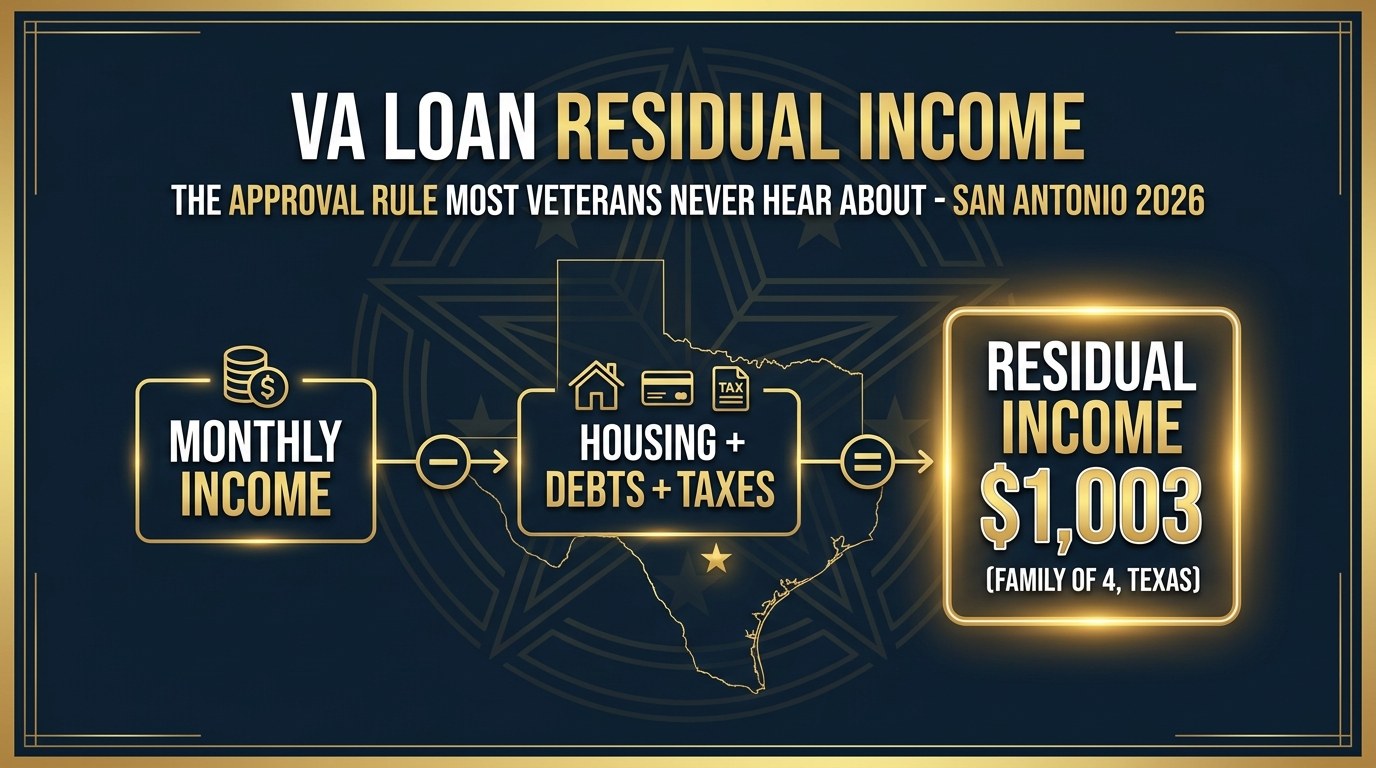

The Complete Guide to Home Buyer Programs for Veterans in San Antonio 2026

Last Updated: April 27, 2026 | By Christopher Beal, Veteran Real Estate San Antonio

The Complete Guide to Home Buyer Programs for Veterans in San Antonio 2026

Key Takeaways

- The VA Home Loan requires zero down payment and no PMI — the single most powerful purchase tool for eligible veterans in 2026.

- The Texas VLB home loan limit increased to $832,750 in January 2026; veterans with 30%+ VA disability rating get a 0.50% rate discount (5.85% vs. 6.35% base rate).

- 100% disabled veterans in Texas pay zero property taxes — on a median San Antonio home, that saves $5,000–$7,000 per year.

- The Serve & Save program reduces closing costs at 1% per year of service, up to 6% — stackable with all VA and state programs.

- A 100% disabled veteran stacking all programs can save $40,000+ in the first year of homeownership vs. a civilian buyer.

- The 78245 ZIP code (near JBSA-Lackland) has a median sale price of $289,994 and 884 active listings as of April 2026 — ideal inventory for VA buyers.

What Federal Programs Help Veterans Buy a Home in 2026?

The Department of Veterans Affairs administers a suite of home-buying benefits that go far beyond the standard VA home loan. Most veterans know about the zero-down purchase loan — but fewer know about the adapted housing grants, the streamline refinance, or the energy-efficient mortgage add-on. Here is the full picture of every federal program available to veteran buyers in San Antonio in 2026.

VA Home Loan — The Foundation of Every Veteran Purchase Strategy

The VA Home Loan is backed by the U.S. Department of Veterans Affairs and originated through VA-approved private lenders. In 2026, eligible veterans in San Antonio can use this benefit to purchase a primary residence with zero down payment, no private mortgage insurance (PMI), and competitive interest rates — without any loan limit tied to a cap, since full-entitlement veterans face no VA-imposed maximum. Key details for 2026:

- Zero down payment for veterans with full entitlement

- No PMI — saving veterans $100–$300/month vs. conventional loans

- VA Funding Fee: 2.15% (first use, no down payment); waived entirely for veterans with 10%+ VA service-connected disability rating

- Seller concession cap: Sellers (including builders) can contribute up to 4% of the loan amount toward the veteran's closing costs

- Eligibility: 90 days active duty during wartime, 181 days during peacetime, 6 years National Guard/Reserves, or surviving spouse of a service member who died in the line of duty

- Certificate of Eligibility (COE): Obtainable via VA.gov or through your lender

For a deeper dive into the VA Home Loan in San Antonio, see Christopher Beal's complete guide at veteranrealestatesa.com/va-home-loans or the step-by-step purchase walkthrough at the 2026 VA Buyer Guide.

VA IRRRL — The Streamline Refinance for Existing VA Loan Holders

The VA Interest Rate Reduction Refinance Loan (IRRRL) — commonly called the VA Streamline Refinance — allows veterans who already hold a VA-backed mortgage to refinance to a lower interest rate with minimal documentation. No appraisal is required in most cases. No income verification. No new Certificate of Eligibility needed. The refinanced loan must result in a lower interest rate (the exception is moving from an adjustable-rate mortgage to a fixed rate). The VA Funding Fee on an IRRRL is just 0.5%, and veterans with a qualifying disability rating may have the fee waived entirely. Veterans who locked in rates during higher-rate periods should evaluate their IRRRL eligibility with a VA-approved lender before rates shift further.

VA Native American Direct Loan (NADL)

The VA Native American Direct Loan (NADL) is a unique federal direct loan — not a guarantee — available to eligible Native American veterans purchasing, constructing, or improving a home on federal trust land. Unlike the standard VA loan (which is originated by private lenders), the VA funds the NADL directly. The tribal organization must have a Memorandum of Understanding (MOU) with the VA. For veterans purchasing non-trust-land property in San Antonio, the standard VA Home Loan is the appropriate program.

VA Adapted Housing Grants — SAH and SHA for Service-Connected Disabilities

Veterans with severe service-connected disabilities have access to two VA-administered housing adaptation grants in FY 2026 — and neither requires repayment. These are grants, not loans, and do not reduce your VA home loan entitlement:

- Specially Adapted Housing (SAH) Grant: Up to $109,986 in FY 2026. For veterans with loss of use of both lower extremities, certain spinal cord injuries, paralysis, or severe burns. Can be used to purchase, build, or substantially modify a home for full accessibility. Available up to 3 times within the lifetime cap.

- Special Home Adaptation (SHA) Grant: Up to $25,350 in FY 2026. For veterans with blindness, loss of use of both hands, or certain severe burns who need targeted modifications (roll-in showers, widened doorways, accessible kitchens). Available up to 6 times across a lifetime.

- Temporary Residence Adaptation (TRA) Grant: Up to $44,299 (SAH-eligible) or $7,256 (SHA-eligible) to modify a family member's home during the period before permanent housing is arranged.

Apply using VA Form 26-4555 through VA.gov's disability housing grants page. The VA assigns a housing agent to guide eligible veterans through the process at no cost.

VA Energy Efficient Mortgage (EEM)

The VA Energy Efficient Mortgage allows veterans to roll up to $6,000 of energy-efficient improvements directly into their VA purchase loan or IRRRL refinance — no separate application, no additional closing, and no appraisal for amounts under $6,000. Qualifying upgrades include solar heating and cooling systems, weatherstripping, storm windows, heat pumps, and insulation. For amounts above $6,000, an energy audit must document that the improvements will produce enough utility savings to offset the additional loan cost. At $6,000 rolled into a 30-year loan at 6.25%, the monthly payment increase is approximately $37 — often less than the monthly utility savings from the improvements themselves.

HUD-VASH — For Veterans Experiencing Housing Instability

The HUD-Veterans Affairs Supportive Housing (HUD-VASH) program combines Housing Choice Voucher (HCV) rental assistance with VA case management services for veterans experiencing homelessness or housing instability. In San Antonio, HUD-VASH vouchers are administered through the Housing Authority of Bexar County (HABC) at 4201 Medical Drive, Suite 280, San Antonio, TX 78229, reachable at (210) 616-9915. Veterans pay no more than 30% of their adjusted income toward rent; the HUD-VASH voucher covers the remainder. While HUD-VASH is a rental assistance program rather than a home-purchase program, it provides stable housing for veterans who need case management support before transitioning to homeownership.

Ready to Use Your VA Benefits?

Christopher Beal has guided 306+ veteran families through the VA purchase process in San Antonio. Call (210) 882-8583 or visit veteranrealestatesa.com/military-relocation for a free consultation.

What Texas State Programs Help Veteran Home Buyers in 2026?

Texas has some of the strongest veteran home-buying programs of any state in the nation — programs that LRG Realty's veteran guide glosses over with minimal detail. Here is the complete picture of every state-level advantage available to veteran buyers in the greater San Antonio area in 2026.

Texas Veterans Land Board (VLB) Veterans Housing Assistance Program (VHAP)

The Texas Veterans Land Board's Veterans Housing Assistance Program is a competitive fixed-rate home loan program available exclusively to Texas-resident veterans and military members. As of January 2026, the VLB increased the maximum loan amount to $832,750, up from $806,500 in 2025 — a $26,250 increase. Key 2026 program details per the Texas General Land Office:

- Maximum loan: $832,750 (2026)

- Base interest rate: 6.35% fixed (as of early 2026; adjusts weekly)

- Disability discount rate: 5.85% fixed for veterans with 30%+ VA disability rating (0.50% reduction)

- Down payment: Little to none when combined with VA financing

- Loan terms: 15, 20, 25, or 30 years (fixed rate)

- Occupancy requirement: Must be your Texas primary residence; must occupy within 60 days; must remain primary residence for at least 3 years

- Eligibility: Texas resident veteran, 18+, honorable/general/medical discharge, minimum 90 days active duty

- Refinance: VLB does NOT offer a refinance option — for refinancing, veterans must use VA IRRRL or conventional products

Important note for military families: The VLB's 3-year primary residence requirement can conflict with PCS orders. Veterans who anticipate orders within 3 years should carefully compare the VLB against a standard VA loan, which has no such restriction. Christopher Beal helps veteran buyers make this analysis before committing. Call (210) 882-8583 to run the numbers for your specific situation.

VLB Home Improvement Loan

The VLB also offers a home improvement loan of up to $50,000 for repairs, upgrades, and accessibility improvements to an existing home. No down payment is required. Veterans with a 30%+ VA disability rating qualify for a discounted interest rate on this program as well. Fixed-rate terms range from 2 to 20 years. An application fee ($10 flood certification + $125 title search) is required at the time of application. This program is particularly valuable for veterans modifying an existing home for accessibility needs that fall below the SAH/SHA grant thresholds.

Texas Veteran Property Tax Exemption — The Silent Wealth Builder

Texas provides property tax exemptions to veterans with VA disability ratings of 10% or greater. Per the Texas Comptroller of Public Accounts and the Texas Veterans Commission, the 2026 exemption tiers are:

| VA Disability Rating | Property Tax Exemption | Annual Savings (est., SA) |

|---|---|---|

| 10–29% | $5,000 off assessed value | ~$110–$130/yr |

| 30–49% | $7,500 off assessed value | ~$165–$195/yr |

| 50–69% | $10,000 off assessed value | ~$220–$260/yr |

| 70–99% | $12,000 off assessed value | ~$264–$312/yr |

| 100% (or unemployability) | Full exemption — $0 property taxes | $5,000–$7,000+/yr |

To claim the exemption, submit your VA award letter to the Bexar County Appraisal District (BCAD). The exemption applies to your primary residence only. Surviving spouses of veterans who died in service or from a service-connected disability may also qualify.

Disabled Veteran's Residence Homestead Exemption

In addition to the disability-rating-based exemption above, Texas also provides a separate Residence Homestead Exemption for 100% disabled veterans that is distinct from the standard homestead exemption. This exemption removes the entire taxable value of the property for school district property taxes — which represent the largest component of Texas property tax bills. Combined with the standard homestead exemption, a 100% disabled veteran in Bexar County effectively pays zero property taxes on their primary residence. The surviving spouse of a 100% disabled veteran may also be eligible to continue receiving this exemption, provided they have not remarried.

What San Antonio Local Programs Exist for Veteran Home Buyers?

Beyond federal and state programs, San Antonio has a robust local support infrastructure for veteran homebuyers. Joint Base San Antonio (JBSA) — encompassing JBSA-Lackland, JBSA-Randolph, JBSA-Fort Sam Houston, and Camp Bullis — makes San Antonio one of the largest military communities in the United States, and the city's support programs reflect that reality.

Bexar County Veterans Services Office

The Bexar County Veterans Services Office provides free assistance to veterans and their families navigating VA benefits, disability claims, and housing resources. County Veterans Service Officers (CVSOs) can help veterans obtain their Certificate of Eligibility, file disability claims that affect property tax exemption eligibility, and connect veterans with state and local housing programs. Veterans who do not yet have a disability rating — or whose rating does not yet reflect their full service-connected conditions — should consult a CVSO before completing a home purchase, as a pending or recently increased disability rating can meaningfully change program eligibility and funding fee status.

Housing Authority of Bexar County (HABC) — HUD-VASH Administration

The Housing Authority of Bexar County (HABC) administers HUD-VASH vouchers for veteran households in Bexar County. Located at 4201 Medical Drive, Suite 280, San Antonio, TX 78229, the HABC accepts veteran referrals directly from the VA at (210) 616-9915. For veterans who are transitioning from rental assistance toward homeownership, HABC case managers can help create a financial roadmap toward VA loan eligibility, including credit improvement and savings planning.

VAREP — HUD-Approved Housing Counseling for Veterans

The Veterans Association of Real Estate Professionals (VAREP) is a HUD-approved 501(c)(3) nonprofit organization that provides free housing counseling, financial literacy workshops, and homeownership education specifically for veterans and military families. VAREP's HUD-approved housing counseling services can help veterans prepare for homeownership, understand their loan options, and navigate the home-buying process. Christopher Beal is a VAREP member — the organization represents a trusted alliance of real estate professionals committed to veteran housing. Learn more at varep.net.

What Real Estate-Specific Programs and Strategies Help Veteran Buyers?

The Beal Group Serve & Save Program — Reduces Closing Costs Up to 6%

The Serve & Save program is The Beal Group's commitment to the veteran and military community in San Antonio. The program reduces closing costs at 1% per year of military service, up to a maximum of 6%. This benefit is applied directly toward what the veteran pays at closing — it is not a cash payment or rebate, but rather a reduction in the out-of-pocket costs a veteran incurs when purchasing a home. For a $290,000 home, a veteran with 6 or more years of service could see closing costs reduced by approximately $17,400. Learn more and calculate your benefit at veteranrealestatesa.com/serve-and-save.

Builder Incentives for VA Buyers in San Antonio

San Antonio's new construction market — with major builders including DR Horton, Lennar, Perry Homes, Pulte, and Meritage — is actively courting VA buyers. Under VA loan rules, builders (as sellers) can contribute up to 4% of the loan amount in concessions toward a veteran buyer's closing costs. Many builders also offer interest rate buy-downs, mortgage points, and option upgrades as incentives. In 2026, DR Horton's communities near JBSA-Lackland in the 78245 ZIP code (Brookmill, Arcadia Ridge, Stonehill) have significant inventory in the $260,000–$330,000 range — squarely within the reach of E-5 through O-3 BAH.

Critical warning: The builder's on-site sales agent represents the builder — not the veteran buyer. Veterans who walk into a model home without a buyer's agent forfeit significant negotiating power. Christopher Beal represents veteran buyers with all major San Antonio builders at no cost to the veteran — the builder pays the buyer's agent commission. Call (210) 882-8583 before visiting any builder's model home.

Seller Concession Cap for VA Buyers — 4%

VA loan rules permit sellers to contribute up to 4% of the appraised value toward a veteran buyer's closing costs, prepaid expenses, and discount points. This is in addition to the standard closing cost contribution. In a buyer's market with 6 months of inventory like 78245 currently (per LERA MLS April 2026 data), negotiating full seller concessions is often realistic — particularly when combined with Serve & Save credits. An experienced veteran real estate agent knows how to structure the offer to maximize concessions within VA appraisal rules.

How Do All Veteran Home Buyer Programs Compare Side by Side?

Table 1: Federal + Texas Programs at a Glance

| Program | Who It's For | Max Benefit | Down Payment | Key Restriction |

|---|---|---|---|---|

| VA Home Loan | All eligible vets | No loan cap (full entitlement) | $0 | Primary residence only |

| VLB VHAP | Texas resident vets | $832,750 loan (2026) | $0 with VA | 3-yr primary residence; Texas only |

| VLB Home Improvement | Texas resident vets (existing home) | $50,000 loan | $0 | Existing home only; Texas |

| SAH Grant | Severely disabled vets | $109,986 grant | N/A (grant) | Qualifying disability required |

| SHA Grant | Vets w/ hand/vision disabilities | $25,350 grant | N/A (grant) | Qualifying disability required |

| VA IRRRL | Existing VA loan holders | Lower rate, minimal fees | N/A (refi) | Must lower rate (exc. ARM→fixed) |

| VA EEM | All VA loan borrowers | $6,000 added to loan | N/A (add-on) | Energy improvements only |

| TX Property Tax Exemption | Vets with 10%+ VA disability | Up to 100% tax exemption | N/A (tax benefit) | Primary residence only; TX |

| Serve & Save | All veteran buyers w/ Beal Group | Up to 6% closing cost reduction | N/A (closing credit) | Works with Beal Group |

Table 2: VA Loan vs VLB — When to Choose Each

| Your Situation | Best Fit | Why |

|---|---|---|

| Buying a Texas primary home, plan to stay 3+ years | VLB VHAP | Lower rate (esp. with 30%+ disability discount) |

| Buying in Texas but expect PCS orders within 3 years | VA Loan | No occupancy lock; easier to rent out or sell |

| 30%+ disability, staying 3+ years | Compare both | VLB rate discount vs VA funding fee waiver — run the math |

| Buying outside Texas (e.g., prior to returning to SA) | VA Loan | VLB is Texas-only |

| Want to refinance later if rates drop | VA Loan | VA IRRRL streamline available; VLB has no refinance |

| Repairing or upgrading existing home | VLB Home Improvement | Up to $50K, below-market rate, no down payment |

How Can a Veteran Stack These Programs to Maximize Savings?

The most powerful aspect of the veteran home-buying landscape in San Antonio is the ability to stack multiple programs simultaneously. Here is a real-scenario example of a 100% disabled veteran purchasing a home in the 78245 ZIP code near JBSA-Lackland in April 2026:

Scenario: 100% Disabled Veteran — Purchase Price $289,994

| VA Home Loan — zero down payment | $0 down |

| VA Funding Fee waiver (100% disability = exempt) | +$6,235 saved |

| No PMI vs. 5% down conventional ($290K loan) | +$145/mo saved |

| Serve & Save — 10 yrs of service × 1% = 6% max cap | −$17,400 closing costs |

| Seller concessions — 4% cap ($11,600) | −$11,600 closing costs |

| Texas property tax exemption — 100% disabled = $0 taxes | +$5,800/yr saved |

| First-Year Total Savings vs. Civilian Buyer | $41,035+ |

Note: Calculations are illustrative. Actual savings depend on purchase price, loan amount, years of service, disability rating, and market conditions. Based on LERA MLS data, April 2026 (ZIP 78245 median $289,994). VA Funding Fee of 2.15% shown for first-use reference, then waived for 100% disabled. Serve & Save applies maximum 6% cap regardless of service years beyond 6. Seller concession success depends on negotiation and market conditions.

A veteran with a 30%+ disability rating who uses the VLB VHAP instead of a standard VA loan at the same price adds another layer: the 0.50% rate discount from 6.35% to 5.85% saves approximately $88/month, or $31,680 over a 30-year loan — providing the 3-year occupancy requirement does not conflict with anticipated PCS orders.

What Do These Programs Actually Buy in San Antonio Right Now?

Programs are only useful when they translate to real homes. Here is what the current San Antonio market looks like in the ZIP code closest to JBSA-Lackland, based on live LERA MLS data as of April 27, 2026:

ZIP 78245 — Southwest San Antonio / JBSA-Lackland Corridor

Based on LERA MLS data, October 2025–April 2026

| Median Sale Price | $289,994 |

| Average Sale Price | $298,931 |

| Active Listings | 884 |

| Homes Sold (6 months) | 880 |

| Months of Inventory | 6.0 months (balanced market) |

| Median Days on Market | 77 days |

| Avg. Price Per Sq Ft | $150/sqft |

| List-to-Sale Ratio | 98.3% |

| New Listings (last 7 days) | 123 |

Top subdivisions by sales volume: Brookmill (97 sales), Stonehill (78), Tres Laurels (49), Arcadia Ridge (43), Ladera (39). Source: LERA MLS, October 2025–April 2026.

At the 2026 E-5 Basic Allowance for Housing (BAH) rate for San Antonio with dependents (approximately $2,214/month), a veteran using a VA loan at current market rates with zero down payment can target homes in the $270,000–$310,000 range — which aligns precisely with the median inventory in 78245. With 884 active listings and 6 months of inventory, buyers have real negotiating leverage, and seller concession requests up to 4% are routinely achievable in this market.

How Do You Get Started with All of These Programs?

Navigating multiple overlapping programs — federal, state, and local — is exactly the kind of complexity that separates a veteran-specialist REALTOR from a generalist agent. Christopher Beal is a U.S. Army veteran, Military Relocation Professional (MRP), and VAREP member who has guided 306+ veteran and military families through home purchases in San Antonio. His team understands VA appraisal requirements, VLB occupancy rules, Bexar County Appraisal District exemption filing, builder contract negotiations, and PCS-timeline management — all at once.

- U.S. Army Veteran

- REALTOR, eXp Realty — TREC #723559

- Military Relocation Professional (MRP) — Verified

- VAREP Member (Veterans Association of Real Estate Professionals — HUD-approved nonprofit)

- SABJ Top 25 Residential Real Estate Teams: #13 (2024), #14 (2025), #20 (2026) — 3× Winner

- Platinum Top 50 Agent — 3× Winner

- eXp ICON Agent — 6× Winner

- Five Star Real Estate Agent 2026

- 2× RateMyAgent Agent of the Year

- Real Producers Top 100

- 306+ families served | $117M+ career volume

Start your veteran home-buying journey with a free consultation. Christopher Beal will review every program you qualify for, run a Serve & Save calculation based on your years of service, and connect you with VA-approved lenders who understand both VA and VLB financing.

- Phone: (210) 882-8583

- Military Relocation: veteranrealestatesa.com/military-relocation

- VA Home Loans: veteranrealestatesa.com/va-home-loans

- Serve & Save Program: veteranrealestatesa.com/serve-and-save

- Client Reviews: veteranrealestatesa.com/reviews

- About Christopher: veteranrealestatesa.com/about-us

- Free Home Evaluation: veteranrealestatesa.com/free-home-evaluation

Ask AI About This Topic

Get instant answers from AI about veteran home buyer programs in San Antonio

Frequently Asked Questions

What veteran home buyer programs are available in San Antonio in 2026?

Veterans in San Antonio can access multiple stacking programs in 2026: the VA Home Loan (zero down, no PMI), the Texas Veterans Land Board (VLB) Housing Assistance Program (up to $832,750, discounted rate for 30%+ disability), Texas property tax exemptions (up to 100% for totally disabled veterans), SAH/SHA adapted housing grants (up to $109,986 and $25,350 respectively), the VA IRRRL refinance, VA Energy Efficient Mortgage, and The Beal Group's Serve & Save program which reduces closing costs up to 6% based on years of service.

Can a veteran use both a VA loan and the Texas VLB program together?

Yes, in many cases. The VLB Veterans Housing Assistance Program (VHAP) can be used alongside VA financing, potentially allowing a veteran to receive no down payment and no PMI while also benefiting from the VLB's discounted interest rate for veterans with a 30% or greater VA disability rating. Your lender must confirm first-lien position and eligibility. Note that the VLB requires the home to remain your Texas primary residence for at least three years — a critical consideration for military families who may PCS.

What is the Texas property tax exemption for disabled veterans in 2026?

Texas provides property tax exemptions tiered by VA disability rating: 10–29% = $5,000 exemption; 30–49% = $7,500 exemption; 50–69% = $10,000 exemption; 70–99% = $12,000 exemption; 100% (or unemployability designation) = complete exemption from all property taxes. A 100% disabled veteran in San Antonio with a $290,000 home saves approximately $5,000–$7,000 per year in property taxes, which is a significant annual benefit. Apply through the Bexar County Appraisal District with your VA award letter.

What is the VA Specially Adapted Housing (SAH) grant in 2026?

The SAH grant provides up to $109,986 in FY 2026 for veterans with severe service-connected disabilities (loss of lower extremities, paralysis, severe burns) to build, buy, or substantially modify a home for full accessibility. The SHA (Special Home Adaptation) grant provides up to $25,350 for veterans with blindness, hand loss, or burns who need targeted modifications like roll-in showers or widened doorways. Both grants are not loans — no repayment is required. Apply using VA Form 26-4555 through VA.gov.

What is the Serve & Save program and how does it benefit veteran buyers?

The Beal Group's Serve & Save program reduces closing costs for veterans at 1% per year of military service, up to a maximum of 6%. This is applied directly toward what the veteran pays at closing. For example, a veteran with 6+ years of service on a $290,000 home purchase could see closing costs reduced by approximately $17,400. This is separate from and stackable with VA loan benefits, VLB programs, and property tax exemptions. Contact Christopher Beal at (210) 882-8583 to learn your specific Serve & Save credit.

What is the VA IRRRL and who qualifies?

The VA Interest Rate Reduction Refinance Loan (IRRRL), also called the VA Streamline Refinance, allows veterans who already have a VA home loan to refinance to a lower interest rate with minimal paperwork and no appraisal required in most cases. You must be refinancing an existing VA loan (not switching from a conventional or FHA loan), and the refinance must result in a lower interest rate unless moving from an ARM to a fixed rate. No income verification or credit underwriting is required in most cases.

How much home can a veteran afford in the 78245 ZIP code near Lackland AFB?

Based on LERA MLS data through April 2026, the 78245 ZIP code (southwest San Antonio, near JBSA-Lackland) has a median sale price of $289,994 with 884 active listings and 6 months of inventory. Average price per square foot is $150. Using 2026 E-5 BAH for San Antonio with dependents ($2,214/month) and a VA loan at current rates with zero down payment, a veteran can comfortably target homes in the $270,000–$310,000 range in this area with no out-of-pocket down payment.

What is the VLB home loan limit for 2026?

As of January 2026, the Texas Veterans Land Board (VLB) increased the home loan limit to $832,750 — up from $806,500 in 2025. This increase of $26,250 applies to the Veterans Housing Assistance Program (VHAP). Veterans with a VA service-connected disability rating of 30% or greater qualify for a discounted interest rate (currently 5.85% fixed vs. the base rate of 6.35% fixed as of early 2026). Rates adjust weekly, so confirm the current rate with a VLB-participating lender before locking.

How does the VA Native American Direct Loan (NADL) work?

The VA Native American Direct Loan (NADL) program is a direct government loan (not a guarantee) available to eligible Native American veterans who wish to purchase, construct, or improve a home on federal trust land. Unlike the standard VA loan which is originated by private lenders, the NADL is directly funded by the VA. The tribal organization must have a Memorandum of Understanding with the VA. For most veterans in San Antonio who are not purchasing trust land, the standard VA loan is the appropriate program.

What builder incentives are available for VA buyers in San Antonio in 2026?

Major builders in San Antonio — including DR Horton, Lennar, and Perry Homes — regularly offer rate buy-downs, closing cost contributions, and option upgrades to attract VA buyers. However, veterans should work with an independent real estate agent (not the builder's agent) because the builder's on-site agent represents the builder, not the buyer. Under VA loan rules, sellers (including builders) can contribute up to 4% of the loan amount in concessions to a veteran buyer. Christopher Beal represents veteran buyers with builders at no cost to the buyer — call (210) 882-8583.

Your Veteran Advantage Starts Here

Christopher Beal | Veteran Real Estate San Antonio: The Beal Group

U.S. Army Veteran · MRP · SABJ Top 25 · 306+ Families Served · eXp Realty

Categories

- All Blogs (319)

- Alamo Heights (4)

- awards (3)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (76)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (6)

- Luxury (27)

- Luxury Real Estate (24)

- Market Trends (5)

- Market Update (13)

- Military Relocation (94)

- Military Retirement (3)

- Mortgage (18)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (16)

- PCS (27)

- Real Estate (32)

- reviews (2)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (5)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (65)

- San Antonio, Veterans Resources, VA Loans (5)

- Seller (25)

- VA Home Loans (28)

- VA Loans (33)

- Va Loans & Financing (26)

- Veterans (8)

- Veterans Resources (38)

Recent Posts