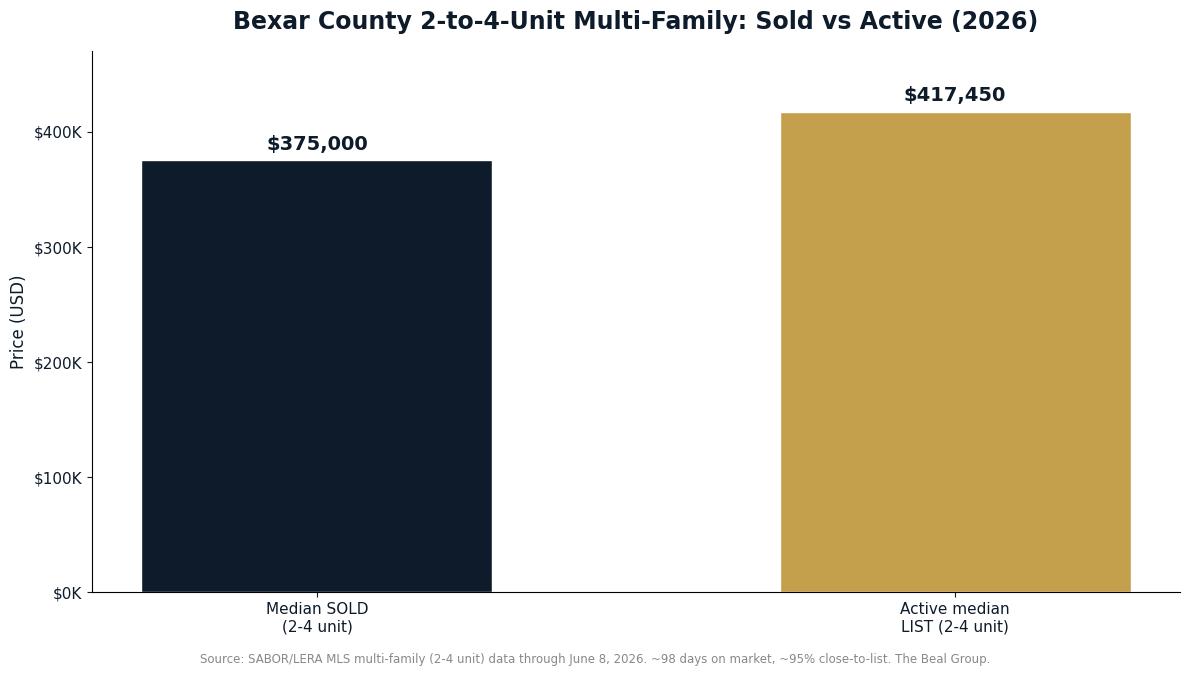

Texas Vet Loan vs VA Loan in San Antonio (2026): Which Should a Veteran Use?

LAST UPDATED: JUNE 15, 2026 | BY CHRISTOPHER BEAL, U.S. ARMY VETERAN & REALTOR

Texas Vet Loan vs VA Loan in San Antonio (2026): Which Should a Veteran Use?

Key Takeaways

- The "Texas Vet Loan" is the Texas Veterans Land Board (VLB) Veterans Housing Assistance Program, a state program. The VA loan is a separate federal benefit. They are not the same thing.

- You usually do not have to choose. In most San Antonio purchases a veteran can pair the VLB below-market rate with a VA-backed loan to get a discounted rate AND zero down payment.

- The Texas Vet Loan sets its interest rate weekly through the VLB and adds an extra 0.5 percent discount for veterans rated 30 percent or higher in service-connected disability.

- Only the Texas Vet Land Loan can finance raw Hill Country acreage. A standard VA loan cannot buy bare land.

- Both are for a primary residence. Christopher Beal, a U.S. Army veteran and San Antonio Realtor, helps Bexar, Comal, Kendall, Medina, and Bandera County veterans line up the right combination.

In This Guide

- What Is the Texas Vet Loan, and How Is It Different From a VA Loan?

- Can You Combine a Texas Vet Loan With a VA Loan in San Antonio?

- How Do the Rates and Costs Compare in 2026?

- Who Qualifies for the Texas Veterans Land Board Loan?

- What About the Texas Vet Land Loan for Hill Country Property?

- Which Loan Is Better for Your San Antonio Home Purchase?

What Is the Texas Vet Loan, and How Is It Different From a VA Loan?

The two programs solve different problems. The Texas Veterans Land Board, known as the VLB, is a division of the Texas General Land Office. It runs the Veterans Housing Assistance Program, which most people in San Antonio simply call the "Texas Vet Loan." The U.S. Department of Veterans Affairs runs the VA loan, a federal mortgage benefit available to qualified veterans nationwide.

The VLB sets its own interest rate every week, and that rate is frequently lower than the going market rate for a comparable mortgage. Because Texas funds the program through bond sales, it can pass a rate advantage on to veterans who served. The VA loan does not set a rate at all. Instead, it guarantees a portion of your loan so a private lender will offer zero down payment with no private mortgage insurance.

Both programs require the home to be your primary residence, and both are built for veterans, not investors. That overlap is exactly why so many San Antonio buyers ask which one to use, when the better question is often how to use them together. For a full walkthrough of the federal side, see our VA loan pre-approval guide for San Antonio.

Can You Combine a Texas Vet Loan With a VA Loan in San Antonio?

This is the insight most generic guides miss. The Texas Vet Loan is not always an either-or choice against the VA loan. The VLB participates as the funding source, and your lender can layer the VLB program on top of a VA-guaranteed loan. When that happens, you get the VLB weekly rate and the VA benefits in a single mortgage.

The VLB program can also be paired with an FHA or conventional loan if a veteran does not have VA entitlement available, which is useful for someone who already has an active VA loan on another property. That flexibility matters for service members at Joint Base San Antonio who bought once already and are buying again after a permanent change of station.

One caution: not every lender is set up to originate VLB loans, and the program has its own paperwork and timelines. Working with a San Antonio agent and a VLB-participating lender from the start keeps a permanent change of station closing on schedule. Our San Antonio VA loan closing cost guide breaks down what to expect at the table.

How Do the Rates and Costs Compare in 2026?

Rates move, so compare them the week you lock. The VLB publishes its current rate every week at vlb.texas.gov, and it adds an extra 0.5 percent discount for veterans with a service-connected disability rating of 30 percent or higher. A VA loan rate is whatever your private lender quotes, which varies by lender and credit profile.

| Feature | Texas Vet Loan (VLB) | VA Loan (Federal) |

|---|---|---|

| Who runs it | Texas Veterans Land Board (state) | U.S. Department of Veterans Affairs (federal) |

| Interest rate | Set weekly by the VLB, often below market; extra 0.5% off for 30%+ disability rating | Set by your private lender; competitive but not state-subsidized |

| Down payment | Depends on the loan it is paired with | Zero down with full entitlement |

| Mortgage insurance | Depends on the paired loan | No PMI ever |

| Funding fee | No VA funding fee on its own; capped origination fee applies | VA funding fee applies, waived for disabled veterans |

| Raw land | Yes, through the separate Texas Vet Land Loan | No, cannot finance bare land |

| Where it can be used | Texas property only | Anywhere in the United States |

| Reusable | Yes, per program rules | Yes, entitlement can be restored and reused |

Source: Texas Veterans Land Board (vlb.texas.gov) and U.S. Department of Veterans Affairs (va.gov), program terms current as of June 2026. Confirm the current weekly VLB rate and fee schedule before you lock.

On the cost side, the VA loan removes the down payment entirely with full entitlement, and the VA funding fee is fully waived for veterans receiving compensation for a service-connected disability. That is why pairing the two is so powerful: the VLB trims the rate while the VA structure removes the down payment and PMI. Veterans should also remember the Texas veteran property tax exemptions that can lower the monthly payment further.

Who Qualifies for the Texas Veterans Land Board Loan?

Texas residency is the dividing line. The VLB program is for veterans, military members, and qualifying spouses who are tied to Texas, while the VA loan follows you to any state. For a service member stationed at Joint Base San Antonio who plans to put down roots in Bexar County, that Texas focus is a feature, not a limitation.

General eligibility for the Texas Vet Loan typically includes a few key conditions, which the VLB verifies on application:

- Texas residency at the time of the loan application.

- Qualifying military service with a discharge characterized as honorable, or current active-duty status.

- Texas National Guard and Reserve members may qualify under current program rules.

- Surviving spouses of veterans who died in service or from a service-connected cause may be eligible.

The VA loan has its own service requirements based on length and period of service, and it is documented through your Certificate of Eligibility. Because the two programs check eligibility separately, a veteran can be approved for one, the other, or both. The official benefit details live at the VA home loans benefits page and at the Texas Veterans Land Board.

What About the Texas Vet Land Loan for Hill Country Property?

This is where the two programs stop overlapping. The Texas Veterans Land Board also runs a Land Loan program for veterans who want to buy rural Texas land, typically of at least one acre, with legal access. It requires a modest down payment, and the VLB sets the loan cap and terms, which it updates over time. A standard VA purchase loan is for a move-in-ready primary residence, so it cannot fund a raw lot.

For veterans dreaming of acreage in Comal, Kendall, Medina, or Bandera County, the land loan opens a door the VA loan never could. If you later build a home on that land, different financing comes into play. Our guide to buying land in the Texas Hill Country walks through how veterans approach rural purchases near San Antonio.

Which Loan Is Better for Your San Antonio Home Purchase?

Match the loan to your priority. There is no single winner, because the programs reward different goals. The table below lines up common veteran priorities in San Antonio with the smart pick.

| Your Priority | Best Pick | Why |

|---|---|---|

| Lowest interest rate | Texas Vet Loan (VLB) | Weekly below-market rate plus the 30%+ disability discount |

| Zero down payment | VA loan | Full entitlement means no down payment and no PMI |

| Lowest rate AND zero down | Both, combined | VLB-funded VA loan captures the rate and the structure |

| Buying out of state next PCS | VA loan | VA works nationwide; the VLB program is Texas only |

| Hill Country acreage | Texas Vet Land Loan | The only veteran program that finances raw land |

| Already used VA entitlement | Texas Vet Loan with conventional | VLB rate without needing available VA entitlement |

Source: program comparison by Christopher Beal, The Beal Group, based on VLB and VA program terms current as of June 2026.

The honest takeaway is that a quick conversation about your entitlement, your disability rating, and your timeline usually points to a clear answer in minutes. Request a free home evaluation to understand your buying power, or call Christopher Beal at (210) 882-8583 to map the right combination. Veterans buying their first San Antonio home should also ask about the Serve and Save program, which reduces closing costs for those who served.

About the Author: Christopher Beal

Christopher Beal is a U.S. Army veteran and the owner and broker of The Beal Group, also known as Veteran Real Estate San Antonio. He specializes in serving military and veteran buyers and sellers across San Antonio and the surrounding counties, including Bexar, Comal, Kendall, Medina, and Bandera. His practice focuses on permanent change of station moves, VA loans, and the financing programs unique to Texas veterans, including the Texas Veterans Land Board options covered in this guide.

As a veteran who has navigated military moves personally, Christopher helps service members at Joint Base San Antonio, including Lackland, Randolph, and Fort Sam Houston, line up the right loan strategy before they ever tour a home. His goal is simple: make sure every veteran captures every benefit they earned. You can reach him at (210) 882-8583 or read Christopher's full credentials.

Explore More Resources

- VA Home Loans

- Military Relocation

- Free Home Evaluation

- Serve and Save

- Client Reviews

- About Christopher

Frequently Asked Questions

Is the Texas Vet Loan the same as a VA loan?

No. The Texas Vet Loan is the Texas Veterans Land Board Veterans Housing Assistance Program, a state program that often offers a below-market interest rate. The VA loan is a separate federal benefit that guarantees zero-down financing. They are different programs that can be used together.

Can I use a Texas Vet Loan and a VA loan at the same time in San Antonio?

Yes. The VLB program can fund a VA-guaranteed loan, so a qualified veteran can get the VLB below-market rate and the VA zero-down, no-PMI structure in one mortgage. A VLB-participating lender sets this up.

Does the Texas Vet Loan have a disability discount?

Yes. Veterans with a service-connected disability rating of 30 percent or higher receive an additional 0.5 percent off the VLB interest rate, on top of the program's already discounted weekly rate.

Can a VA loan buy land in the Texas Hill Country?

No. A standard VA purchase loan is for a move-in-ready primary residence and cannot finance bare land. The Texas Vet Land Loan is the veteran program for raw Texas acreage of at least one acre with legal access.

Who qualifies for the Texas Veterans Land Board loan?

Generally, Texas residents with qualifying military service and a discharge under honorable conditions, plus many active-duty members, Texas National Guard members, and certain surviving spouses. The VLB confirms final eligibility at application.

Is the Texas Vet Loan only for first-time buyers?

No. The program is not limited to first-time buyers, though the home must be your primary residence. It can be reused under current program rules, which is helpful for veterans buying again after a permanent change of station.

Where do I find the current Texas Vet Loan interest rate?

The Texas Veterans Land Board publishes its current rate every week at vlb.texas.gov. Because the rate changes weekly, compare it against your VA lender quote in the same week you plan to lock.

Does the Texas Vet Loan charge a VA funding fee?

The VLB program itself does not charge the VA funding fee. If it is paired with a VA-guaranteed loan, the VA funding fee rules apply to that loan, and the fee is waived for veterans receiving compensation for a service-connected disability.

Can I use the Texas Vet Loan outside of Texas?

No. The Texas Vet Loan finances Texas property only. If your next move takes you out of state, the federal VA loan is the benefit that follows you anywhere in the United States.

How do I decide which loan to use for my San Antonio purchase?

It comes down to your VA entitlement, your disability rating, and whether land is involved. For most San Antonio veterans buying a primary home, a VLB-funded VA loan is the strongest combination. A short call with Christopher Beal at (210) 882-8583 usually clarifies the best path quickly.

Ready to Compare Your Options?

Buying a home in San Antonio as a veteran should start with the right loan strategy, not a guess. Here is how to take the next step today:

Request a free, no-obligation home evaluation to understand your buying power across Bexar, Comal, Kendall, Medina, and Bandera County. Visit veteranrealestatesa.com/home-evaluation.

Get matched with a VLB-participating lender so you can compare the current Texas Vet Loan rate against a VA quote in the same week.

Call Christopher Beal, U.S. Army veteran and San Antonio Realtor, at (210) 882-8583 to build a plan that captures every benefit you

Categories

- All Blogs (284)

- Alamo Heights (3)

- awards (2)

- Best Neighborhoods in San Antonio (13)

- Buyer (12)

- Buyer Education (59)

- Community Events (4)

- Hill Country (10)

- JBSA (33)

- Local Guide (5)

- Luxury (21)

- Luxury Real Estate (19)

- Market Trends (1)

- Market Update (12)

- Military Relocation (92)

- Military Retirement (3)

- Mortgage (7)

- Neighborhood Guides (16)

- neighborhoods (5)

- New Construction (15)

- PCS (25)

- Real Estate (29)

- reviews (1)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (1)

- San Antonio Neighborhoods (38)

- San Antonio Real Estate (60)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (16)

- VA Home Loans (14)

- VA Loans (24)

- Va Loans & Financing (26)

- Veterans (3)

- Veterans Resources (38)

Recent Posts