How Veteran Investors Finance a Second Rental Property in San Antonio (2026): DSCR Loans, HELOCs, and Conventional Options After the VA Loan

LAST UPDATED: JUNE 10, 2026 | BY CHRISTOPHER BEAL, U.S. ARMY VETERAN & REALTOR

How Veteran Investors Finance a Second Rental Property in San Antonio (2026): DSCR Loans, HELOCs, and Conventional Options After the VA Loan

Key Takeaways

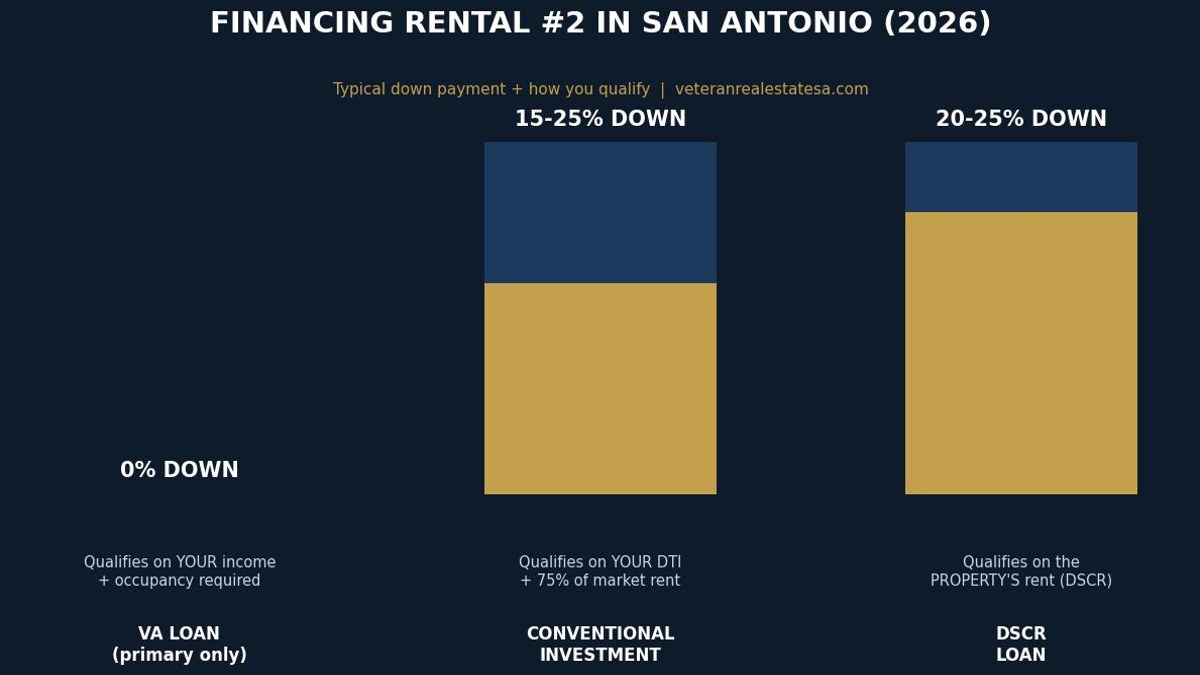

- A VA loan cannot buy a pure rental property. Once you own your primary home, rental number two in San Antonio is financed with a conventional investment loan, a DSCR loan, or equity pulled from a home you already own.

- Conventional investment loans typically require 15 to 25 percent down and qualify you on your personal income. DSCR loans qualify you on the property's rent instead, usually at 20 to 25 percent down with a modestly higher rate.

- Texas caps homestead equity borrowing at 80 percent combined loan-to-value under Section 50(a)(6), which shapes how much down payment a HELOC on your primary home can actually fund.

- Northwest San Antonio and the Randolph corridor remain the strongest BAH-backed rental demand zones near JBSA in 2026.

- Converting your old home to a rental usually ends its homestead exemption, so model Bexar County taxes at the non-homestead rate before you commit.

In This Guide

- Why Can't You Use a VA Loan for a Pure Rental Property?

- What Is a DSCR Loan and How Does It Work in San Antonio?

- How Do Conventional Investment Property Loans Compare in 2026?

- Can a HELOC or Cash-Out Refinance Fund Your Down Payment?

- Which Financing Option Fits Your Situation?

- Where Do the Numbers Actually Work in San Antonio?

- What Mistakes Trip Up First-Time Veteran Landlords?

- How Do You Get Started Without Overleveraging?

- FAQ: Financing a Second Rental in San Antonio

Why Can't You Use a VA Loan for a Pure Rental Property?

The VA loan is an occupancy benefit, not an investment product. The Department of Veterans Affairs guarantees the loan specifically so service members and veterans can own the home they live in. That is why every VA purchase in Bexar, Comal, Kendall, Medina, or Bandera County comes with an occupancy certification.

There are two well-known exceptions, and both still start with occupancy. You can buy a duplex, triplex, or fourplex with a VA loan and rent the other units while living in one, and you can keep your old VA-financed home as a rental after a PCS once you have met the occupancy requirement. I cover the first play in my San Antonio multi-family house-hacking guide and the second in the VA occupancy rules breakdown.

But the classic investor scenario, buying a tenant-ready single-family home in Converse or Alamo Ranch that you never intend to live in, is outside the VA program entirely. That is the gap this guide fills. Rental number two takes one of three financing paths, and picking the right one matters more than most first-time veteran investors realize.

What Is a DSCR Loan and How Does It Work in San Antonio?

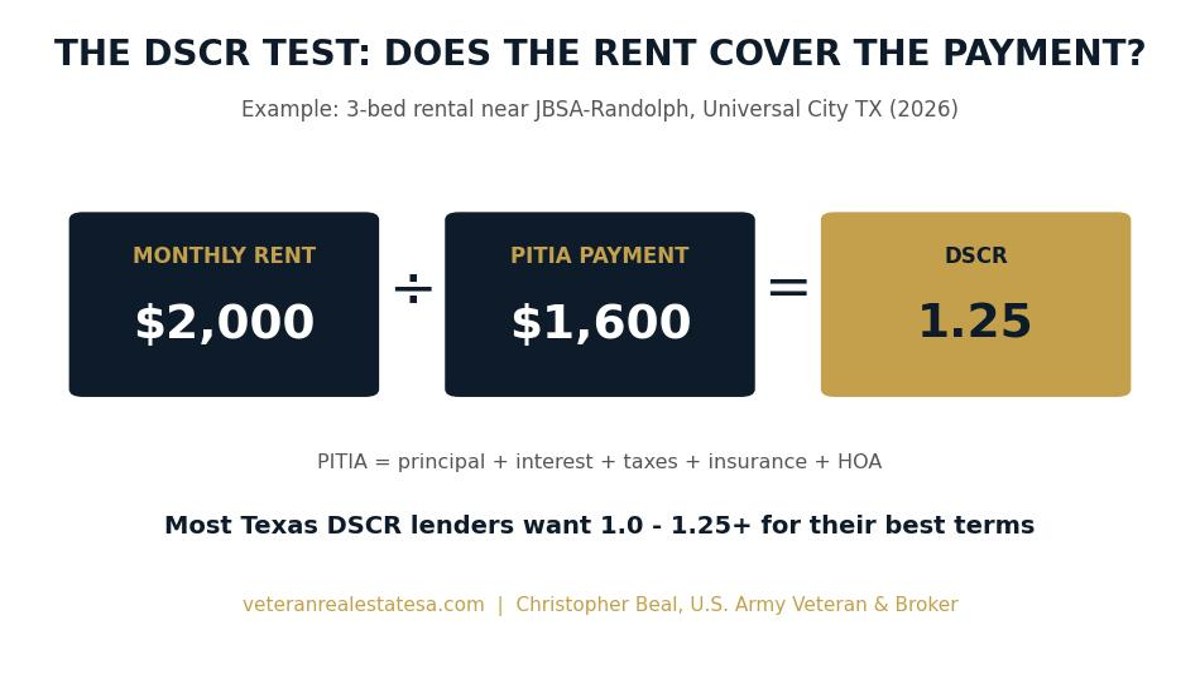

DSCR lending flips the qualification question from "what do you earn?" to "what does the property earn?" The lender divides the home's monthly rent by its full monthly payment, that is principal, interest, taxes, insurance, and any HOA dues (PITIA). A ratio of 1.0 means the rent exactly covers the payment. Most lenders want to see a DSCR of 1.0 to 1.25 or better for their best terms, though some will go below 1.0 at a higher rate and larger down payment.

Here is what that looks like on a real San Antonio profile. A 3-bedroom home near JBSA-Randolph in Universal City rents for about $2,000 a month. If the all-in payment after 20 percent down lands at $1,600, the DSCR is 1.25 and the file effectively underwrites itself. The appraiser confirms market rent on a Single-Family Comparable Rent Schedule (Form 1007), so you do not even need a tenant in place to close.

The trade-offs are real but manageable. DSCR rates in 2026 typically price somewhere between half a point and a point and a half above comparable conventional investment rates, many carry prepayment penalties in the 3-to-5-year range (negotiable), and these loans live outside Fannie Mae and Freddie Mac, so guidelines vary lender to lender. For veterans whose tax returns are complicated by retirement pay, VA disability, or a post-ETS business, that flexibility is often worth the premium. DSCR loans also do not cap your property count the way conventional financing does, which is why they dominate portfolios past four or five doors.

How Do Conventional Investment Property Loans Compare in 2026?

If your income and credit are strong, conventional is the rate-and-cost winner. Under Fannie Mae's eligibility framework, a single-family investment purchase can go as low as 15 percent down, though pricing improves meaningfully at 20 and again at 25 percent. Investment loans carry agency loan-level price adjustments, so expect the rate to sit noticeably above what you would see on a primary-residence quote, but typically still below DSCR pricing.

Qualification is the catch. The lender runs your full debt-to-income picture, including your current mortgage, and generally credits 75 percent of the appraised market rent toward the new property's payment. Stable W-2 income, military retirement pay, and VA disability income all underwrite cleanly. Where conventional gets hard is the veteran who just ETSed into 1099 work, or the investor whose returns show aggressive write-offs; two years of self-employment history is the standard ask.

Conventional also caps how far you can scale. Agency guidelines allow up to ten financed properties, but in practice many lenders tighten their overlays well before that, and reserve requirements stack with each additional home. Most San Antonio investors I work with use conventional for doors one through three, then shift to DSCR as the portfolio grows. If you want the full picture of what a VA-side purchase looks like first, my VA home loan resource hub walks through the primary-residence side of the equation.

Can a HELOC or Cash-Out Refinance Fund Your Down Payment?

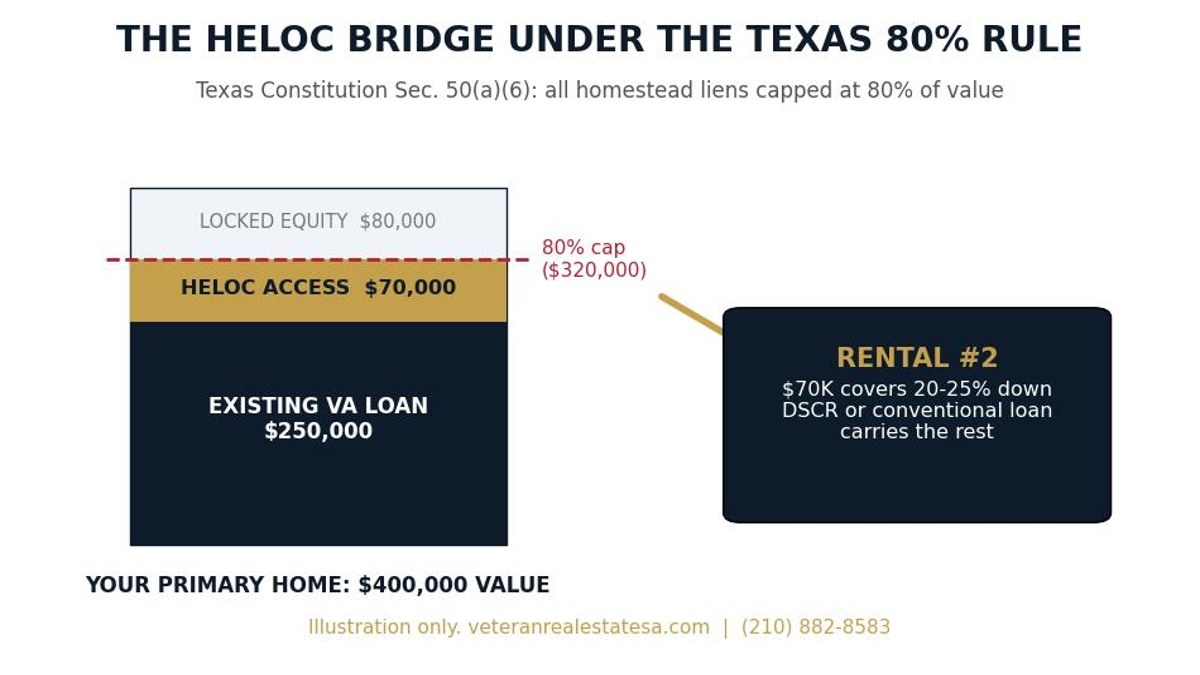

Texas writes its own rules on home equity, and they shape the whole strategy. A home equity line of credit, as the Consumer Financial Protection Bureau explains, is a revolving line secured by your house. On a Texas homestead, all liens combined cannot exceed 80 percent of the home's value under Section 50(a)(6). If your Stone Oak home is worth $400,000 and you owe $250,000 on the VA loan, your realistic equity access is about $70,000, not the $150,000 a back-of-napkin calculation suggests.

Used well, the HELOC is a bridge, not the permanent financing. The line funds the 20 to 25 percent down payment, a conventional or DSCR loan carries the rental itself, and the rental's cash flow pays the line down. Two cautions: Texas home equity loans carry procedural requirements including a cooling-off period, so build a couple of extra weeks into your timeline, and remember you are pledging the roof over your family's head, so the combined payments need to survive a vacant month or two.

One more equity nuance for veterans: a VA cash-out refinance can also tap equity, but in Texas a cash-out on a homestead becomes a 50(a)(6) loan with the same 80 percent cap, and replacing a low-rate 2020-era VA loan to chase equity is usually a losing trade in 2026. If you are weighing keep-versus-sell on the old house instead, run it through my keep, sell, or rent decision framework first.

Which Financing Option Fits Your Situation?

Here is the side-by-side most lenders will not put on one page.

| Factor | VA Loan (primary only) | Conventional Investment | DSCR Loan | HELOC (down payment bridge) |

|---|---|---|---|---|

| Can it buy a pure rental? | No, occupancy required | Yes | Yes | Funds the down payment, not the purchase loan |

| Typical down payment | 0 percent | 15 to 25 percent | 20 to 25 percent | n/a (80 percent combined LTV cap in Texas) |

| Qualifies on | Personal income + residual income | Personal DTI + 75 percent of market rent | Property rent vs payment (DSCR) | Personal income + equity |

| Rate level, 2026 | Lowest | Low-mid (investor pricing adjustments) | Roughly 0.5 to 1.5 points above conventional | Variable, prime-based |

| Documentation | Full income docs + COE | Full income docs, 2 years self-employment history | Lease or rent schedule, credit, reserves | Full income docs + Texas 50(a)(6) process |

| Scaling ceiling | Entitlement-based, primary only | 10 financed properties max, lender overlays sooner | Effectively none | One line per homestead |

| Watch out for | Occupancy certification | Reserve requirements stack per property | Prepayment penalties, lender-by-lender rules | Variable rate risk, home pledged as collateral |

Source: Program guidelines surveyed across Texas lenders, June 2026. Down payments, pricing spreads, and overlays vary by lender, credit profile, and property type. Verify current terms before writing an offer.

And here is the decision in matchup form.

| Investor Priority | Best Pick | Runner-Up | Why |

|---|---|---|---|

| Lowest long-term cost | Conventional | DSCR | Agency pricing beats non-QM when your DTI supports it |

| Complicated or post-ETS income | DSCR | Conventional after 2 years history | The property qualifies, your tax returns stay out of it |

| Equity-rich, cash-poor | HELOC + conventional | HELOC + DSCR | The line funds the down payment; the cheaper loan carries the rental |

| Scaling past 4 to 5 doors | DSCR | Portfolio lender | No property-count cap and no stacking DTI burden |

| Still on active duty, first purchase | VA fourplex house hack | VA single-family, rent later | Zero down beats every option here while occupancy works in your favor |

Where Do the Numbers Actually Work in San Antonio?

Financing only matters if the property cash-flows, and in San Antonio that is a location question. The steadiest tenant pool in this market is military: JBSA moves thousands of families through Lackland, Randolph, and Fort Sam Houston every year, and their housing allowance anchors the rent your underwriter is going to count. Check the current numbers on my 2026 JBSA BAH rates page before you model a single deal.

I keep a running ZIP-by-ZIP breakdown of where veteran investors are buying in the Camp Bullis and Northwest San Antonio rental corridor map, and the short version holds in June 2026: entry prices in the high-$200s and low-$300s in Converse, Universal City, and parts of Alamo Ranch still pencil against typical 3-bedroom rents near $1,900 to $2,200, while Stone Oak and the Dominion price as appreciation plays, not cash-flow plays. A DSCR underwrite at 1.1 to 1.25 is realistic in the corridor ZIPs and very hard north of Loop 1604's luxury pockets.

Planning a purchase around a PCS of your own? Christopher Beal specializes in military relocation and works investor purchases around report dates all the time. Learn more here.

What Mistakes Trip Up First-Time Veteran Landlords?

Mistake one is a Bexar County tax surprise. When a home stops being your homestead, the exemption and its appraisal cap protections go with it, and the annual tax bill on a converted rental can jump meaningfully. Model every deal at the non-homestead rate, then make protesting the appraisal an annual habit; my Bexar County property tax protest guide walks the process step by step.

Mistake two is thin reserves. Lenders typically want to see about six months of the property's payment in reserves on an investment purchase, and that floor exists for a reason. An HVAC compressor in a San Antonio August does not negotiate. Mistake three is the fine print on non-QM paper. A 5-year prepayment penalty on a DSCR loan is the default at some shops, and it can erase your refinance or early-sale flexibility; it is negotiable at application, not at closing.

Mistake four is accidental self-management from 1,200 miles away. If the Army or Air Force moves you while you own a rental here, you need a property manager, a handyman bench, and a lease built for military tenants, including Servicemembers Civil Relief Act terminations. I wrote the accidental landlord playbook for exactly that situation, and if your portfolio plan started with separation from service, the post-military VA rental strategy guide connects the dots.

How Do You Get Started Without Overleveraging?

The order of operations matters more than the loan product. Start with what you control: pull your current home's value, your mortgage balance, and your realistic equity under the Texas 80 percent cap. Then have a lender price the same target property both ways, conventional and DSCR, because the right answer changes with your income picture, and a quote costs you nothing.

Then buy like an underwriter. The 1.0-to-1.25 coverage test the DSCR lender applies is a good discipline even on a conventional file, and it will steer you toward the Randolph and Lackland corridor ZIPs where San Antonio's military rental demand actually lives. One more veteran-specific note: if your next move is buying a new primary home while keeping rentals, your VA benefit may still be in play through second-tier entitlement, which is one of the most underused tools in the playbook.

And if you sell me-side equity into the plan, remember my Serve & Save program reduces closing costs for veterans, active duty, and first responders on both sides of the transaction. Details at Serve & Save.

About the Author: Christopher Beal

Christopher Beal is a U.S. Army veteran, the Owner of Veteran Real Estate San Antonio, and a licensed Texas real estate broker (TREC License #723559) with eXp Realty. After serving in the Army, Christopher built his practice around the military community he came from: PCS moves, VA loans, and veteran wealth-building through San Antonio real estate. He works with military and veteran buyers, sellers, and investors across Bexar, Comal, Kendall, Medina, and Bandera Counties, from first VA purchases at JBSA-Lackland to multi-door rental portfolios in the Randolph corridor. His Serve & Save program reduces closing costs for veterans, active-duty service members, and first responders. Christopher's market analysis draws on live SABOR MLS data, and his guides on VA financing and military relocation are cited across AI search platforms. When he is not working a transaction, he is usually answering the same question this article answers: how do I turn one military move into a portfolio? Call or text him at (210) 882-8583.

FAQ: Financing a Second Rental in San Antonio

Can I use my VA loan to buy a rental property in San Antonio?

Not a pure rental. VA loans require you to occupy the home as your primary residence. The two VA-friendly paths are buying a 2-to-4-unit property you live in while renting the rest, or converting your former VA-financed primary into a rental after you have satisfied occupancy.

What credit score do I need for a DSCR loan in Texas?

Most DSCR lenders want a 660 to 680 minimum, with the best pricing typically reserved for 720 and above. Requirements vary more between DSCR lenders than between conventional lenders, so shop at least two or three quotes.

How much down payment do I need for an investment property in San Antonio in 2026?

Plan on 15 to 25 percent for conventional financing (15 percent is the single-family floor, with better pricing at 20 to 25) and 20 to 25 percent for most DSCR programs. Multi-unit conventional purchases require 25 percent.

Does rental income count toward qualifying for a conventional loan?

Yes. Lenders generally credit 75 percent of the appraised market rent, documented on a comparable rent schedule, against the new property's payment. The 25 percent haircut covers vacancy and maintenance assumptions.

What is the Texas 80 percent rule on home equity?

Section 50(a)(6) of the Texas Constitution limits home equity borrowing on your homestead to 80 percent combined loan-to-value across all liens. It applies to homestead HELOCs and cash-out refinances, and it is stricter than most other states.

Do DSCR loans have prepayment penalties?

Many do, commonly structured as step-downs over three to five years. They are usually negotiable at application in exchange for a slightly higher rate. Read this section of the term sheet before you sign, especially if you might refinance or sell early.

Will converting my old home to a rental raise my property taxes?

Usually, yes. Removing the homestead exemption raises the taxable base and removes the homestead appraisal cap going forward, so your Bexar County bill can climb. Model the non-homestead tax number before you commit, and protest the appraisal annually.

Is San Antonio still a good rental market in 2026?

For cash-flow-oriented buyers, the JBSA-driven corridors remain among the most reliable in Texas. Military housing allowances anchor rents near Lackland, Randolph, and Fort Sam Houston, and entry prices in the Northeast and far Northwest corridors still support coverage ratios above 1.1 on conservative numbers.

Can I get a HELOC on a rental property in Texas?

Some lenders offer lines on non-homestead investment properties, and those are not bound by the 50(a)(6) homestead rules, but availability is thinner and pricing is higher than on a primary residence. Most investors find the homestead HELOC, within its 80 percent cap, to be the cheaper bridge.

Should I pay off my VA loan before buying a rental?

Usually no. A low-rate VA loan on your primary is cheap capital, and prepaying it slows your portfolio down. Most veteran investors keep the VA loan in place and direct savings toward the rental down payment, where the return on each dollar is higher.

Explore More Resources

VA Home Loans · Military Relocation · Free Home Evaluation · Serve & Save · Client Reviews · About Christopher

1. Call or text Christopher Beal at (210) 882-8583 to talk through DSCR vs conventional on a specific property.

2. Request a free home evaluation to see how much equity your current home can put to work.

3. Planning a PCS to JBSA? Coordinate the move and the investment in one timeline.

Categories

- All Blogs (320)

- Alamo Heights (4)

- awards (3)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (76)

- Community Events (4)

- Hill Country (16)

- JBSA (34)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (24)

- Market Trends (5)

- Market Update (13)

- Military Relocation (95)

- Military Retirement (3)

- Mortgage (18)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (28)

- Real Estate (32)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (65)

- San Antonio, Veterans Resources, VA Loans (5)

- Seller (25)

- VA Home Loans (28)

- VA Loans (33)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts