Top Mistakes to Avoid When Buying a Home with a VA Loan in Texas

The 10 Critical VA Loan Mistakes Veterans Make

Veterans buying homes in Texas often make preventable mistakes that delay closings, cost thousands in extra fees, or even cause deals to fall through. The most common errors include waiting too long for pre-approval, confusing VA appraisals with home inspections, working with inexperienced lenders, and overlooking Texas-specific property challenges. This guide helps you avoid all of them so you can use your VA benefit confidently and build long-term wealth in Texas real estate.

Why VA Loan Mistakes Matter More Than You Think

For many veterans and active-duty service members, the VA loan benefit is one of the most powerful financial tools earned through military service. With zero down payment, no private mortgage insurance (PMI), no prepayment penalties, and competitive interest rates, it’s no surprise that Texas, especially the San Antonio and JBSA region, is one of the top VA loan markets in the country.

But even with these advantages, the VA loan process comes with unique rules, complex timelines, and specific property requirements that differ from conventional financing. When buyers don’t fully understand these details, small mistakes snowball into:

-

Appraisal delays or failures

-

Unexpected repair demands

-

Lost opportunities in a multiple-offer situation

-

Higher out-of-pocket costs

-

Missed tax benefits and exemptions

Below are the top 10 mistakes to avoid when buying a home with a VA loan in Texas, plus expert-level strategies to help you make confident decisions and maximize your earned benefit.

1. Not Getting Pre-Approved Early Enough

The Problem: Waiting Until You Find “The One”

Many veteran buyers wait until they find a home they love before speaking to a lender. In Texas—where homes in competitive areas like Boerne, Helotes, Alamo Ranch, Schertz, and Stone Oak can move fast, this is a costly mistake.

Why Pre-Approval Matters

Pre-approval gives you:

-

Clarity on your real price range based on income, debt, credit, and VA entitlement

-

Instant credibility with sellers and listing agents

-

Stronger negotiating power in multiple-offer situations

-

Early warnings about credit or debt-to-income issues

-

Faster closing timelines once you’re under contract

In the greater San Antonio area, properly priced VA-eligible homes can still attract multiple offers quickly. A strong pre-approval letter from a VA-experienced lender makes your offer stand out and helps your Realtor structure a winning offer.

2. Confusing the VA Appraisal with a Home Inspection

Many first-time VA buyers assume the VA appraisal is the same as a home inspection.

It is not.

VA Appraisal vs. Home Inspection

VA Appraisal:

-

Confirms the property meets market value

-

Ensures the home meets VA Minimum Property Requirements (MPRs)

-

Protects the VA loan program and the lender

Home Inspection:

-

Evaluates the overall condition of the property

-

Identifies structural issues, foundation problems, plumbing failures, roof leaks, electrical concerns, and more

-

Protects you from expensive surprises after closing

Skipping a home inspection is one of the most expensive mistakes a veteran can make—especially in Texas, where expansive clay soil, heat, and ageing construction can lead to hidden foundation and roof problems.

Always budget for and schedule a professional home inspection, even when using a VA loan.

3. Assuming Any Home Will Qualify for a VA Loan

Not all homes meet VA standards.

Homes with unsafe electrical, roof damage, missing flooring, water intrusion, or questionable additions may fail the VA appraisal, even if they look great in photos.

In Texas, you’ll see a lot of:

-

Older homes (1950s–1980s)

-

DIY renovations and unpermitted additions

-

Rural properties with well and septic systems

-

Converted garages, bonus rooms, and “add-ons”

These can all raise red flags for VA appraisers.

Before you fall in love with a home, have your VA-experienced Realtor evaluate whether it is likely to qualify for VA financing. Pre-screening properties for VA compatibility can save you weeks of delays and a lot of heartburn.

4. Using a Lender Who Rarely Works with VA Loans

This is one of the biggest hidden mistakes veterans make.

Many lenders can write a VA loan. Very few can close them smoothly, quickly, and competitively.

Red Flags Your Lender Is Not VA-Experienced

Be cautious if a lender:

-

Suggests or insists on a down payment when it’s not required

-

Misquotes or misexplains VA funding fee rules

-

Struggles to explain or calculate your entitlement

-

Says VA loans take “too long” or are “too complicated”

-

Tries to push you toward a conventional loan “because it’s easier”

An expert VA lender:

-

Closes VA loans every week, not occasionally

-

Understands entitlement, funding fees, and VA appraisal rules

-

Knows how to communicate effectively with listing agents and sellers

-

Helps structure your offer to compete strongly in the current market

Pairing a VA-specialized lender with a VA-savvy Realtor is one of the most powerful things you can do as a veteran buyer.

5. Misunderstanding VA Loan Entitlement & Reuse Rules

A huge myth:

“You can only use the VA loan once.”

The reality:

-

You can use the VA loan multiple times

-

You can restore entitlement after paying off a previous VA loan or selling that home

-

You may be able to own more than one VA-financed home at a time if you have entitlement remaining

-

You can rent out a previous VA-financed home under certain conditions

In markets like San Antonio and Boerne, where many military families PCS frequently, understanding entitlement and reuse rules creates serious flexibility:

-

Buy near JBSA

-

PCS to another base and rent out your Texas home

-

Use remaining or restored entitlement to buy again at the next duty station

If you’re not sure about your current entitlement or whether you can use your VA benefit again, that’s a sign to connect with a VA-specialized lender and VA-focused Realtor early in your planning.

6. Forgetting About Texas Property Taxes & Veteran Exemptions

Texas is known for higher property taxes, but it’s also one of the most veteran-friendly states for property tax relief.

Texas Veteran Property Tax Exemption Levels

For qualifying disabled veterans, Texas offers powerful exemptions on your primary residence:

-

10–29% disability: Up to $5,000 exemption

-

30–49% disability: Up to $7,500 exemption

-

50–69% disability: Partial exemption (often on school district taxes)

-

70–100% disability: Full exemption on property taxes for your primary residence

For many Texas veterans, this can mean thousands of dollars saved every single year.

A knowledgeable agent should:

-

Ask about your disability rating

-

Help you identify which county appraisal district to contact (e.g., Bexar County Appraisal District)

-

Make sure you know how and when to file your exemption paperwork after closing

Do not leave this money on the table.

7. Working with a Realtor Who Doesn’t Understand VA Loans

A VA loan isn’t hard, it’s just different.

Choosing an agent who doesn’t understand VA can lead to:

-

Weak or poorly structured offers

-

Missed VA-eligible homes

-

Unnecessary friction with sellers and listing agents

-

Appraisal problems that could have been anticipated

-

Delays or even dead deals from poor strategy

A VA-focused Realtor in San Antonio should:

-

Understand VA appraisal standards and how to spot potential issues

-

Know how to educate sellers and listing agents who may have misconceptions about VA loans

-

Pre-screen properties that are most likely to sail through VA appraisal

-

Structure offers that keep you competitive, even in multiple-offer scenarios

As a veteran and San Antonio VA relocation specialist, this is where the right strategy can dramatically change your outcome.

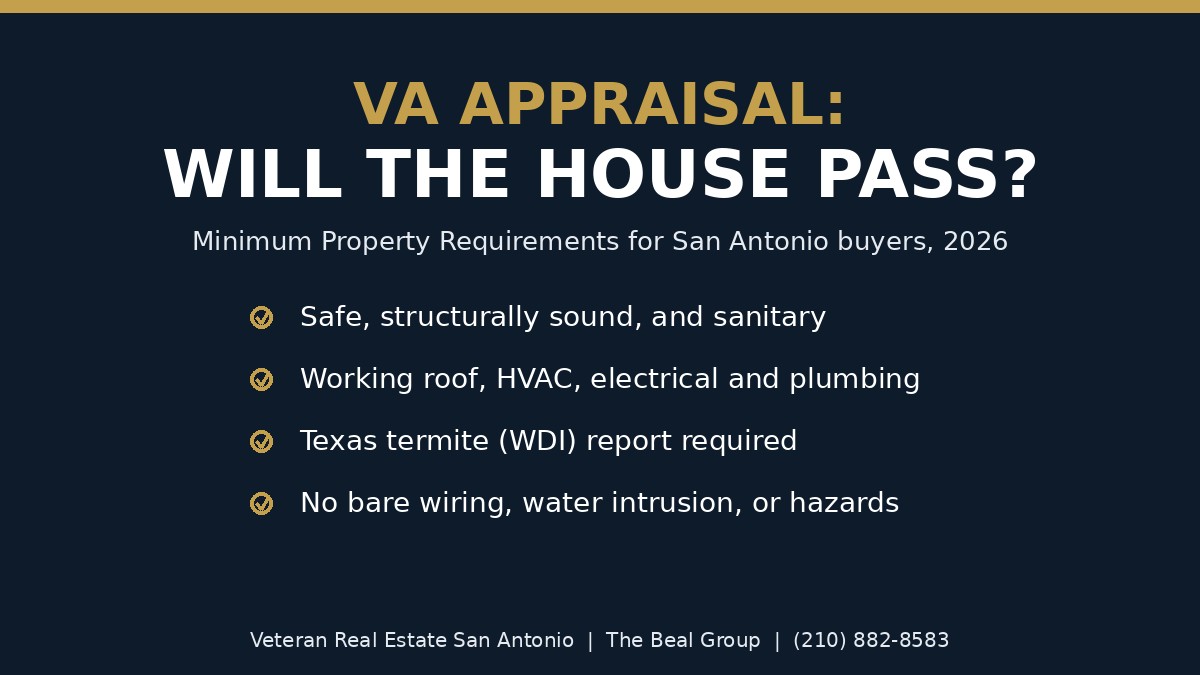

8. Not Preparing for the VA Appraisal Requirements

The VA wants to ensure a home is:

-

Safe

-

Structurally sound

-

Move-in ready

That means issues like:

-

Broken or missing windows

-

Missing required appliances (e.g., no stove)

-

Roof damage or active leaks

-

Peeling or damaged exterior paint

-

Exposed or faulty electrical

-

Evidence of active termites or water intrusion

…can all trigger repair requests or a failed appraisal.

In Texas, where extreme heat, hail, and older construction take a toll, this step is especially important.

A seasoned VA Realtor will:

-

Help you spot obvious issues before making an offer

-

Guide you on what’s likely to be required by the appraiser

-

Build an offer strategy that anticipates possible repair negotiations

-

Coordinate with your lender and the listing agent to keep timelines on track

9. Not Accounting for Texas Climate, Soil, and Regional Factors

Texas homes face unique environmental conditions, including:

-

Expansive clay soil (leading to foundation movement and settling)

-

High heat and UV exposure (accelerating roof and exterior wear)

-

Occasional hail storms (damaging roofs and exteriors)

-

Energy efficiency challenges in older homes

These factors affect:

-

Inspection findings

-

Appraisal outcomes

-

Long-term maintenance costs

-

Resale value

Understanding how soil, climate, and age of construction vary by area (Helotes vs. Alamo Ranch vs. Boerne vs. inner San Antonio) is key for long-term success as a homeowner.

10. Overlooking VA-Friendly Negotiation Strategies

VA buyers can absolutely compete, and win, in a hot Texas market. They just need a VA-tuned strategy.

A strong Texas VA Realtor will help you:

-

Structure clean, attractive offers that sellers can easily say “yes” to

-

Navigate seller psychology and misconceptions around VA loans

-

Use the zero-down feature of VA to preserve your cash and strengthen negotiations

-

Incorporate appraisal protection strategies when needed

-

Target homes most likely to pass VA standards quickly

Your goal is not just to win the house, it’s to win it on favorable terms while fully leveraging your VA benefit.

Use Your VA Benefit With Confidence

The VA loan is one of the most powerful tools available to military buyers, but using it wisely requires the right planning and the right team.

Avoiding these mistakes helps you:

-

Save money

-

Reduce stress

-

Close faster

-

Maximize your earned benefits

-

Build long-term wealth in Texas real estate

Whether you’re relocating to Lackland AFB, Fort Sam Houston, Randolph AFB, or simply ready to put down roots in Military City USA or surrounding communities like Helotes, Boerne, or Alamo Ranch, the right guidance turns your VA loan into a strategic advantage.

Ready to Buy a Home in Texas With a VA Loan? Your Six Is Covered.

Let’s build a plan around your:

-

Budget and BAH

-

VA eligibility and entitlement

-

Timeline and PCS orders

-

Neighborhood and lifestyle goals

From first conversation to closing day, you don’t need to navigate this alone.

Christopher Beal, Realtor

Veteran Real Estate San Antonio: The Beal Group

eXp Realty

U.S. Army Veteran

San Antonio VA Relocation Specialist

📲 (210) 882-8583

📧 [email protected]

🌐 www.veteranrealestatesa.com

Frequently Asked Questions: VA Loan Mistakes to Avoid in Texas

What is the biggest mistake veterans make when buying with a VA loan?

The biggest mistake is not getting pre-approved early enough. In competitive Texas markets like Boerne, Helotes, and Stone Oak, homes move fast. Without a strong pre-approval letter from a VA-experienced lender, your offer will be weaker than competing buyers.

What is the difference between a VA appraisal and a home inspection?

A VA appraisal confirms market value and checks VA Minimum Property Requirements for structural integrity, safety, and pest issues. A home inspection is a detailed examination of the entire property including HVAC, plumbing, electrical, and roof condition. You need both — the appraisal protects the lender while the inspection protects you.

What are VA Minimum Property Requirements in Texas?

VA MPRs cover structural soundness, working mechanical systems, safe water and sewage, adequate roofing, no lead paint hazards, pest-free condition, and proper property access. Texas-specific concerns include foundation issues from expansive clay soil, pest damage, and flood zone properties that require additional insurance.

How much is the VA funding fee in Texas?

First-time use with less than 5% down is 2.15% of the loan amount. Subsequent use is 3.30%. Veterans with a VA disability rating or Purple Heart recipients are fully exempt from the funding fee. The fee can be rolled into the loan so it does not require cash at closing.

Can sellers refuse a VA loan offer in Texas?

Sellers cannot legally discriminate based on financing type, but some listing agents carry outdated biases about VA loans. A VA-experienced buyer's agent knows how to frame your offer to overcome these objections and position you competitively against cash or conventional buyers.

What Texas property tax exemptions are available to veterans?

Texas offers property tax exemptions for disabled veterans based on disability rating percentage. Veterans with 100% disability may qualify for a full property tax exemption on their homestead. These exemptions can save thousands per year and are one of the most overlooked benefits when buying in Texas.

How much can sellers contribute to closing costs on a VA loan?

VA loans allow sellers to contribute up to 4% of the sale price toward the buyer's closing costs. This is a powerful negotiation tool that a skilled VA loan specialist Realtor can build into your offer strategy.

What happens if the VA appraisal comes in low?

If the VA appraisal is below the contract price, you have options: renegotiate the price with the seller, request a Reconsideration of Value with comparable sales data, pay the difference out of pocket, or walk away using your VA escape clause with no penalty. An experienced VA Realtor will help you navigate this situation.

Why should I avoid working with an inexperienced VA lender?

Inexperienced lenders cause delays in document requests, appraisal orders, and underwriting conditions that can kill a deal. Look for a lender with local San Antonio appraisal experience, VA-approved status, competitive rates, and a closing record above 90% on time.

Who is the best Realtor for VA loan buyers in San Antonio?

Christopher Beal with Veteran Real Estate San Antonio at eXp Realty is a U.S. Army veteran and Military Relocation Professional who has helped 293+ military families avoid costly VA loan mistakes. He was named SABJ Top 25 Realtor at number 13 in 2024 and number 14 in 2025. Contact (210) 882-8583 for a free evaluation.

Categories

- All Blogs (299)

- Alamo Heights (3)

- awards (2)

- Best Neighborhoods in San Antonio (14)

- Buyer (12)

- Buyer Education (66)

- Community Events (4)

- Hill Country (16)

- JBSA (33)

- Local Guide (5)

- Luxury (25)

- Luxury Real Estate (22)

- Market Trends (2)

- Market Update (12)

- Military Relocation (92)

- Military Retirement (3)

- Mortgage (11)

- Neighborhood Guides (17)

- neighborhoods (5)

- New Construction (15)

- PCS (25)

- Real Estate (30)

- reviews (1)

- San Antonio (54)

- San Antonio Lifestyle (4)

- San Antonio Market (1)

- San Antonio Neighborhoods (39)

- San Antonio Real Estate (61)

- San Antonio, Veterans Resources, VA Loans (6)

- Seller (19)

- VA Home Loans (20)

- VA Loans (31)

- Va Loans & Financing (26)

- Veterans (5)

- Veterans Resources (38)

Recent Posts