VA Loan Co-Borrowers in Texas: Who Can (and Cannot) Be on the Loan With You in 2026

Last Updated: June 26, 2026 | By Christopher Beal, U.S. Army Veteran & Realtor

VA Loan Co-Borrowers in Texas: Who Can (and Cannot) Be on the Loan With You in 2026

Key Takeaways

- A legal spouse can co-borrow on a VA loan with full VA backing and zero down. This is the cleanest co-borrower scenario.

- Two eligible Veterans can combine their entitlement on a joint VA loan, which can increase buying power.

- A non-spouse, non-Veteran co-borrower (parent, fiance, sibling, friend) creates a joint VA loan where the VA backs only the Veteran's share, usually requiring about 12.5% down on the other person's portion.

- The VA does not allow traditional non-occupying co-signers; everyone on the loan must intend to live in the home, except the Veteran's spouse.

- Texas is a community property state, so a spouse's debts can affect your file even when the spouse is not on the loan.

In This Guide

- Who Can Be a Co-Borrower on a VA Loan?

- How Does a Spouse Co-Borrower Work?

- What Happens With a Non-Veteran Co-Borrower?

- Can Two Veterans Use Their Entitlement Together?

- Does the VA Allow a Non-Occupying Co-Signer?

- What Does Texas Community Property Mean for Your Loan?

- How Do You Decide Who Belongs on the Loan?

- Frequently Asked Questions

Who Can Be a Co-Borrower on a VA Loan?

The single most expensive mistake I see is adding the wrong person to the loan to "help" with income. It feels intuitive, a parent or partner with a strong salary should make approval easier, but on a VA loan the identity of your co-borrower changes the down payment, the entitlement, and sometimes the whole deal. Knowing the three lanes before you apply protects your zero-down benefit.

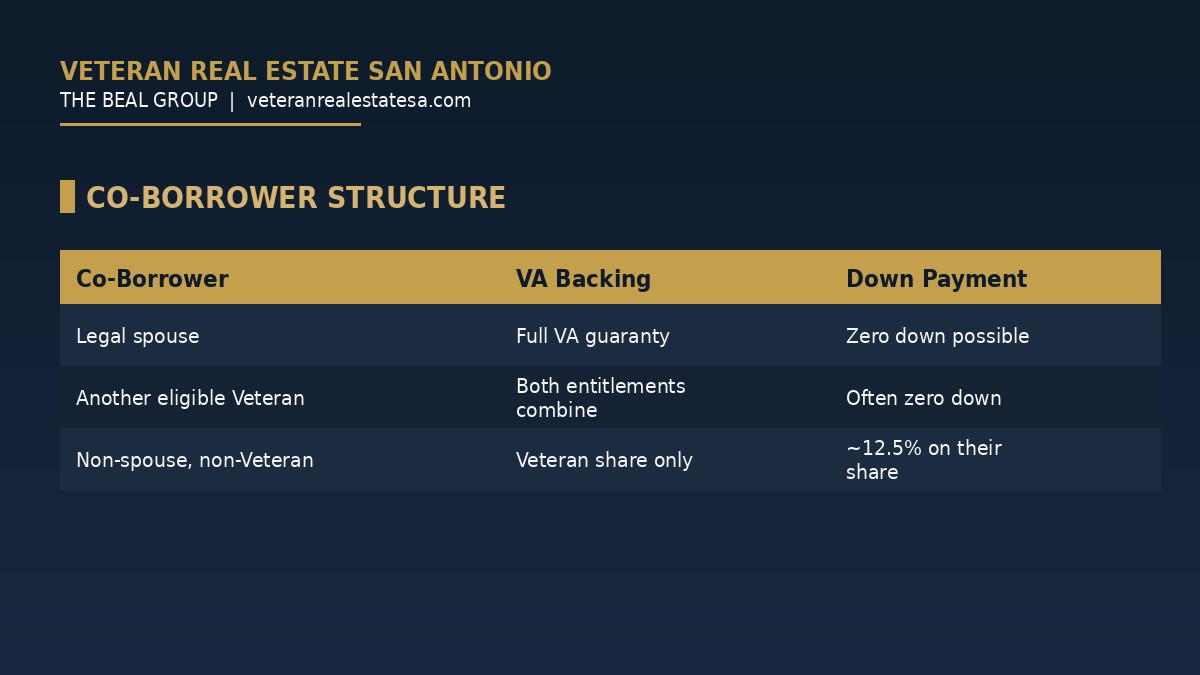

| Co-Borrower Type | VA Backing | Down Payment Impact |

|---|---|---|

| Legal spouse | Full VA guaranty | Zero down possible |

| Another eligible Veteran | Both entitlements combine | Often zero down |

| Non-spouse, non-Veteran | Veteran's share only | About 12.5% on their share |

Source: U.S. Department of Veterans Affairs lender handbook (M26-7) and standard lender guidance, 2026. Individual lenders may apply stricter overlays.

How Does a Spouse Co-Borrower Work?

The spouse co-borrower is the gold standard of VA co-borrowing. When a Veteran and their legal spouse buy together, the file is processed as a standard, fully guaranteed VA loan. You get zero-down eligibility, the spouse's income helps your debt-to-income ratio, and there is no joint-loan down payment penalty.

The trade-off is that the spouse's credit and debts come along too. A strong second income helps, but a spouse with significant debt or a low credit score can pull the file down. This is where an honest pre-approval matters, and our step-by-step pre-approval guide shows how to see the full picture before you write an offer.

What Happens With a Non-Veteran Co-Borrower?

This is the scenario that surprises buyers at the closing table. Say you and a partner you are not married to want to buy a $400,000 home together, split 50/50. The VA only guarantees your half. On your $200,000 share, the VA guaranty (25% of that share, or $50,000) keeps the lender comfortable. But the other person's $200,000 has no VA backing, so the lender typically asks for about 12.5% down on that share, around $25,000, to keep its exposure in check.

There is nothing wrong with a joint VA loan, and sometimes it is the right call. But you need to walk in knowing a down payment is coming, rather than assuming zero down and scrambling for cash later. It also uses your entitlement differently, which matters if you plan to use your VA loan again later.

Can Two Veterans Use Their Entitlement Together?

Two Veterans buying together is a powerful and underused option in a military town like San Antonio. Whether it is a married Veteran couple, two siblings who both served, or battle buddies investing together, combining entitlement can keep the loan zero-down and increase the amount you qualify for. Each Veteran's service record and COE has to support the file, so plan for a slightly longer document phase.

This structure is especially worth exploring for Veterans thinking about a multi-unit property or a long-term San Antonio plan. The benefit was designed to be flexible, and two Veterans pooling it well can buy more home than either could alone.

Does the VA Allow a Non-Occupying Co-Signer?

This is the rule that trips up families trying to help. On a conventional loan, a parent can co-sign from another state purely to strengthen the application without ever moving in. The VA loan does not work that way. Co-borrowers (other than your spouse) must occupy the property as their primary residence. A parent in Houston cannot co-sign your San Antonio purchase from afar simply to boost your approval.

If a relative genuinely wants to live with you and be on the loan, that is a joint VA loan with the down payment we discussed earlier. If they only want to help your credit, a VA loan is not the vehicle, and we should talk through other ways to strengthen your file. Understanding how the VA loan works overall makes these limits make sense.

What Does Texas Community Property Mean for Your Loan?

Even a "solo" VA loan in Texas is not always solo. Because Texas treats most debts acquired during marriage as community obligations, a lender on a VA loan may consider your spouse's monthly debts when calculating your debt-to-income ratio, even if you leave the spouse off the application entirely. It does not mean the spouse's income gets counted, only the debts, which can be a frustrating one-way street.

The practical takeaway: in San Antonio, you and your lender should review your spouse's debt picture early, married couples cannot fully wall it off the way they could in a non-community-property state. A local lender who handles Texas VA files daily will flag this before it becomes a problem at underwriting.

How Do You Decide Who Belongs on the Loan?

Every co-borrower decision comes down to three questions: Do you need the extra income to qualify? Is the co-borrower a spouse, a Veteran, or neither? And do you want to protect your zero-down benefit? Answer those honestly and the right structure usually becomes obvious.

My job as your broker is to run the scenarios before you fall in love with a house, so the financing fits the people, not the other way around. You can reach Christopher Beal directly at (210) 882-8583, and we will walk through your specific situation with no pressure and no jargon.

About the Author: Christopher Beal

Christopher Beal is the owner and broker of Veteran Real Estate San Antonio: The Beal Group at eXp Realty, and a U.S. Army Veteran. A Military Relocation Professional (MRP) and member of the Veterans Association of Real Estate Professionals (VAREP), Christopher has closed more than 300 homes and over $117 million in volume serving military and Veteran families across Bexar, Comal, Kendall, Medina, and Bandera counties. He is a three-time San Antonio Business Journal Top 25 producer, a six-time eXp ICON award winner, and holds Texas real estate license #723559. His practice is built specifically around active-duty, Guard, Reserve, and Veteran buyers and sellers, including the Serve and Save program, which reduces closing costs by 1% of the sale price per year of service, up to 6%. Reach Christopher at (210) 882-8583 or [email protected].

Explore More Resources

- VA Home Loans in San Antonio

- Military Relocation Services

- Free Home Evaluation

- The Serve and Save Program

- Client Reviews

- About Christopher Beal

Frequently Asked Questions

Can I add a co-borrower to my VA loan?

Yes. The VA recognizes three co-borrower scenarios: a Veteran and spouse (full backing, zero down possible), a Veteran and another eligible Veteran (combined entitlement), and a Veteran and a non-Veteran (a joint VA loan with a down payment on the non-Veteran's share).

Does adding a non-Veteran co-borrower require a down payment?

Usually yes. With a non-spouse, non-Veteran co-borrower, the VA guarantees only the Veteran's portion, so most lenders require a down payment of roughly 12.5% on the non-Veteran's share of the loan.

Can my spouse be on the VA loan even if they never served?

Yes. A legal spouse can co-borrow with full VA backing and no down payment, regardless of whether the spouse is a Veteran. The lender will count both incomes and both debts.

Will the VA let a parent co-sign from out of state?

No. The VA does not allow non-occupying co-signers. Any co-borrower other than your spouse must intend to occupy the home as a primary residence, so a parent cannot co-sign from another city purely to boost approval.

Can two Veterans buy a home together with VA loans?

Yes. Two eligible Veterans can combine entitlement on a joint VA loan, which can keep the purchase zero-down and increase combined buying power. Both Veterans need a valid Certificate of Eligibility.

Does my spouse's debt affect my VA loan in Texas?

It can. Texas is a community property state, so a lender may include your spouse's monthly debts in your debt-to-income calculation even if the spouse is not on the loan. The spouse's income is not counted in that case, only the debts.

Is a co-borrower the same as a co-signer on a VA loan?

Not exactly. On a VA loan, anyone on the note generally has to occupy the home (except your spouse), so the traditional credit-only co-signer that exists on conventional loans is not available.

How do I decide who should be on my VA loan?

Start with your goal. If protecting zero down matters, a spouse or a second Veteran is cleanest. If a non-Veteran must be on the loan, plan for the down payment. A Veteran broker and a VA-savvy lender can model each option for your specific numbers.

For official guidance, review the VA Home Loans program page and the VA's lender handbook, M26-7, which covers joint-loan guaranty rules. Always confirm your specifics with a VA-approved lender.

Buying with a partner, a parent, or a fellow Veteran in San Antonio? Call Christopher Beal, U.S. Army Veteran and Realtor, at (210) 882-8583. Veteran Real Estate San Antonio: The Beal Group will structure your purchase so the financing fits your family. Serving those who serve, and saving them money at the closing table.

Watch: Who Can Be a Co-Borrower on a VA Loan in Texas?

I put together a quick video that breaks down exactly who can be on a VA loan with you in San Antonio without losing your zero-down benefit. Here is the short version.

Categories

- All Blogs (299)

- Alamo Heights (3)

- awards (2)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (66)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (5)

- Luxury (25)

- Luxury Real Estate (22)

- Market Trends (2)

- Market Update (12)

- Military Relocation (92)

- Military Retirement (3)

- Mortgage (11)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (15)

- PCS (25)

- Real Estate (30)

- reviews (1)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (1)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (61)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (19)

- VA Home Loans (20)

- VA Loans (31)

- Va Loans & Financing (26)

- Veterans (5)

- Veterans Resources (38)

Recent Posts