How to Get a Real Home Valuation (Not a Zestimate) in San Antonio in 2026

Last Updated: June 8, 2026 | By Christopher Beal, U.S. Army Veteran & REALTOR

How to Get a Real Home Valuation (Not a Zestimate) in San Antonio in 2026

Key Takeaways

- A real home valuation in San Antonio is a broker CMA built from SABOR sold comps, not a Zestimate or other automated estimate (AVM).

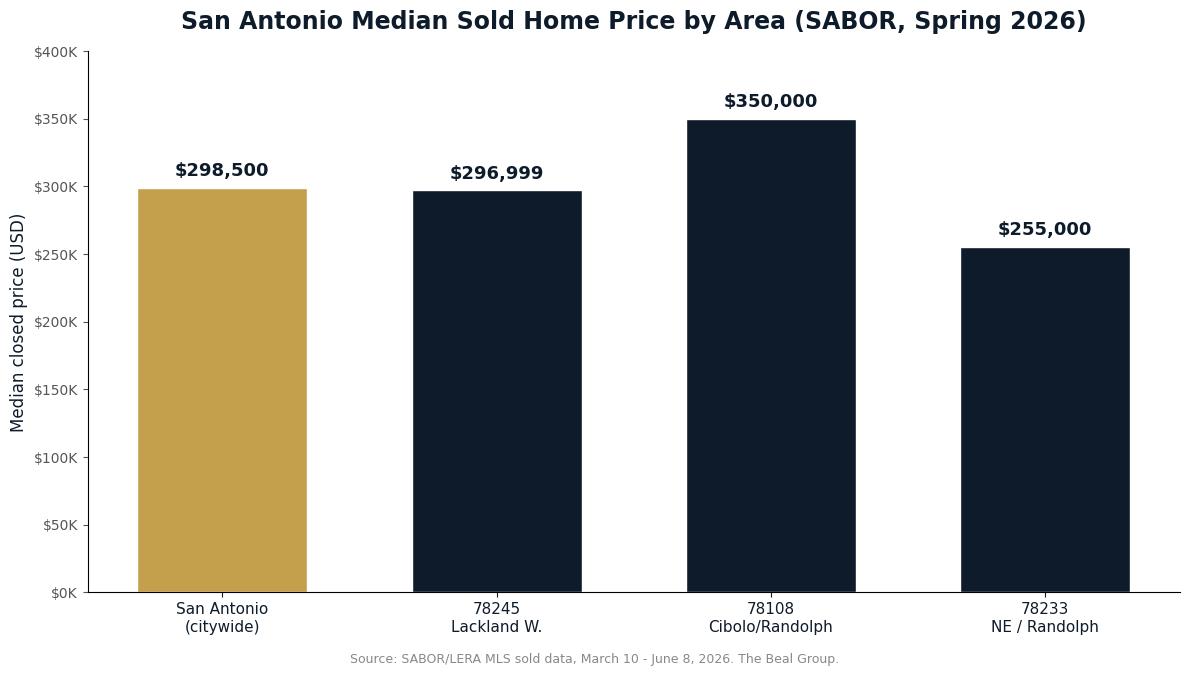

- San Antonio homes sold at a median of $298,500 and closed at about 97.2 percent of list price over the spring 2026 window, but medians swing from $255,000 in 78233 to $350,000 in 78108.

- Algorithms misread military ZIP codes near Joint Base San Antonio because they cannot see VA-buyer demand, BAH-driven rent floors, or condition.

- A CMA, an AVM, and an appraisal answer different questions; PCS sellers need the CMA first to set price and time a listing against a report date.

- The Beal Group prepares a CMA-grade home valuation free for San Antonio sellers. Call (210) 882-8583.

In This Guide

- What a CMA Is and Why It Beats an AVM

- CMA vs Zestimate vs Appraisal: Who Uses Which and When

- Why Algorithms Misread Military ZIP Codes Near JBSA

- What a Broker Checks That Zillow Cannot See

- How PCS Sellers Should Time a Valuation Against Report Dates

- How to Request a Free CMA From a Veteran Broker

- FAQ: San Antonio Home Valuation

What Is a CMA and Why Does It Beat an AVM?

The difference is comparables versus correlations. When I build a CMA for a San Antonio seller, I pull closed sales from the San Antonio Board of REALTORS (SABOR) MLS, filter to homes that genuinely compete with yours, and adjust line by line: a converted garage, a 2026 roof, a cul-de-sac lot, a view of the greenbelt. An AVM cannot make those adjustments because it never sees the home. It infers value from square footage, lot size, and the last recorded sale price, then leans on a metro-wide trend to fill the gaps.

That gap matters in a market like ours. Across San Antonio, the median home sold for $298,500 over the spring 2026 window, with an average of 79 days on market and a close-to-list ratio near 97.2 percent. But a citywide median is useless for pricing a single house. In ZIP code 78108 near Cibolo and Randolph, the median close was $350,000; in 78233 on the northeast side, it was $255,000. A blended algorithm that splits the difference will overprice one home and underprice the other, and both errors cost the seller real money.

Planning a PCS to JBSA and need to sell first? Christopher Beal specializes in military relocation across San Antonio — learn more.

CMA vs Zestimate vs Appraisal: Who Uses Which and When?

Each tool exists for a different reader. A Zestimate and similar automated valuation models serve a curious browser who wants a number now. A CMA serves a seller deciding what to list at. An appraisal serves a lender deciding how much to lend. The Consumer Financial Protection Bureau notes that an appraisal is an independent, licensed opinion ordered to protect the loan, not the sale price; it usually arrives after you are already under contract.

| Tool | Who Builds It | Best Use | Cost |

|---|---|---|---|

| Zestimate / AVM | Software algorithm | Quick ballpark, early curiosity | Free |

| Broker CMA | Licensed agent or broker | Setting your list price to sell | Free from your agent |

| Licensed appraisal | Certified appraiser | Lender or VA loan protection | $500 to $700, buyer-paid on most VA loans |

Source: SABOR/LERA MLS, March to June 2026; Consumer Financial Protection Bureau appraisal guidance. Appraisal fees reflect typical Bexar County VA transactions.

The mistake I see most often is a seller anchoring to a Zestimate and refusing a CMA that says something different. The algorithm is not wrong on purpose; it simply cannot see the things that move a real buyer. That is the whole reason the next two sections exist.

Why Do Algorithms Misread Military ZIP Codes Near JBSA?

Algorithms learn from history, and military ZIPs do not behave like the metro. Take 78245 on the far west side near Lackland AFB: it posted a $296,999 median close and a 98.7 percent close-to-list ratio over spring 2026, with an average 92 days on market. That ZIP is heavy with new construction, where a builder's incentives, lot premiums, and phase pricing scramble the comparable picture an AVM relies on. Two houses with identical square footage can close $30,000 apart because one came with a builder rate buydown and the other did not.

Now compare 78108 near Cibolo and Randolph AFB, where the median close hit $350,000 at a 98.2 percent close-to-list ratio. Demand there is anchored by Randolph commuters and Comal County schools, not by anything the algorithm can read from a tax record. Meanwhile 78233, closer in on the northeast side, posted a $255,000 median at 97.6 percent of list. Three ZIP codes, three different buyers, one algorithm trying to average them all.

What Does a Broker Check That Zillow Cannot See?

A CMA is a series of judgment calls an algorithm is not allowed to make. When I value a San Antonio home, I am answering questions Zillow cannot: Is the primary suite down? Does the lot back to a greenbelt or a retention pond? Is the kitchen original to a 2006 build, or was it redone last year? How many directly comparable homes are active right now, and what are they asking? The active median list price across San Antonio sat near $308,125 this spring, above the $298,500 sold median, which tells a broker that some sellers are still chasing the market down. That is a pricing signal, not a data point an AVM weighs.

- Condition and updates: roof age, HVAC, flooring, kitchen and bath finishes, and deferred maintenance that a buyer will discount.

- Location nuance: cul-de-sac vs through street, gate proximity, school attendance zone, and noise or flood exposure.

- Live competition: how many comparable homes are active, pending, and recently expired in your exact submarket.

- Buyer pool: whether VA, conventional, FHA, or cash buyers dominate your price band and ZIP.

Here is a real adjustment most algorithms get wrong. Say two homes in 78108 each closed near the $350,000 median, but one sat on a standard interior lot and the other backed to a greenbelt with no rear neighbor. A buyer in that market will routinely pay $8,000 to $15,000 more for the greenbelt lot, so a CMA adjusts the interior-lot comp upward to reflect what your greenbelt home is actually worth. An AVM treats both as the same lot because the tax record does not flag the view. Multiply that blind spot across a converted garage, a 2026 roof, or a re-done primary bath, and the gap between an automated estimate and a defensible list price can easily reach five figures on a mid-priced San Antonio home.

Want the number that reflects your actual home? Request a free home evaluation and a same-week CMA, or call (210) 882-8583.

How Should PCS Sellers Time a Valuation Against Report Dates?

PCS orders set the clock, and the math is unforgiving. If San Antonio homes are averaging 79 days from list to close, and you need a clean closing before your report date, you cannot start the valuation conversation the week your movers arrive. I tell every military seller to get a CMA the moment orders look likely. An early valuation lets you decide whether to list at 90, 60, or 30 days out, and whether a small repair or a price adjustment will protect your timeline.

This is also where the keep, sell, or rent decision gets made on real numbers rather than a guess. A CMA tells you your likely net; a rent analysis tells you your likely cash flow. You cannot compare them without the valuation first.

For the full selling timeline, see how to sell a San Antonio home in under 60 days for a fall PCS, and how to sync the sale with a purchase in the PCS to JBSA timeline for when to list, buy, and close. For market direction, check the San Antonio housing market forecast for 2026.

How Do You Request a Free CMA From a Veteran Broker?

A good valuation is a conversation, not a form letter. When you request a CMA from The Beal Group, you get a real price range backed by named comparable sales, the close-to-list trend for your ZIP, and a net sheet that shows what you walk away with after commissions, title, and any concessions. For veteran sellers buying again, our Serve and Save program reduces closing costs on the purchase side, so the move pencils out as one plan rather than two transactions.

| Your Priority | Best Tool | Why |

|---|---|---|

| Quick curiosity | Zestimate / AVM | Instant, free, no commitment, but unadjusted |

| Setting a list price | Broker CMA | Adjusted comps, live competition, net sheet |

| Loan protection under contract | Licensed appraisal | Independent, lender-ordered, VA-compliant |

Source: The Beal Group seller workflow; SABOR/LERA MLS, 2026.

About the Author: Christopher Beal

Christopher Beal is the owner and broker of Veteran Real Estate San Antonio: The Beal Group at eXp Realty, and a U.S. Army veteran (TREC License #723559). He holds the Military Relocation Professional (MRP) certification, is a member of the Veterans Association of Real Estate Professionals (VAREP), and has been named to the San Antonio Business Journal Top 25 and recognized as a six-time eXp ICON agent. Christopher and The Beal Group have closed more than 293 homes representing over $112 million in volume, with a focus on military and veteran buyers and sellers, PCS moves, VA loans, and listings across Bexar, Comal, Kendall, Medina, and Bandera counties. His Serve and Save program reduces closing costs for the veterans and military families he serves. Reach him at (210) 882-8583 or [email protected].

Explore More Resources

- VA Home Loans in San Antonio

- Military Relocation Services

- Free Home Evaluation

- Serve and Save Program

- Client Reviews

- About Christopher Beal

For broader market context, the FHFA House Price Index tracks regional price trends, the Consumer Financial Protection Bureau explains appraisals and the closing process, and the San Antonio Board of REALTORS (SABOR) publishes local market reports.

FAQ: San Antonio Home Valuation

Is a Zestimate accurate in San Antonio?

A Zestimate is a useful ballpark but not a list-price tool. It cannot adjust for condition, updates, lot, or the live buyer pool, and it tends to misread military ZIP codes near JBSA where new construction and VA demand dominate. Use it for curiosity, then get a broker CMA before you price.

How much does a home valuation cost in San Antonio?

A broker CMA is free from your agent. A Zestimate or AVM is free online. A licensed appraisal costs roughly $500 to $700 and is ordered by the lender once you are under contract.

What is the difference between a CMA and an appraisal?

A CMA is a broker's price opinion used to set a list price and is free. An appraisal is an independent, licensed opinion ordered by the lender to protect the loan, and it usually happens after you accept an offer.

What is the median home price in San Antonio in 2026?

The citywide median sold price was about $298,500 over the March to June 2026 window, with homes closing near 97.2 percent of list price. Medians vary widely by ZIP, from $255,000 in 78233 to $350,000 in 78108.

Why do home values differ so much between San Antonio ZIP codes?

Different ZIPs serve different buyers. Areas near Lackland like 78245 are new-construction heavy, while 78108 near Randolph draws commuters and Comal County school demand. A CMA prices your exact submarket; a metro average does not.

How long does it take to get a CMA?

The Beal Group typically returns a CMA within a few days of receiving your address and a short note on any updates. There is no cost and no obligation.

When should a PCS seller get a home valuation?

Get the CMA 60 to 90 days before your report date. With an average 79 days on market in San Antonio, an early valuation gives you room to price, prep, and close without overlapping housing costs.

Does a CMA tell me my net proceeds?

Yes. A complete CMA from The Beal Group includes a net sheet showing your estimated walkaway after commissions, title costs, and any buyer concessions, so you can compare selling against renting on real numbers.

Can I trust an online estimate for a VA-financed sale?

Not for pricing. VA buyers and the VA appraisal both respond to condition and comparable sales an AVM cannot see. A broker CMA aligns your list price with what a VA appraisal is likely to support, which protects your contract.

Get a real number on your San Antonio home today. Call Christopher Beal at (210) 882-8583, email [email protected], or visit veteranrealestatesa.com to request your free CMA.

Categories

- All Blogs (319)

- Alamo Heights (4)

- awards (3)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (76)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (24)

- Market Trends (5)

- Market Update (13)

- Military Relocation (94)

- Military Retirement (3)

- Mortgage (18)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (27)

- Real Estate (32)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (65)

- San Antonio, Veterans Resources, VA Loans (5)

- Seller (25)

- VA Home Loans (28)

- VA Loans (33)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts