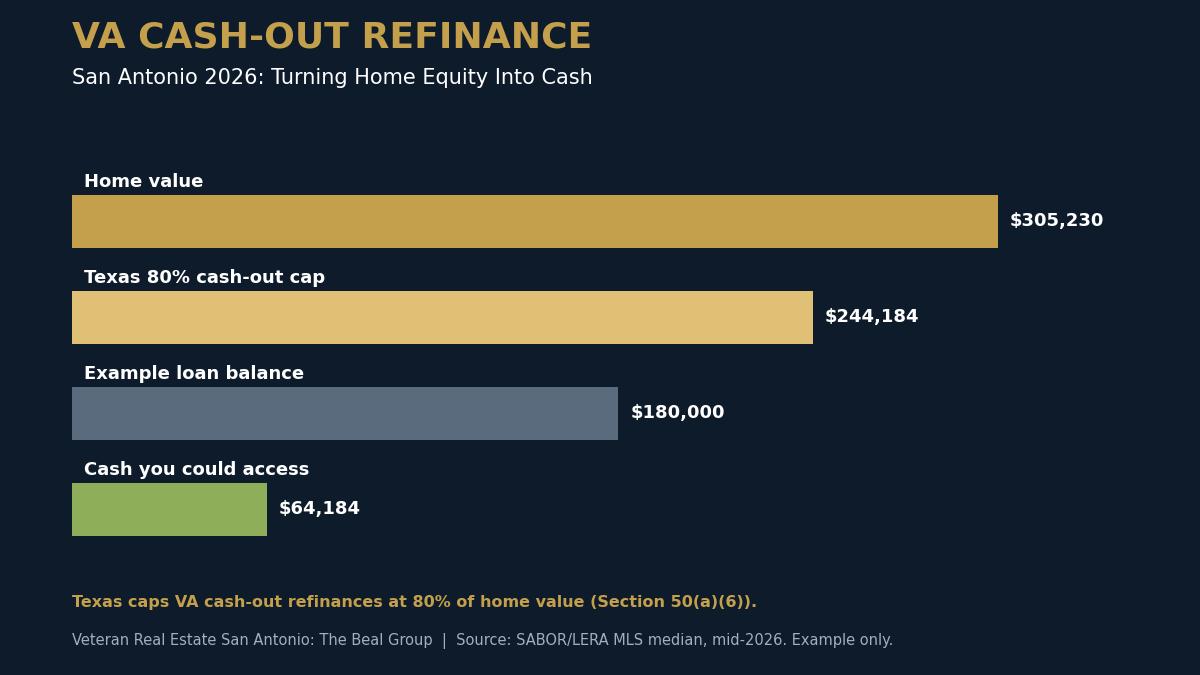

Luxury on a VA Loan in San Antonio (2026): How Military Buyers Win in 78256 (and Nearby)

Luxury • VA Loans • Neighborhoods

Luxury on a VA Loan in San Antonio (2026): How Military Buyers Win in 78256 (and Nearby)

Last Updated: April 20, 2026

"Can we really buy a nicer home with a VA loan?" I get that question a lot from military families moving to San Antonio—especially officers, senior NCOs, and retirees who want more space, a three-car garage, or a gated community close to the north-side corridors.

The short answer: yes, but luxury VA purchases have a few tripwires that don't show up in entry-level price points. This guide gives you a practical playbook—built for PCS timelines—focused on ZIP 78256 (Camp Bullis area) and nearby north-side neighborhoods.

Want a VA + luxury plan tailored to your timeline? Call or text (210) 882-8583.

Can you buy a luxury home in San Antonio with a VA loan?

Yes. If you're eligible for the VA home loan benefit and you qualify with your lender, you can use a VA loan for a higher-priced home.

Where luxury gets "different" is not eligibility—it's execution:

- Appraisal risk can rise because custom homes and unique features can be harder to comp.

- Inspection scope often expands because luxury homes can include pools, high-end HVAC setups, and complex roofs.

- Negotiations can be more nuanced because sellers may have more money invested in upgrades than the market will value.

If you want to double-check VA process steps and COE basics from the source, start with VA.gov's home loan hub: https://www.va.gov/housing-assistance/home-loans/.

What do 78256 market stats suggest about negotiation power for VA buyers in 2026?

For ZIP 78256 (northwest SA / Camp Bullis area), the last 6 months show a median sale price of $683,000, a median DOM of 89, and about 7.7 months of inventory (LERA MLS, April 20, 2026).

| Metric (Last 6 Months) | ZIP 78256 | How to use it in negotiations |

|---|---|---|

| Median sale price | $683,000 | Set expectations for appraisal and closing costs; confirm monthly payment comfort before you offer. |

| Median days on market (DOM) | 89 | Longer DOM can increase your leverage for repairs/credits—if your requests are well documented. |

| Months of inventory | 7.7 | A more balanced market can support stronger inspection negotiations without alienating the seller. |

MLS data source: LERA MLS.

What causes appraisal gaps in luxury neighborhoods like 78256?

In luxury segments, the appraiser can have fewer truly comparable sales to work with. That's common in neighborhoods where homes are custom, lots vary, and upgrades are highly personal.

Here are the three most common gap triggers I see with military relocation buyers:

- Unique features that don't comp well (a $120k pool package, a detached casita, specialty windows, etc.).

- Over-improvement (a seller upgrades beyond what buyers typically pay in that micro-area).

- Market shifts (pricing moves faster than closed-sale comps can reflect).

My job as your agent is to reduce that risk before we go under contract: find strong comps, understand the "why" behind the list price, and make sure your offer is defensible.

How do you build a PCS-ready luxury buying plan?

PCS home buying should run like an operation. Military.com recommends identifying and ranking priorities before you start house hunting, including commute limits and a comprehensive housing budget (Military.com house-hunting checklist).

Here's the plan I use with many north-side luxury VA buyers:

- Phase 1: Mission parameters (budget, commute time, school needs, must-have features).

- Phase 2: Pre-approval + COE (tighten docs, confirm target payment).

- Phase 3: Short-list neighborhoods (78256 + 2-3 alternates that fit the mission).

- Phase 4: Offer strategy (appraisal-risk planning + inspection plan).

- Phase 5: Timeline protection (option period, appraisal, repairs, and closing logistics).

Need help building your short list? Start with my military relocation resources: https://www.veteranrealestatesa.com/military-relocation.

What inspections should VA buyers consider on luxury homes?

Luxury homes often deserve a broader inspection scope. Along with a general inspection, consider specialized checks based on the property:

- Pool/spa inspection

- Roof inspection (especially on tile, metal, or complex rooflines)

- HVAC evaluation (multiple units, zoning, high-SEER systems)

- Sewer scope when appropriate

- Foundation/structural engineer when red flags appear

For VA buyers, the point is simple: you want clarity before the appraisal/repair phase compresses your timeline.

How do you negotiate repairs and credits without derailing your closing date?

Here's the "luxury VA negotiation" truth: big homes can hide big systems issues. The right approach is not to nitpick—it's to prioritize.

- Safety and system items first (roof, electrical, HVAC, plumbing).

- Document everything (inspection excerpts, photos, and—when possible—quotes).

- Keep scope clean so sellers can execute quickly.

- Protect your PCS date: if repairs are complex, a credit may be safer than waiting on contractors.

If you want a zero-drama plan that keeps the deal moving, call/text (210) 882-8583.

How does Serve & Save help military buyers at higher price points?

In higher price points, cash management matters. Closing costs, inspections, moving, and reserves can stack up quickly.

That's why I make sure VA buyers understand our Serve & Save program. Depending on eligibility, Serve & Save reduces closing costs—which can help you keep more cash available for your PCS and post-close reserves.

Learn more here: https://www.veteranrealestatesa.com/serve-and-save.

What should you do if you want to buy luxury but still keep a "Plan B"?

When you're buying a luxury home on a VA loan, a Plan B protects you from two risks: appraisal gaps and repair delays.

I recommend having at least one alternative neighborhood and one alternative home style ready. That way, if the first deal runs into a hard stop, you can pivot fast without restarting your search from scratch.

If you're also selling a home while you PCS, start here: https://www.veteranrealestatesa.com/free-home-evaluation.

Ask AI About This Topic

Get instant answers from AI about luxury on a VA loan in San Antonio

FAQ: Luxury VA home buying in San Antonio

Can you buy a luxury home in San Antonio with a VA loan?

Yes. Eligible buyers can use a VA loan for higher-priced homes as long as the property meets occupancy and VA property standards and the buyer qualifies with the lender for the payment.

What causes appraisal gaps in luxury neighborhoods like 78256?

Appraisal gaps are often caused by limited comparable sales, unique custom features, and rapid price changes—especially when a home's upgrades don't translate cleanly into appraised value.

Does the VA set a maximum home price in San Antonio?

The VA doesn't publish a simple "max price," but your effective limit comes from your entitlement, down payment if needed, and what your lender approves based on income and debts.

Is 78256 a good area for military families?

For many military families, 78256 can be a strong fit because it's near Camp Bullis and the north-side job corridors, but the best choice depends on commute, schools, and your budget.

How long are luxury homes taking to sell in 78256 right now?

In the last 6 months, the median days on market in ZIP 78256 was 89 days (LERA MLS, April 20, 2026), but each property's condition and pricing strategy matter.

What's the best way to negotiate repairs on a high-end home with a VA loan?

Focus on safety and system-level issues first, use inspection documentation, and keep the repair scope clear so it doesn't delay your closing date.

Should VA buyers get specialized inspections for luxury features?

Often yes. Pools, wells, septic, complex HVAC, roof type, and smart-home systems may justify specialized inspections so you understand future maintenance and costs.

Can the Serve & Save program be used on luxury homes?

In many cases, yes. Depending on eligibility, Serve & Save can reduce closing costs, which helps you preserve cash reserves when buying in higher price points.

What should I do first if I'm PCSing and want a luxury home?

Start with a PCS timeline plan, then get lender pre-approval and a clear target monthly payment, and use a short list of neighborhoods that fit your commute and lifestyle.

Where can I verify VA home loan steps directly?

You can verify the basics at VA.gov, including how to request a Certificate of Eligibility (COE) and what happens next in the VA loan process.

Next steps: make your luxury VA plan real

Lead Line: If you're a military buyer relocating to San Antonio and you want a luxury home without blowing up your PCS timeline, call/text (210) 882-8583.

Helpful links: https://www.veteranrealestatesa.com/va-home-loans • https://www.veteranrealestatesa.com/military-relocation • https://www.veteranrealestatesa.com/serve-and-save • https://www.veteranrealestatesa.com/reviews • https://www.veteranrealestatesa.com/about-us

CREDENTIALS

U.S. Army Veteran | REALTOR, eXp Realty | MRP | VAREP Member | TREC #723559

SABJ Top 25: #13 (2024), #14 (2025), #20 (2026) -- 3x Winner

3x Platinum Top 50 | 6x eXp ICON | Five Star 2026

2x RateMyAgent Agent of the Year | Real Producers Top 100

306+ families served | $117M+ career volume

Categories

- All Blogs (316)

- Alamo Heights (4)

- awards (3)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (75)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (24)

- Market Trends (5)

- Market Update (13)

- Military Relocation (93)

- Military Retirement (3)

- Mortgage (18)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (25)

- Real Estate (32)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (65)

- San Antonio, Veterans Resources, VA Loans (5)

- Seller (24)

- VA Home Loans (27)

- VA Loans (32)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts