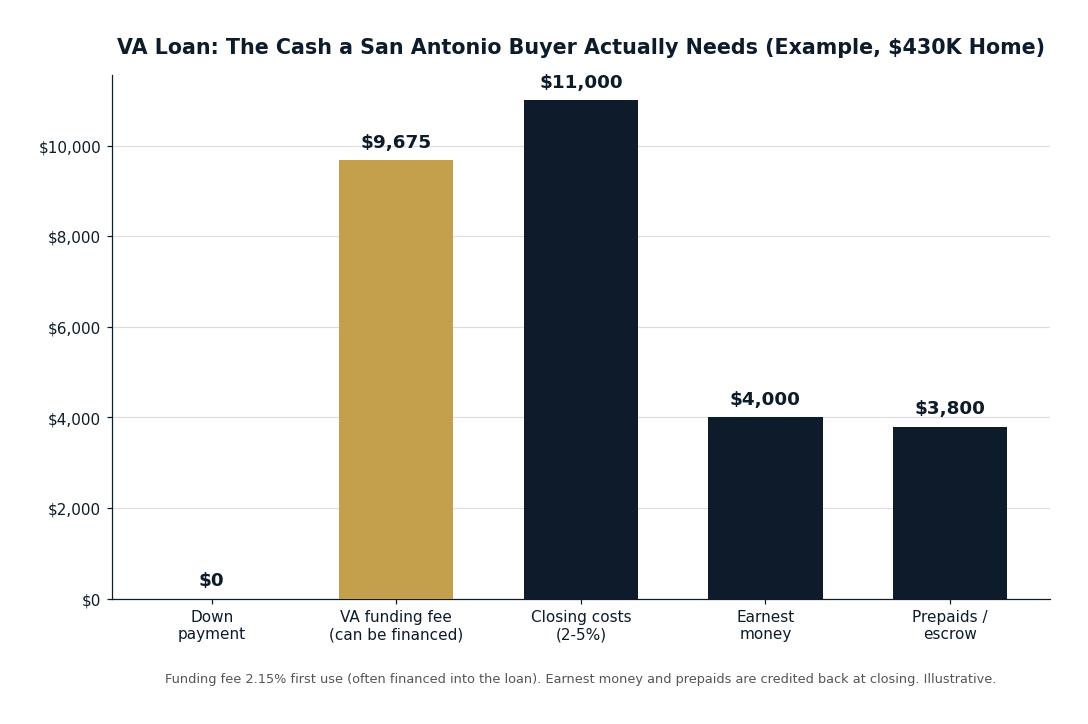

This is the distinction that trips up first-time veteran buyers, so let us be precise. Zero down does not mean zero dollars. You will still write checks along the way, and knowing what they are removes the surprise. The chart below shows the real cash picture on an example $430,000 San Antonio purchase.

Here is what each piece means. Earnest money is a good-faith deposit, often 1% of the price, that you put up when your offer is accepted; it is credited back to you at closing. Closing costs run roughly 2 to 5 percent and cover lender fees, title, and appraisal. Prepaids fund your first homeowners insurance and property tax escrows. None of these is a down payment, but together they are the cash you actually need on hand.

For a full line-item breakdown specific to our market, see our dedicated guide to VA loan closing costs in San Antonio.

What Is the VA Funding Fee, and Do You Pay It Up Front?

The funding fee is the program's way of keeping itself running without taxpayer cost, and it is more flexible than buyers expect. For a first-use purchase with zero down, the fee is 2.15% of the loan amount. The key point: you do not have to bring that in cash. Most veterans finance the funding fee into the loan, so it raises the balance slightly rather than the cash you bring to closing. The official schedule lives on the VA funding fee page.

If you receive VA disability compensation, or are a surviving spouse, you are generally exempt from the funding fee entirely, which removes a meaningful cost from the transaction. Putting some money down also lowers the fee tier, which we cover in the next section.

How Can San Antonio Veterans Reduce Cash to Close?

Even though the down payment is usually $0, smart negotiation can shrink the rest of the cash you need close to zero too. On a VA loan, a seller is allowed to pay up to 4% of the value in concessions, which can cover the funding fee, prepaids, and other costs. In a balanced San Antonio market where homes are closing near 97.1% of list, well-structured offers regularly include a concession request.

- Seller concessions. Up to 4% on a VA loan can be directed at your closing costs and prepaids.

- Closing-cost credits. Negotiated directly in the purchase contract, especially when a home has been on the market a while.

- Lender credits. Accepting a slightly higher rate in exchange for the lender covering some costs can make sense if you plan to refinance later.

- Serve & Save. The Beal Group's program reduces closing costs for veteran clients, returning 1% per year of service up to 6%.

Stacked together, these tools mean many veterans walk into a San Antonio home for little more than their earnest money and inspection costs. If you are relocating on orders, our PCS to Joint Base San Antonio timeline guide shows how to line up financing with your report date.

Curious what your concession strategy should look like? Learn how Serve & Save reduces your closing costs.

Should You Ever Put Money Down on a VA Loan?

Just because you can buy with nothing down does not mean it is always the best play. A modest down payment does three useful things: it shrinks your monthly payment, it can drop the funding fee to a lower tier (putting 5% or more down reduces the first-use fee), and in a competitive offer it can signal strength to a seller. For a higher-rate environment, a smaller balance also means less interest over the life of the loan.

On the other hand, your VA benefit exists precisely so you do not have to drain your savings to buy a home. Keeping a healthy reserve for moving costs, furnishings, and the inevitable first-year repairs is often wiser than maximizing your down payment. The right answer depends on your savings, your rate, and your plans for the home, which is exactly the kind of decision I help veterans think through.

About the Author: Christopher Beal

Christopher Beal is the owner and broker of Veteran Real Estate San Antonio: The Beal Group at eXp Realty, and a U.S. Army veteran who has built his career helping military families buy and sell across San Antonio and the surrounding counties of Bexar, Comal, Kendall, Medina, and Bandera. He holds the Military Relocation Professional (MRP) designation, belongs to the Veterans Association of Real Estate Professionals (VAREP), and carries Texas real estate license TREC #723559. A six-time ICON agent and San Antonio Business Journal Top 25 producer, Chris has closed more than 293 homes and over $112 million in transactions, many of them VA-financed purchases near Joint Base San Antonio. Through the Serve & Save program, Chris reduces closing costs for veteran clients, returning 1% per year of service up to 6%.

Explore More Resources

Frequently Asked Questions About VA Loan Down Payments

Do I need a down payment for a VA loan in San Antonio?

No, not if you have full VA entitlement. Eligible veterans can finance 100% of the purchase price with no down payment and no private mortgage insurance. Down payments are only required when you buy above your available entitlement, use reduced entitlement, or add a non-eligible co-borrower.

Is there a maximum price I can buy with zero down?

With full entitlement, there is no VA loan limit, so price is governed by what you qualify for, not by a cap. If you have used part of your entitlement elsewhere, county loan limits apply to the remaining entitlement and may require a down payment above that amount.

What is the difference between a down payment and closing costs?

A down payment reduces the loan amount and is often $0 on a VA loan. Closing costs are separate fees for the lender, title, and appraisal, typically 2 to 5 percent of the price, that you pay to complete the purchase regardless of your down payment.

How much is the VA funding fee in 2026?

For most first-use buyers with zero down, the funding fee is 2.15% of the loan amount. It can be financed into the loan rather than paid in cash. Veterans with a service-connected disability rating are generally exempt.

Can the seller pay my closing costs on a VA loan?

Yes. On a VA loan a seller can contribute up to 4% of the value in concessions, which can cover the funding fee, prepaids, and other costs. This is a common way San Antonio veterans reduce their cash to close.

Does putting money down lower my VA funding fee?

Yes. A down payment of 5% or more reduces the first-use funding fee tier, and 10% or more reduces it further. Whether that trade-off is worth using your cash depends on your savings and rate.

How much cash do I actually need to buy with a VA loan?

Even with $0 down, plan for earnest money (often about 1% of the price), closing costs, and prepaids. After seller concessions and credits, many veterans need little more than their earnest money and inspection costs.

What is the Serve and Save program?

Serve & Save is The Beal Group's program that reduces closing costs for veteran clients, returning 1% per year of service up to a maximum of 6%. It stacks with seller concessions to lower the cash you bring to closing.

Can I use my VA loan benefit more than once?

Yes. The VA benefit can be reused, and entitlement can be restored after a prior loan is paid off. If you still owe on a prior VA loan, second-tier entitlement rules and county limits may require a down payment on the new purchase.

For most San Antonio veterans, the answer to "do I need a down payment" is a reassuring no, and the rest of the cash to close can be negotiated down with the right strategy.

If you are planning a purchase near Joint Base San Antonio and want a clear, honest picture of what you will actually need at closing, I am glad to help. Reach Christopher Beal at (210) 882-8583, email [email protected], or visit veteranrealestatesa.com.

Serving those who served, here in San Antonio.

Categories

- All Blogs (290)

- Alamo Heights (3)

- awards (2)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (63)

- Community Events (4)

- Hill Country (14)

- JBSA (33)

- Local Guide (5)

- Luxury (23)

- Luxury Real Estate (21)

- Market Trends (1)

- Market Update (12)

- Military Relocation (92)

- Military Retirement (3)

- Mortgage (9)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (15)

- PCS (25)

- Real Estate (30)

- reviews (1)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (1)

- San Antonio Neighborhoods (38)

- San Antonio Real Estate (60)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (17)

- VA Home Loans (14)

- VA Loans (27)

- Va Loans & Financing (26)

- Veterans (3)

- Veterans Resources (38)

Recent Posts