2026 JBSA BAH Rates — San Antonio Military Housing Allowance Guide

Last Updated: March 26, 2026

Updated February 2026 | Serving Fort Sam Houston, Lackland AFB, Randolph AFB, Camp Bullis & surrounding areas.

Searching for the best veteran Realtor in San Antonio or a top San Antonio veteran real estate agent? Christopher Beal, U.S. Army veteran, MRP-certified Military Relocation Professional, San Antonio Business Journal Top 25 Realtor (#13 in 2024, #14 in 2025), 3× Platinum Top 50 Agent, and founder of Veteran Real Estate San Antonio: The Beal Group, helps military families translate BAH into real homeownership at every JBSA installation. Call (210) 882-8583 or visit veteranrealestatesa.com.

What Is BAH?

Basic Allowance for Housing (BAH) is a monthly, non-taxable housing allowance provided to active-duty service members to cover housing costs when government quarters are not available. BAH is calculated based on three factors:

-

Rank / Pay Grade

-

Dependency Status (with or without dependents)

-

Duty Station ZIP Code (Military Housing Area)

For service members stationed at Joint Base San Antonio (JBSA), all installations — Fort Sam Houston, Lackland AFB, Randolph AFB, and Camp Bullis — fall within the same Military Housing Area (TX285), so BAH rates are identical regardless of which JBSA installation you're assigned to.

What Are the 2026 BAH Rates for JBSA San Antonio?

The 2026 BAH rates for Joint Base San Antonio range from $1,359/mo (E-1 without dependents) to $2,475/mo (O-6 with dependents). Rates decreased approximately 2.9% from 2025 across most pay grades. Existing recipients are typically protected by DoD rate grandfathering — new arrivals receive 2026 rates.

2026 JBSA Enlisted BAH Rates

Enlisted BAH rates at JBSA for 2026 cover pay grades E-1 through E-9. Note that E-1 through E-4 receive the same BAH rate under DoD guidelines. Rates shown use Army rank titles, the most common branch at Joint Base San Antonio.

| Pay Grade | With Dependents | Without Dependents |

|---|---|---|

| E-1 (Private) | $1,728/mo | $1,359/mo |

| E-2 (Private) | $1,728/mo | $1,359/mo |

| E-3 (Private First Class) | $1,728/mo | $1,359/mo |

| E-4 (Specialist/Corporal) | $1,728/mo | $1,359/mo |

| E-5 (Sergeant) | $1,869/mo | $1,500/mo |

| E-6 (Staff Sergeant) | $2,094/mo | $1,596/mo |

| E-7 (Sergeant First Class) | $2,112/mo | $1,731/mo |

| E-8 (Master Sergeant) | $2,121/mo | $1,920/mo |

| E-9 (Sergeant Major) | $2,157/mo | $1,977/mo |

*E-1 through E-4 receive the same BAH rate at all duty stations per DoD policy.

2026 JBSA Warrant Officer BAH Rates

Warrant officer BAH rates at JBSA for 2026 cover pay grades W-1 through W-5. These rates apply to all warrant officers stationed at any JBSA installation.

| Pay Grade | With Dependents | Without Dependents |

|---|---|---|

| W-1 (Warrant Officer 1) | $2,109/mo | $1,692/mo |

| W-2 (Chief Warrant Officer 2) | $2,118/mo | $1,917/mo |

| W-3 (Chief Warrant Officer 3) | $2,130/mo | $1,986/mo |

| W-4 (Chief Warrant Officer 4) | $2,178/mo | $2,085/mo |

| W-5 (Chief Warrant Officer 5) | $2,280/mo | $2,097/mo |

2026 JBSA Officer BAH Rates

Officer BAH rates at JBSA for 2026 cover all commissioned officer pay grades from O-1 through O-10, plus prior-enlisted officers (O-1E through O-3E). Rates shown are monthly amounts for ZIP code 78234.

| Pay Grade | With Dependents | Without Dependents |

|---|---|---|

| O-1 (2nd Lieutenant) | $1,905/mo | $1,584/mo |

| O-2 (1st Lieutenant) | $2,091/mo | $1,827/mo |

| O-3 (Captain) | $2,127/mo | $2,007/mo |

| O-4 (Major) | $2,307/mo | $2,088/mo |

| O-5 (Lt Colonel) | $2,457/mo | $2,100/mo |

| O-6 (Colonel) | $2,475/mo | $2,103/mo |

| O-7 (Brigadier General) | $2,490/mo | $2,112/mo |

| O-8 (Major General)* | $2,490/mo | $2,112/mo |

| O-9 (Lieutenant General)* | $2,490/mo | $2,112/mo |

| O-10 (General)* | $2,490/mo | $2,112/mo |

| O-1E | $2,115/mo | $1,866/mo |

| O-2E | $2,124/mo | $1,965/mo |

| O-3E | $2,196/mo | $2,082/mo |

*Note: The DoD groups O-7 through O-10 (general/flag officers) at the same BAH rate, designated O-7+ in official rate tables.

For official rate verification, visit the Defense Travel Management Office BAH Calculator.

Did JBSA BAH Go Up or Down in 2026?

JBSA BAH rates decreased approximately 2.9% from 2025 for most pay grades. The national average BAH increase was 4.2%, but rates vary by local housing market — and San Antonio's rental market data drove the reduction.

Key points about the 2026 decrease:

-

If you were already receiving 2025 BAH rates, DoD rate protection (grandfathering) typically preserves your higher rate as long as eligibility is continuous.

-

New arrivals to JBSA in 2026 will receive the lower 2026 rates.

-

Despite the decrease, San Antonio home prices remain approximately 21% below the national average, meaning BAH still stretches further here than in most duty stations.

What this means for buyers: A slightly lower BAH doesn't eliminate buying power, it shifts strategy. With the San Antonio median home price around $250,000–$290,000 and current VA loan rates in the 5.4%–6.2% range, many JBSA service members can still structure a mortgage where BAH covers most or all of the monthly payment when paired with a VA loan.

How Lenders Use BAH for VA Loan Qualification

Because BAH is non-taxable income, most VA-experienced lenders gross up the allowance by 25% when calculating your debt-to-income ratio. This gives BAH more mortgage leverage than the dollar amount alone suggests.

Example — E-5 with dependents:

-

BAH: $1,869/mo

-

Grossed up at 125%: $2,336/mo qualifying income

-

This increases maximum loan approval compared to taxable income of the same amount.

Not all lenders apply gross-up identically. Always confirm with a VA-experienced loan officer — not every lender treats military income the same way.

Additional VA loan advantages at JBSA:

-

Zero down payment — no 3–20% down required

-

No Private Mortgage Insurance (PMI) — conventional buyers pay $100–$300/mo in PMI; VA buyers pay $0

-

Seller concessions up to 4% of the purchase price toward closing costs, funding fee, or rate buydown

-

Disabled veterans may qualify for property tax exemptions in Texas, on a $305,000 home, a 100% disability exemption saves $5,000–$8,000/year

👉 Read: VA Loan Guide for San Antonio — entitlement, funding fee exemptions, and how to close with minimal out-of-pocket costs.

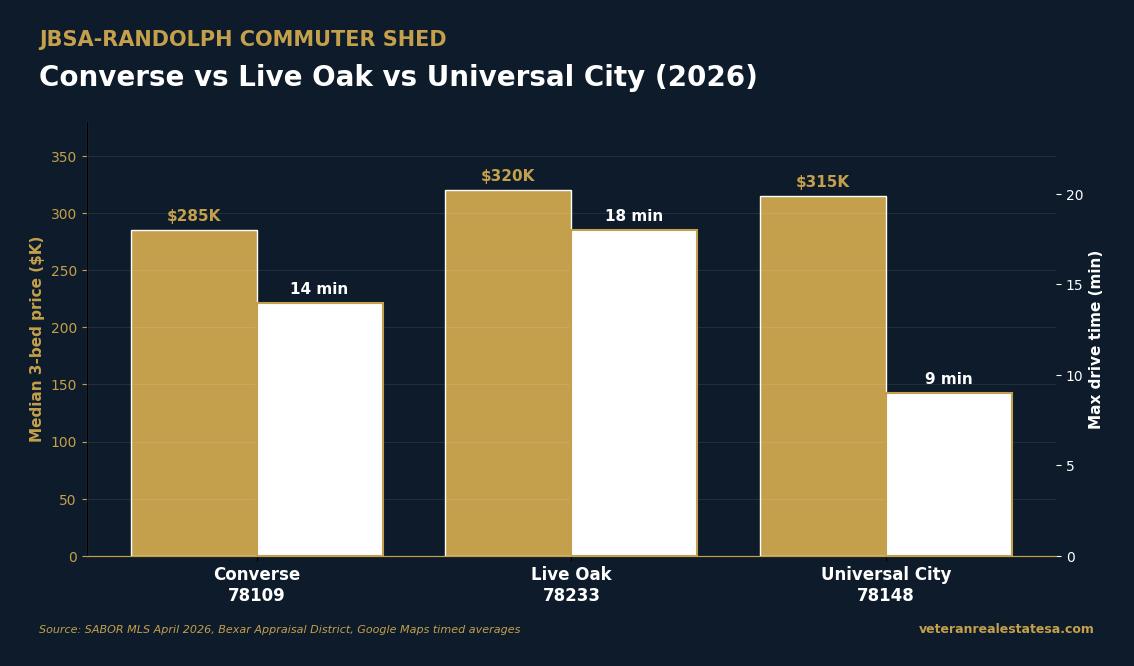

BAH by JBSA Installation

All JBSA installations share the same Military Housing Area (TX285), so your BAH rate is identical whether you're assigned to Fort Sam Houston, Lackland AFB, Randolph AFB, or Camp Bullis. However, where you buy determines how far that allowance stretches.

| Installation | Best Nearby Communities | Typical Price Range | Key Advantages |

|---|---|---|---|

| Fort Sam Houston | Schertz, Cibolo, Converse | $230K–$340K | SCUC ISD schools, strong resale |

| Lackland AFB | Helotes, Alamo Ranch, Westover Hills | $260K–$400K+ | Hill Country proximity, Northside ISD |

| Randolph AFB | Universal City, Schertz, Cibolo | $220K–$370K | Short commute, newer construction |

| Camp Bullis | Helotes, Boerne, Fair Oaks Ranch | $300K–$550K+ | Hill Country lifestyle, larger lots |

Each area has different price points, school districts, and commute considerations. Christopher Beal provides personalized neighborhood recommendations based on your rank, BAH bracket, family needs, and assigned installation.

👉 Read: Best Areas Near JBSA for Military Families

Where Does Your 2026 BAH Stretch Furthest?

San Antonio's housing costs run well below the national average, making it one of the most favorable BAH-to-homeownership markets in the country.

-

Schertz — Strong value relative to median pricing, established neighborhoods, SCUC ISD schools, equidistant between Randolph and Fort Sam

-

Cibolo — Active new construction inventory, slightly newer communities, ideal for families wanting a modern home within BAH budget

-

Universal City — Closest to Randolph, most affordable entry points, strong military resale demand

-

Helotes — Trends higher in price but offers Hill Country proximity, Northside ISD, and strong long-term appreciation

-

Converse — Budget-friendly option near Fort Sam and Randolph with improving infrastructure

For dual-military families with split JBSA assignments, Schertz sits almost exactly between Randolph and Fort Sam Houston — typically 12–15 minutes to each installation.

Worked Examples: What 2026 BAH Actually Buys at JBSA

Translating BAH into purchase price is the buying-power question every JBSA family asks. Use these examples as a starting point and verify with a VA-experienced lender for your specific scenario.

E-5 with Dependents at $1,869 BAH

Grossed up at 125 percent for VA-loan qualification: $2,336 monthly qualifying income. With a VA loan in the 5.4 to 6.2 percent range and Bexar County property tax around 2.2 percent, this supports a purchase price of roughly $250,000 to $300,000 depending on credit and other DTI. That fits 3-bedroom resale homes in older Alamo Ranch sections, Cibolo, Schertz, and Universal City.

O-3 with Dependents at $2,127 BAH

Grossed up: $2,659 qualifying income. Supports roughly $290,000 to $340,000 purchase price. Opens up newer Alamo Ranch sections, Stillwater Ranch, and the Cibolo Canyons-adjacent inventory.

O-5 with Dependents at $2,457 BAH

Grossed up: $3,071 qualifying income. Supports roughly $340,000 to $400,000 purchase price. That fits four-bedroom homes in newer Alamo Ranch sections, much of Boerne, parts of Bulverde, and select Hill Country options.

VA Loan Plus Serve and Save: Real Out-of-Pocket Numbers

The biggest myth I bust on weekly Zoom calls is that you need 20 percent down to buy a house. You do not. With a VA loan, you can put zero down, pay no PMI, and finance the funding fee. With the Beal Group Serve and Save program, a portion of my commission is credited at closing to reduce your closing costs at the table; this is a closing-table cost reduction, not a post-close rebate, which keeps you VA-loan compliant.

On a $300,000 home in Cibolo or older Alamo Ranch, the typical out-of-pocket for a VA buyer using Serve and Save runs:

- Earnest money: $1,000 to $3,000 (refundable per contract terms)

- Option period money: $200 to $500

- Inspection: $500 to $750

- Appraisal: $700 to $1,000 (sometimes credited)

- Net at closing after Serve and Save credit: often $0 to $2,000

That means a JBSA family with $5,000 to $7,000 saved can land a 3-bedroom home and use the rest of their BAH for actual living.

BAH and the Texas Disabled Veteran Tax Exemption Stack

The single highest-leverage move for a 100 percent disabled veteran in Texas is filing the homestead and disabled veteran property tax exemption together. A Texas-resident veteran with a 100 percent service-connected disability rating from the VA can be exempt from all property tax on their homestead.

What that means in BAH math: a $300,000 home in Cibolo typically carries roughly $7,200 to $7,800 per year in property taxes ($600 to $650 per month inside PITIA). Eliminate that line and your $1,869 BAH suddenly supports a much higher purchase price, or a much smaller monthly stretch. Veterans with partial disability ratings (10 to 90 percent) qualify for tiered exemption amounts. Your Bexar County, Comal County, or Kendall County appraisal district handles the application; bring your VA disability award letter and your DD-214.

4 BAH Mistakes JBSA Families Make in 2026

Mistake 1: Confusing BAH With Housing Cost Cap

BAH is what you receive, not what you must spend. Living below your BAH builds savings; matching your BAH funds your housing fully; exceeding it eats other budget categories.

Mistake 2: Ignoring Total Monthly Cost

PITIA is more than the mortgage. Texas property tax (roughly 2.2 percent annually in Bexar County) and homeowners insurance are non-trivial. Always run total monthly cost, not just principal and interest, before signing.

Mistake 3: Skipping Disabled Veteran Property Tax Exemption

If you are a 100 percent disabled veteran, you may qualify for a full property tax homestead exemption in Texas. That changes the buying-power math significantly. File homestead within the first year of ownership and apply the disabled veteran exemption with your county appraisal district.

Mistake 4: Rate-Shopping Without VA Lender Specialization

Not all lenders are equal on VA loans. A VA-experienced lender will run residual income, navigate VA appraisal reconsideration of value, and structure the loan to close on time. A retail lender can introduce avoidable delays that derail PCS timing.

Frequently Asked Questions About 2026 JBSA BAH

Does BAH cover 100% of my mortgage?

BAH is designed to offset average housing costs in your area. Whether it covers your full mortgage payment depends on your purchase price, interest rate, property taxes, insurance, and any HOA fees. In San Antonio, many service members can structure a VA loan where BAH covers all or most of the monthly payment at price points near the median.

Can I use BAH to qualify for a VA loan?

Yes. Lenders include BAH as qualifying income. Because BAH is non-taxable, many lenders gross it up by 25%, giving you more purchasing power than the dollar amount suggests on paper.

Does BAH change every year?

Yes. BAH rates are updated annually by the Department of Defense based on local rental market survey data. Rates can increase or decrease — 2026 JBSA rates decreased 2.9% from 2025.

If I buy a home, do I keep receiving BAH?

Yes. As long as you are eligible for BAH and not residing in government housing, your BAH continues — regardless of whether you rent or own.

What happens if BAH decreases after I buy a home?

DoD rate protection (grandfathering) typically preserves your current BAH rate as long as your eligibility is continuous. You would only receive a lower rate if you have a break in BAH eligibility.

Did BAH go up or down in San Antonio for 2026?

BAH decreased approximately 2.9% at JBSA for 2026. However, the national average increased 4.2%. San Antonio's decrease reflects local rental market data.

What can an E-5 with dependents afford in San Antonio?

An E-5 with dependents receives $1,869/mo in 2026 BAH. Grossed up at 125%, that's $2,336/mo in qualifying income. At current VA rates in the 5.4%–6.2% range, this supports a purchase in the $250,000–$300,000 range depending on credit, other income, and debt.

Next Step — Know Your Real Buying Power

Your BAH is more than a housing allowance, it's leverage. If you're PCS'ing to San Antonio or evaluating whether now is the right time to buy:

-

Get a personalized BAH-to-purchase analysis based on your rank, dependents, and financial profile

-

Compare neighborhoods aligned with your BAH bracket and assigned installation

-

Understand VA loan advantages in today's rate environment, including zero down, no PMI, and grossed-up BAH income

Christopher Beal, U.S. Army veteran, MRP-certified, San Antonio Business Journal Top 25 Realtor, has helped 256+ military families and veterans buy and sell homes across San Antonio and the Texas Hill Country.

📞 (210) 882-8583 | 📧 [email protected] | 🌐 veteranrealestatesa.com

👉 Schedule Your Military Homebuying Strategy Call Today

Related Resources

- JBSA Master Guide — All Installations

- PCS Move Timeline Guide 2026

- Military Relocation in San Antonio

- ETS Home Buying Guide San Antonio

- Should Active-Duty Military Rent or Buy?

- First-Time Home Buyer San Antonio Guide

- Military & Veteran Home Buying San Antonio

- VA Loan Funding Fee Guide

- Texas Veteran Property Tax Exemption

- Selling Your Home When You PCS or ETS

- Serve & Save — Veteran Real Estate Rebate Program

- San Antonio Relocation Guide

- Best Neighborhoods in San Antonio TX

- New Construction Homes San Antonio

- Luxury Homes for Sale in San Antonio TX

How to Maximize Your JBSA BAH for Homeownership in San Antonio

Understanding your 2026 BAH rate is just the first step. The real question is how to leverage that housing allowance to build long-term wealth through homeownership rather than paying rent. For service members stationed at JBSA-Lackland, Fort Sam Houston, or Randolph AFB, the VA loan benefit combined with San Antonio BAH rates creates a powerful path to owning your own home with zero money down.

Here is how the math works for a typical E-6 with dependents stationed at JBSA in 2026. With a BAH rate in the $1,800 to $2,000 per month range, you can comfortably afford a VA loan mortgage payment on a home priced between $280,000 and $330,000, depending on current interest rates and property tax rates. Because the VA loan requires no down payment and no private mortgage insurance, nearly your entire BAH goes directly toward your mortgage payment, property taxes, and homeowners insurance. Compare that to renting a three-bedroom apartment near base for $1,500 to $1,800 per month, where you build zero equity and are subject to annual rent increases.

Over a typical three-year PCS assignment, a military homeowner at JBSA can build $30,000 to $50,000 in equity through mortgage payments and home appreciation alone. Many service members choose to keep their San Antonio home as a rental property when they PCS to their next duty station, generating $200 to $400 per month in positive cash flow while continuing to build equity. This strategy has helped thousands of military families across JBSA build real estate portfolios that provide financial security long after their military career ends.

Want to see exactly how much home your BAH can buy in San Antonio? Call Christopher Beal at (210) 882-8583 for a free BAH-to-mortgage analysis. As a U.S. Army veteran and San Antonio Business Journal Top 25 Agent, Chris helps military families maximize their housing allowance every day. Visit veteranrealestatesa.com to get started.

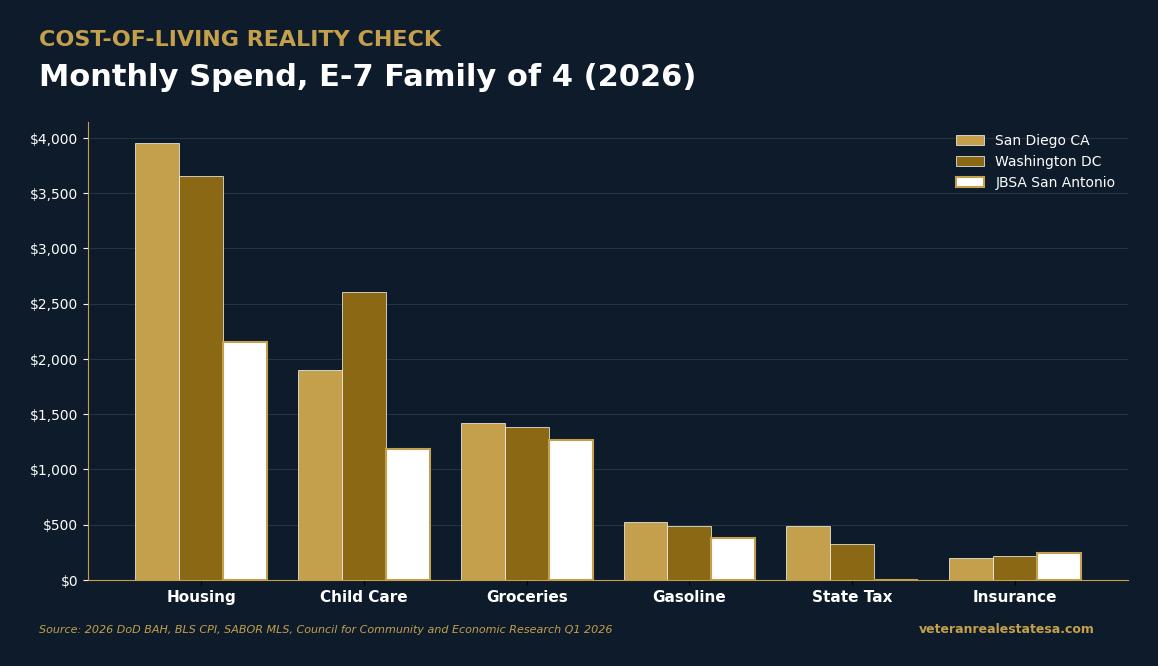

Why San Antonio BAH Rates Make It One of the Best Military Housing Markets in America

San Antonio consistently ranks as one of the most favorable markets in the country for military homebuyers, and the 2026 BAH rates reinforce that position. Unlike high-cost military hubs like San Diego, the DC metro area, or Hawaii, where BAH rates are high but home prices are even higher, San Antonio offers a sweet spot where BAH rates provide genuine purchasing power. The median home price in the San Antonio metro area hovers around $310,000, which is well within reach for E-5 and above service members using their full BAH toward a VA loan mortgage.

Texas also provides additional financial advantages for military families. There is no state income tax, which means your entire paycheck and BAH go further. Property taxes in Bexar County average around 2.2 percent, but the VA loan exemption and military homestead exemptions can significantly reduce that burden. Additionally, Texas offers generous veterans land and housing programs through the Texas Veterans Land Board, providing below-market interest rates for qualifying veterans and service members.

The combination of competitive BAH rates, affordable home prices, no state income tax, and the VA loan benefit makes San Antonio one of the smartest places in the country for military families to invest in real estate. Whether you are an E-3 buying your first home or an O-6 looking for luxury property in the Hill Country, The Beal Group has the expertise to help you find the right home at the right price. Christopher Beal, a 3-time Platinum Top 50 Agent and 6-time eXp ICON Agent, has personally helped hundreds of JBSA families turn their BAH into long-term wealth.

Ready to stop renting and start building equity near JBSA? Contact The Beal Group at (210) 882-8583 or visit veteranrealestatesa.com/military-relocation-san-antonio for your free military relocation consultation.

Frequently Asked Questions About JBSA BAH Rates in 2026

Does my BAH change if I live off base versus on base at JBSA?

Yes. If you live on base at JBSA, your BAH is forfeited to cover your government housing. If you live off base, you receive the full BAH rate for your pay grade and dependency status, which you can use toward rent or a mortgage payment. Most financial advisors recommend living off base and using your BAH toward a VA loan mortgage to build equity.

Can I use BAH to qualify for a VA loan mortgage near JBSA?

Absolutely. VA loan lenders count your full BAH as qualifying income when calculating your debt-to-income ratio. This means your BAH directly increases your borrowing power, allowing you to qualify for a larger mortgage than you might expect based on base pay alone.

What happens to my BAH if I PCS from JBSA to a different installation?

Your BAH rate adjusts to the new duty station location rate. However, if you purchased a home near JBSA with a VA loan, you can keep the property as a rental. Many military families generate positive cash flow from their San Antonio rental while receiving BAH at their new duty station.

Are 2026 JBSA BAH rates higher or lower than 2025?

The 2026 JBSA BAH rates reflect adjustments based on local housing cost surveys. San Antonio has seen moderate housing cost increases, so most pay grades received slight increases from 2025 levels. The Beal Group tracks these changes closely to help military families make informed homebuying decisions each year.

Explore More Resources

- VA Home Loans Guide

- Military Relocation San Antonio

- Serve & Save Program

- Client Reviews

- San Antonio Homes for Sale

- Read More Blog Articles

- What Is My Home Worth?

- Contact The Beal Group

Ready to make your move? Call Christopher Beal at (210) 882-8583 or visit veteranrealestatesa.com today.

Categories

- All Blogs (260)

- Alamo Heights (3)

- awards (2)

- Best Neighborhoods in San Antonio (13)

- Buyer (12)

- Buyer Education (47)

- Community Events (4)

- Hill Country (7)

- JBSA (29)

- Local Guide (5)

- Luxury (19)

- Luxury Real Estate (15)

- Market Trends (1)

- Market Update (12)

- Military Relocation (84)

- Military Retirement (2)

- Mortgage (4)

- Neighborhood Guides (13)

- neighborhoods (5)

- New Construction (13)

- PCS (23)

- Real Estate (23)

- reviews (1)

- San Antonio (53)

- San Antonio Lifestyle (4)

- San Antonio Market (1)

- San Antonio Neighborhoods (36)

- San Antonio Real Estate (58)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (9)

- VA Home Loans (14)

- VA Loans (17)

- Va Loans & Financing (26)

- Veterans (3)

- Veterans Resources (35)

Recent Posts